Private banking, unlike traditional or retail banking, is a relationship-first approach to financial services that pairs high-net-worth individuals with dedicated banking and financial experts who know their full financial picture. Instead of explaining their needs and history every time, clients work with a dedicated team who knows them and their financial picture well. At First Business Bank, private banking operates within a broader Private Wealth model, so a client's banking needs are coordinated directly by Wealth Advisors who help connect daily banking decisions to long-term financial plans.

What Is Private Banking?

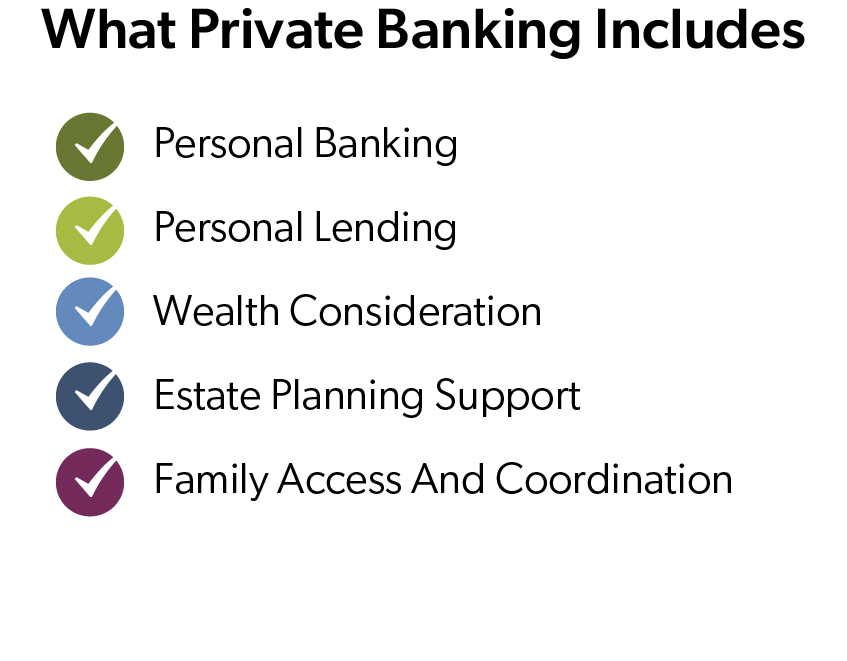

Private banking is a specialized suite of banking services for individuals, typically encompassing checking, money market accounts, lending, and cash management, delivered through a dedicated, relationship-driven model rather than a branch or call center. The services are structured around a client's personal financial life: their assets, family, goals, estate, and legacy.

Private banking is a specialized suite of banking services for individuals, typically encompassing checking, money market accounts, lending, and cash management, delivered through a dedicated, relationship-driven model rather than a branch or call center. The services are structured around a client's personal financial life: their assets, family, goals, estate, and legacy.

