As companies of all sizes prepare for an economic downturn, some report they’re paying invoices late or not paying at all to correct financial difficulties. Of the 85% of employer firms who reported financial challenges in the 2022 Small Business Credit Survey, nearly one-third made a late payment or did not pay. How does this affect your own business’s accounts receivable collections?

As companies of all sizes prepare for an economic downturn, some report they’re paying invoices late or not paying at all to correct financial difficulties. Of the 85% of employer firms who reported financial challenges in the 2022 Small Business Credit Survey, nearly one-third made a late payment or did not pay. How does this affect your own business’s accounts receivable collections?

Let’s start by focusing on what you can control — improving your cash flow by implementing the latest accounts receivable collections best practices for businesses .

Accounts Receivable Collections Best Practices

In a recent episode of the First Business Bank Podcast, my colleagues Melissa Fellows and Kim Preston, both Senior Vice Presidents of Treasury Management, joined me to discuss Tips to Improve Accounts Receivable Collection. Both of them are experts in helping businesses to optimize their cash flow, reduce back-office processing, strengthen security, and improve their financial operations overall.

In a recent episode of the First Business Bank Podcast, my colleagues Melissa Fellows and Kim Preston, both Senior Vice Presidents of Treasury Management, joined me to discuss Tips to Improve Accounts Receivable Collection. Both of them are experts in helping businesses to optimize their cash flow, reduce back-office processing, strengthen security, and improve their financial operations overall.

Let’s walk through our experts’ recommended best practices to improve accounts receivable collections .

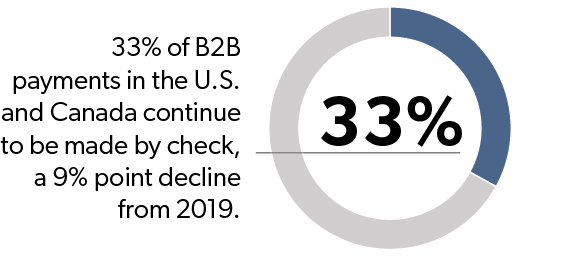

Get Funds Into Your Account Faster

“While we love seeing you in our lobby, from a business efficiency and timing standpoint, there are multiple reasons to stop bringing checks or deposits to the bank,” Fellows said. How long do checks sit in your office? How many employees can access them? Consider the liability of employees bringing significant volumes of cash or checks to the bank, and how long it’s taking to get those funds into your account.

Talk to your banker about getting your receivables into your account in a timely, efficient, and safe manner that works for your organization, such as mobile or remote deposit, accepting electronic payments, or outsourcing receivables with Lockbox .

Depositing funds faster not only improves efficiency, it also drives revenue. When rates are low, near zero, this isn’t as meaningful and the idea of advantages around collecting funds faster, putting them to work faster, didn't maybe mean as much. Now, whether it's interest-bearing account or other investment vehicle, with rates now up, that means a lot more. Alternatively, if you have cash available faster to reduce your borrowing on a line of credit, borrowing rates are going up as well.

Securely Store Sensitive Information

Do your clients’ account numbers or credit card numbers live in a filing cabinet or your accounting system? Transfer them to a more secure environment.

“If you're holding account numbers or credit card numbers in your accounting software system or a filing cabinet somewhere, definitely use your bank platform or your merchant partner’s online platform to securely store that information,” Fellows said.

Implement Efficient Check Reporting

Our experts have watched many nonprofit organizations photocopy checks before running to the bank to deposit them. Simple, secure technology allows you to scan and deposit at the same time, efficiently fulfilling two needs at once.

“Scanning technology allows you to deposit the check from your office, and it’s also taking an image of that check for you,” Fellows said. “Or, likely your bank is imaging that check for you for overnight processing. So talk to your bank about ways you can get better reporting for the paper checks you’re depositing at the bank.”

Automate Accounts Receivable Collection To Improve Processes

There’s a comfort in “the way we’ve always done things.” In an unpredictable economy, when you’re searching for advantages, adopting automation to improve efficiency can make a big difference in several areas of the business saw an uptick.

“We try to educate clients on different options to try,” said Kim Preston. “For instance, during the pandemic, we saw an uptick in the use of remote deposit and Lockbox, but there are several other options, from an ACH standpoint. You have the ability to hold funds from your vendors — it's called an ACH collection. Take a look at your existing processes because efficiency not only drives more revenue, from a workforce standpoint, your employees have more time if they’re not doing these mundane tasks. They can put their hours to work for other initiatives.”

In an environment where it's harder to get new teammates, or, alternatively, with the existing staff you can take on even more business without having to add incremental FTE. That, is a really important point around this idea of automation, streamlining, moving away from paper and toward electronic solutions on the collection side of things, as well.

“It's not a case where if someone decides they want to automate, they have to all at once,” Preston said. “They can ease into it to test it out a little bit with a few key clients to get some feedback from them on how it works.”

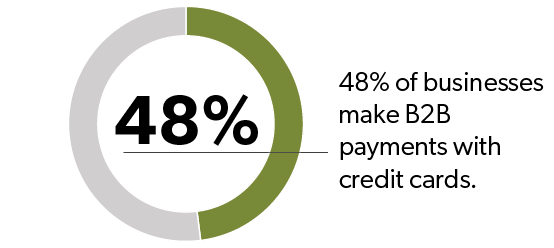

Consider Accepting Credit Cards In The Right Situations

Accepting credit card payments, which allow you to collect on your invoices faster than a check, is not necessarily the right fit for all businesses.