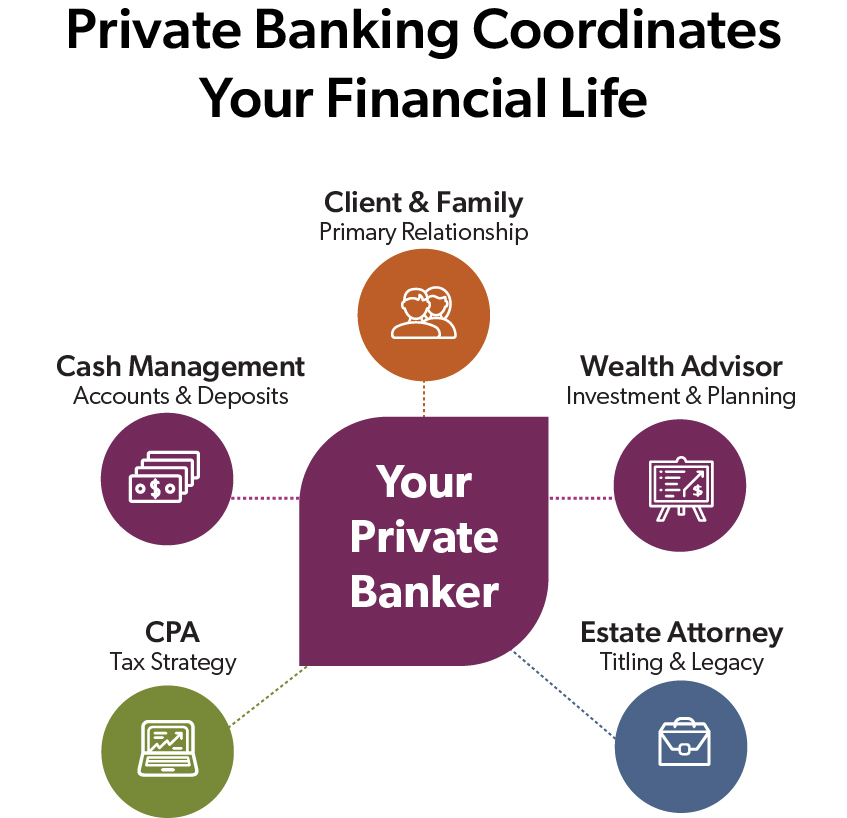

The level of integration, personalized service, and coordination all separate private banking from standard personal banking. At First Business Bank, private banking functions as one component of a holistic wealth relationship. That means a client's banking needs are communicated directly through their Wealth Advisor, who, in turn, coordinates with estate planning and tax professionals, and helps ensure that banking activity aligns with their broader financial strategy. When an advisor recommends adjusting how accounts are titled for estate planning purposes, the Wealth Advisor handles the execution. When a lending need comes up, it is evaluated in the context of the client's full financial picture, not just a credit profile.

This stands in contrast to the volume-based model most large banks operate on, where product sales drive the relationship and clients rarely speak to the same person twice. First Business Bank's model is built around deep relationships with clients, not scale. Private banking clients aren't a number in a queue. They're business owners, executives, and professionals whose financial lives are complex enough to warrant a partner who pays attention.

Why Do Busy Professionals Choose Private Banking?

For many high-net-worth individuals, standard personal banking comes with increasing friction of managing a complex financial life across too many relationships, accounts, and institutions that don't communicate with each other.

Here's what that often looks like. A client has a personal checking account at one bank, a mortgage at another, investment accounts at a third, an accountant with a different firm, and a business banking relationship somewhere else entirely. Each knows a slice of the financial picture. None of them know the client’s goals. When a question comes up that crosses those boundaries, the client spends more and more time coordinating their own financial life across providers.

Private banking clients typically make the switch when one or more of these pain points reaches a tipping point:

- Repetitive onboarding. Every new banking interaction starts from scratch. Clients re-explain their situation, goals, and history to someone who has no context, only numbers in front of them.

- Fragmented personal and business finances. For business owners and executives, the line between personal and business wealth is rarely clean. Standard personal banking doesn't accommodate that overlap very well.

- Slow decisions. When a time-sensitive lending need or liquidity question comes up, a big-bank process built for volume doesn't move at the speed that busy lives require.

- No proactive guidance. Standard banking is reactive — banks wait for clients to call for something. Private banking flips that dynamic with a proactive model.

For busy professionals, the administrative burden of managing fragmented banking relationships compounds quickly, and lack of time and frustration often drives the decision to consolidate.

What White-Glove Private Banking Service Looks Like

At First Business Bank, private banking clients are assigned a dedicated Wealth Advisor who serves as their primary point of contact across all personal banking needs. When something comes up, clients reach a live, local person, not an AI chatbot, not an 800 number, and not an offshore call center.

The day-to-day experience of private banking, depending on client needs, looks different from standard banking in several ways:

- Proactive account reviews. Rather than waiting for clients to identify a problem, Wealth Advisors initiate regular check-ins to review account structures, flag opportunities, and make sure banking arrangements still reflect current goals and circumstances.