“When considering credit card payment processing, think about the industry and who is your client base?” Fellows said. “Restaurants and retail, for example, have to accept credit cards. If you accept larger dollar payments, but lower volume, accepting credit cards can be expensive. So make sure you speak with a credit card provider to determine that you're collecting card information in an efficient, secure manner to lower the interchange rate to make it as cost effective as you can. Think, ‘What is my cost to accept this payment?’ And maybe you need to capture that in your invoice when you're billing your customer.”

The positives of accepting credit cards sometimes outweigh the negatives.

“Most importantly, will you add additional clients if you accept a credit card payment, and does it make it easier to do business?” Fellows said. “I also think of not-for-profits. Yes, it might be a more costly payment to accept, but you're going to be collecting additional donations that maybe you would not have otherwise had you not offered credit card as an option for your donors.”

“Most importantly, will you add additional clients if you accept a credit card payment, and does it make it easier to do business?” Fellows said. “I also think of not-for-profits. Yes, it might be a more costly payment to accept, but you're going to be collecting additional donations that maybe you would not have otherwise had you not offered credit card as an option for your donors.”

There are other, potentially unexpected, outcomes of accepting credit cards, Preston points out. There are some statistics, in cases where credit card is used as an option for payments, that people tend to spend more,” Preston said. “Cards are becoming more prevalent even around B2B businesses now because they can earn revenue and generate revenue on their end when they use a card. Virtual card is also coming into play. Having multiple options for your clients to pay is a good thing.”

Credit cards also allow businesses to know immediately whether or not funds are available for the payment. “You're going to know right away when a credit card or a debit card is declined, whereas with a check, there might also be a fund's availability instance,” Fellows said. “And so, you're mitigating that by accepting a credit card payment.”

Manage Receivables Effectively & Electronically

Once you’re collecting your accounts receivable as quickly as possible, it’s instantly available in your account. Then what? An experienced banker can help you determine the most advantageous way for you to manage your receivables .

Once you’re collecting your accounts receivable as quickly as possible, it’s instantly available in your account. Then what? An experienced banker can help you determine the most advantageous way for you to manage your receivables .

“An example when funds are immediately available to you via ACH, is it better for your company to apply that directly to a line of credit to save an interest expense?” Fellows said. “So as much as you can direct electronically, it makes those funds immediately available, and can make reconciliation simpler because it’s less likely that something is going to come back insufficient.”

Reduce Accounts Receivable Errors & Fraud

Automating and outsourcing your accounts receivable with a solution like Lockbox services helps to reduce human error and payment fraud.

“With Lockbox, we're accepting your check deposit, but we can also help with reporting,” Fellows said. “We work with our clients and determine the client account number, client name, and the information you're looking for from a payment so that you can accept a file and automatically apply that to your accounts receivable system. There's additional value in error reduction by taking that human element out of manually posting a payment.”

“From a fraud perspective, too, there’s no manipulation of incoming payments,” Preston said. “It’s not always going to be the case that clients experience inside fraud, but the fraud risk is definitely mitigated by automating it.”

Make Paying Easy For Your Clients & Donors

Especially in this rocky economic environment, the bottom line is that you should try to make paying your organization as seamless as possible.

“Who is your client base, and who do you want your client base to be?” Fellows said. “Create a receivables process that aligns with your company's mission, and make it simple. Not-for-profit organizations should make it easy for donors to make a donation with a link on your website, offering multiple payment options for donors, and making that donation as seamless as possible.”

“In today's world, if you're being innovative, that looks good from your client's perspective,” said Preston. “You’re adapting to change; you are in the 21st century and moving forward. We strive to help our clients be innovative and bring them new solutions and ideas. Not everything is going to work, but at least talking through those presents a positive image.”

Our experts have found that modernizing your accounts receivable collection system can drive top-line revenue as you can expand your market share by attracting new types of customers.

“If you accept check only, people of a certain age may have never owned a checkbook,” Fellows said. “It's not convenient to find your checkbook and write a paper check. It gets back to customer experience and working to expand it by making it simpler and providing multiple options for varying receivables.”

Starting The Accounts Receivable Automation Process

Sometimes it’s daunting to imagine tackling accounts receivable automation all at once, so I asked our team to talk about how some clients have approached it.

“It's different for every client, and it can vary a little bit based on industry,” Fellows said. “I'm working with an insurance company that receives a large number of paper checks. We're working on an electronic receivable strategy for them, so let’s walk before we run. The starting point for this company is to collect premiums from policyholders with an ACH. So any new policy holders they add, or any renewals, they’re making ACH an option on the setup form. There's an option to collect bank routing and bank account information to migrating more receivables automatically to electronic for any new clients. Then there will be a point in time where you look at who's remitting, who's paying by check, is there an option to capture more of those payments electronically? That’s an example of an industry where we see a lot of adaption towards electronic payments."

Kim Preston pointed out that any organization’s bank should work with them to develop a plan to move toward more efficient accounts receivable collection.

“We want to be an extension of your team,” Preston said. “So we work with you to identify where processes could be changed or improved, and then we help you with that. So it's not a case we're going to say, ‘Hey, you should do this,’ and you're on your own. We're in the trenches with you, whether it's even helping to train your staff, or the first run you do from an ACH collection standpoint, we'll work with you, and be a part of your team. That's where we set ourselves apart.”