- Fee waivers and elevated account features. Private banking relationships typically include waived wire fees, free checks, and premium money market and checking account options that aren't available through standard retail banking.

- Accessibility for the whole relationship. When a client's spouse, adult child, or estate attorney needs help, they can access advisors who know the full picture. Private banking isn't just for the primary account holder.

- Coordination with the wealth team. A client's Wealth Advisor, Trust Advisor, and Portfolio Manager work from the same understanding of the client's financial life, which means banking decisions don't happen in isolation from investment, tax, or estate planning conversations.

Coordination is an important value for private banking clients. When advisors aren't in touch with each other, accounts are titled incorrectly, liquidity sits idle when it can work harder, and time-sensitive opportunities might be missed because no one connected the dots.

Private banking at First Business Bank is structured to close those gaps and handle the unexpected. When a client faces a time-sensitive property closing, has an accessibility need that requires a different level of support, or encounters a family situation that requires discretion, how a Wealth Advisor handles those scenarios matters more than any account feature.

How Does Private Banking Protect and Simplify Your Deposits?

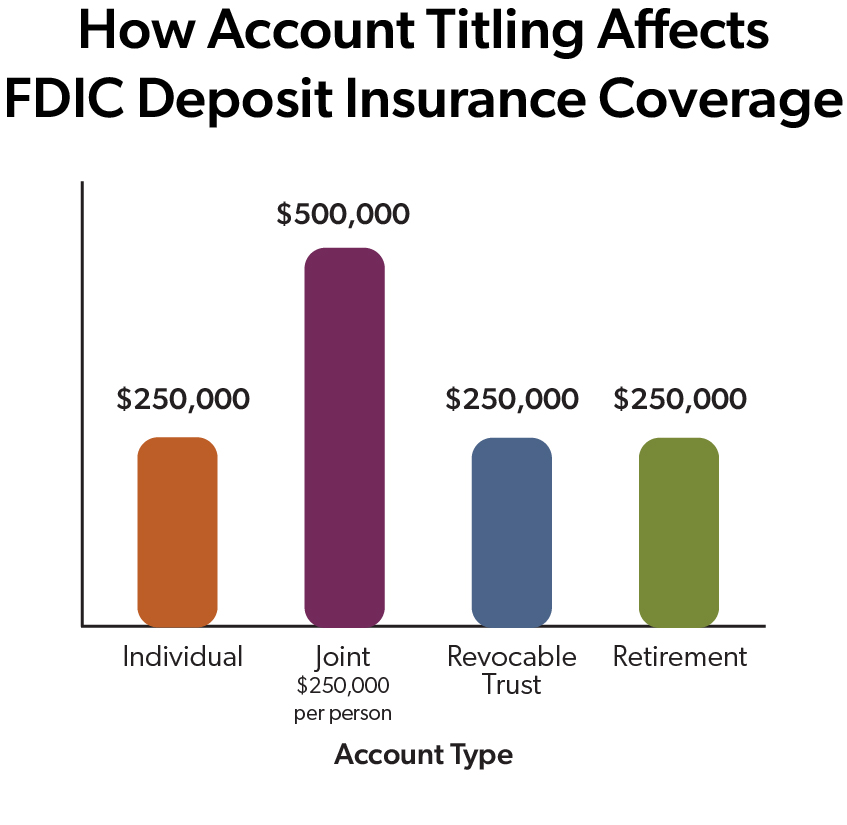

For high-net-worth individuals, FDIC Deposit Insurance coverage for their deposits can get complex quickly. The standard limit is $250,000 per depositor, per institution, per ownership category, but federal rules defining ownership category can be tricky.

Account titling is critical for ownership categories. An individual account, a joint account, a revocable trust account, and a retirement account all represent separate ownership categories under FDIC rules. Understanding how to structure and title accounts across those categories can achieve coverage well beyond the base $250,000 limit at a single institution, without spreading money across ten different banks to do it.

Account titling is critical for ownership categories. An individual account, a joint account, a revocable trust account, and a retirement account all represent separate ownership categories under FDIC rules. Understanding how to structure and title accounts across those categories can achieve coverage well beyond the base $250,000 limit at a single institution, without spreading money across ten different banks to do it.

A dedicated Wealth Advisor walks through account structures with clients, identifies gaps in coverage, and helps implement titling strategies that reflect both their current situation and their estate plan. For clients who have historically kept accounts at multiple institutions specifically to manage deposit insurance coverage, consolidation suddenly becomes an option, and often a cleaner one.

Consolidation also matters for estate administration. Surprisingly, a common challenge for families navigating a loved one's estate is simply locating all the accounts. When assets are scattered across multiple institutions with no clear documentation, heirs and attorneys spend a lot of time tracking down accounts. Private banking helps clients bring accounts into a coherent, well-documented structure while they're still managing their financial life.

This level of financial organization creates clarity, reduces administrative burden for families, and ensures that the estate plan their attorney drafted reflects how their banking is set up.

How Does Private Banking Support Sophisticated Lending Needs?

For business owners, executives, and high-net-worth individuals, borrowing needs tend to be complex, time-sensitive, and deeply tied to their broader financial picture.

A few examples illustrate what that looks like in practice. A senior executive may need personal financing to buy into a business partnership, a transaction that requires a lender who understands both the individual's financial position and the structure of the deal. A business owner managing a succession transition may need liquidity that bridges personal and business finances simultaneously. A client with significant real estate holdings may want to consolidate multiple pieces of collateral into a single, coherent loan structure rather than managing several separate obligations.

A few examples illustrate what that looks like in practice. A senior executive may need personal financing to buy into a business partnership, a transaction that requires a lender who understands both the individual's financial position and the structure of the deal. A business owner managing a succession transition may need liquidity that bridges personal and business finances simultaneously. A client with significant real estate holdings may want to consolidate multiple pieces of collateral into a single, coherent loan structure rather than managing several separate obligations.

Lending decisions within the context of a private banking relationship benefit from knowing the full financial picture, including a client's assets, their business relationship, their cash flow patterns, and their long-term goals.

This approach reflects a deliberate philosophy. Private banking applies sound judgment to situations that require more than a standard underwriting checklist. Clients with complex financial needs benefit from a lender who considers their entire situation before reaching a decision, and who has the authority and experience to act quickly.

How Is First Business Bank's Private Banking Different?

Most banks offer some version of preferred client service. What sets First Business Bank apart is relationship continuity, for the client and for their family. When a spouse, child, or heir needs support, they work with advisors who already know the family's financial history. For clients thinking about philanthropy and generational wealth, that familiarity has practical value when it matters most.

First Business Bank's private banking team also operates without the bureaucracy that slows down large institutions. Clients have direct access to decision-makers, and the people handling their relationships have the experience and authority to find solutions that a standard retail banking model isn't designed to offer.

Is Private Banking Right for You? Key Questions to Ask

Private banking delivers the most value for individuals whose financial lives have grown beyond standard banking. A few questions to ask:

Private banking delivers the most value for individuals whose financial lives have grown beyond standard banking. A few questions to ask:

- Are assets spread across multiple banks with no clear organizational structure?

- Do personal and business finances overlap in ways that require a lender who understands both sides?

- Is coordination between a banker, a financial advisor, an accountant, and an attorney falling on the high-net-worth individual?

- When a time-sensitive financial decision comes up, does the current bank move fast enough?

If the answer to most of those questions is yes, private banking is worth a conversation.

How to Get Started With Private Banking at First Business Bank

An initial conversation with a Private Wealth Advisor will cover the basics like current account structures, banking relationships, and whether private banking is a good fit for the client's situation.

From there, onboarding typically includes an account titling review, fee structure alignment, and introductions to the broader wealth advisory team. Most clients see immediate practical benefits, including fee waivers and consolidated account structures, before the broader relationship fully takes shape. For many, the greatest value is the peace of mind and confidence from having an organized financial life and the time gained from having an experienced team working on their behalf.