Money sitting idle can cost your business when interest rates change and catch you unprepared. Understandably, tracking interest rate movements slides to the bottom of your priorities when you're managing operations and driving growth.

However, strategically managing your liquidity with interest rates in mind is a competitive edge hiding in plain sight, opening ways for your business to save and earn money. By partnering with a proactive Treasury Management team, you can capitalize on interest rate opportunities without needing to constantly monitor market conditions. This article will help position your company for effective liquidity management no matter which direction rates trend.

What’s The Cost Of Overlooking An Interest Rate Strategy?

Business leaders often don't realize what they're missing when they lack a proactive approach to interest rate changes. Here are just some of the lost opportunities:

Lost Interest Income. A business with $500,000 in cash reserves could miss out on tens of thousands of dollars annually by keeping funds in low-yield accounts during rising rate environments

Lost Interest Income. A business with $500,000 in cash reserves could miss out on tens of thousands of dollars annually by keeping funds in low-yield accounts during rising rate environments - Excessive Borrowing Costs. Companies without line of credit sweeps might pay thousands in unnecessary interest by borrowing while having idle cash in other accounts

- Delayed Capital. Businesses collecting receivables 15 days slower than possible effectively loan money interest-free to customers, sacrificing potential returns

- Vendor Discount Opportunities. Missing early payment discounts of 2% on $1 million in annual purchases costs $20,000 that goes straight to your bottom line

- Refinancing Windows. Failing to refinance a loan when rates drop by can cost your business by paying additional interest expense

- Investment Timing Advantages. Companies that can't quickly move capital miss the higher initial returns available when deploying funds early in rising rate cycles

- Foreign Exchange Costs. Businesses with international operations miss savings from strategically timing currency conversions based on interest rate differentials

How Do I Manage Cash More Effectively As Interest Rates Move?

While you can't control the Federal Reserve's decisions that affect interest rates, you can control how your business responds to them. Many companies miss opportunities because they don't have a flexible cash management plan that adapts to fluctuating interest rates. Businesses that implement proactive strategies can gain a financial advantage in rising and falling interest rate environments. Ideally, your bank’s Treasury Management experts review these and other items at least annually. Here's where we suggest you start:

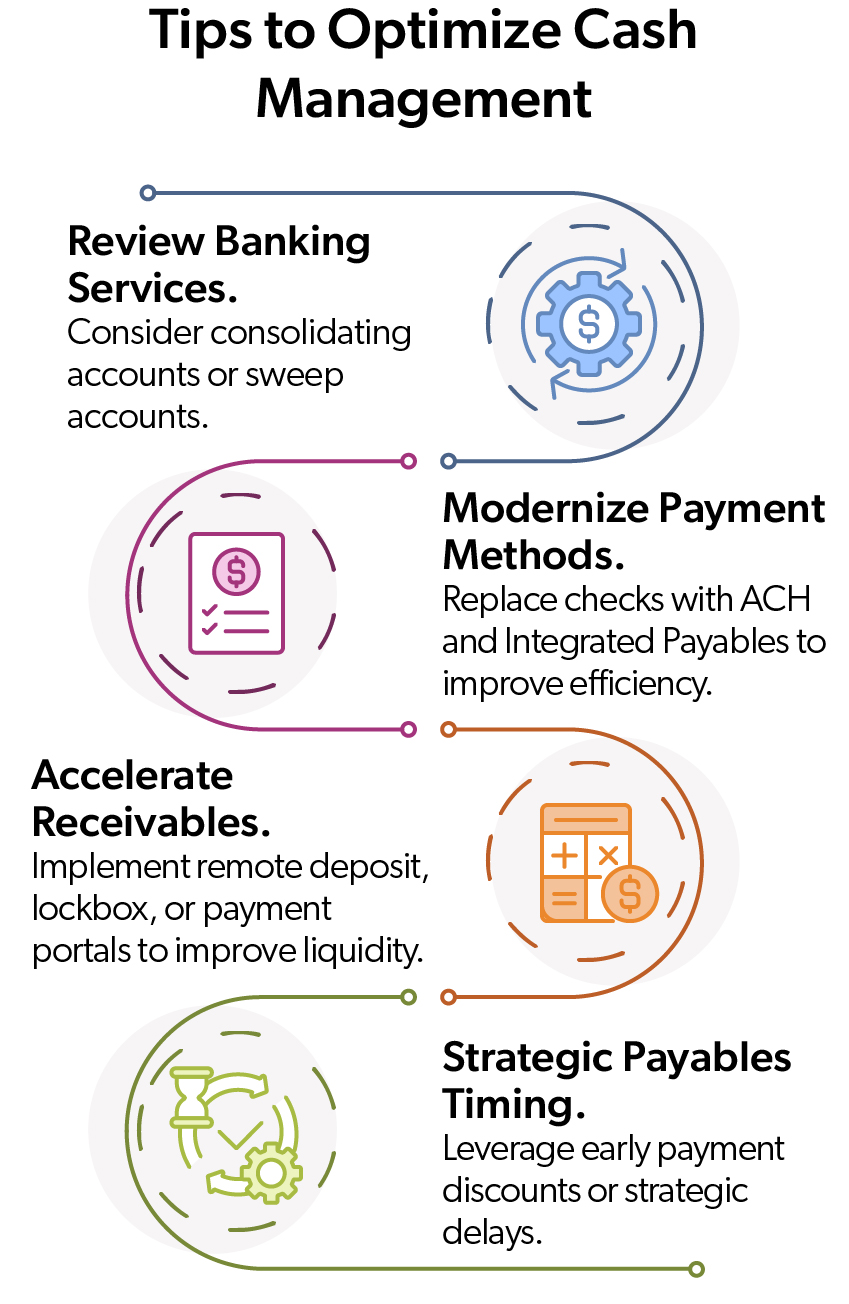

Review Your Banking Services. Begin with your monthly account analysis statement to identify potential savings. Do you have investment sweep accounts set up, and are they benefiting your business? Could consolidating bank accounts reduce your service charges? Reviewing your services helps to keep your banking structure aligned with current interest rate conditions.

Review Your Banking Services. Begin with your monthly account analysis statement to identify potential savings. Do you have investment sweep accounts set up, and are they benefiting your business? Could consolidating bank accounts reduce your service charges? Reviewing your services helps to keep your banking structure aligned with current interest rate conditions. - Optimize Payment Methods. Your payment strategy matters in any interest rate environment because it directly impacts your cash position, transaction costs, and how effectively you can capitalize on interest rates. If you're still writing checks, consider transitioning to ACH payments for lower processing costs and improved security. Banking solutions like Integrated Payables take the manual work off your team while improving your control over cash flow and strengthening your payment security. The efficiency gained allows you to maintain optimal cash balances that can be deployed strategically as interest rates fluctuate, ensuring you're neither over-exposed to low-yield accounts nor caught short when interest rates rise and investment opportunities emerge.

- Collect Receivables Faster. When money sits in your customers' accounts instead of yours, it's not working for your business. Faster collections mean more funds available for earning interest, offsetting fees, reducing debt, or funding growth initiatives. Consider implementing electronic receivables solutions like remote deposit capture to eliminate bank trips and deposit checks immediately. Lockbox services process payments the same day they arrive, while digital payment portals give customers convenient ways to pay electronically. For recurring billing, ACH debit arrangements ensure predictable timing, helping you optimize cash positions based on current interest rates.

Even simple policy changes can drive significant improvements: revise invoice terms from net-30 to net-15, offer early payment discounts of 2% for paying within 10 days, or establish clear follow-up procedures for aging receivables. Each day you accelerate collections adds value in any interest rate environment. - Timing Your Payables. Timing accounts payable can make a meaningful difference regardless of current interest rates. Ask vendors about early payment discounts as some may offer them but don't advertise it. Without discounts, strategize your payments based on terms and the interest rate environment. In rising interest rate environments, holding onto your cash longer allows you to maximize interest income or minimize borrowing costs. When rates are falling, strategically prepaying certain obligations might make financial sense if the savings outweigh what you could earn elsewhere. Your Treasury Management banking team can help analyze the true cost of capital in changing interest rate scenarios, finding the right balance between maintaining strong vendor relationships and optimizing your cash position to leverage current interest rate conditions.

How Can I Optimize Returns On Excess Liquidity During Rate Fluctuations?

As interest rates change, your investment approach needs regular attention. This isn't a "set it and forget it" scenario because what worked yesterday might not be optimal tomorrow.

When interest rates rise, you might consider laddering short-term CDs to capitalize on higher yields while maintaining liquidity. In a declining interest rate environment, longer-term instruments may help lock in current rates before they fall further.

For businesses with significant debt or capital-intensive operations, your Relationship Manager can discuss interest rate risk management tools. These might include interest rate swaps that let you convert variable-rate loans to fixed rates (or vice versa), or caps that protect against dramatic rate increases while allowing benefit from decreases. The right hedging strategy depends on your business size, debt structure, and risk tolerance.

Supply chain financing presents another opportunity to adapt to changing interest rates. During high-rate periods, buyers can leverage their stronger credit ratings to help suppliers access more affordable capital, strengthening critical vendor relationships. Your Treasury Management team can structure programs where your suppliers receive early payment while you maintain or extend your payment terms, creating a win-win scenario whose value shifts with interest rate cycles.

Some businesses leave their investment strategy on autopilot, missing chances to adapt. For example, excess cash that previously served you best in a money market account might now deliver more value by:

- Prepaying higher-interest debt

- Offsetting bank service charges through balance credits

- Funding a strategic acquisition while borrowing costs are favorable

If your business experiences significant cash flow variability, automated tools like line of credit sweeps can help optimize your cash position. These systems automatically move excess liquidity to reduce borrowed amounts when cash is abundant and draw on credit lines when cash is tight, minimizing interest expenses in rising interest rate scenarios.

Regular Banking Reviews Are Important in Any Interest Rate Environment

While you can't control Federal Reserve decisions about interest rates, you can control how your business responds to them. Building a strong relationship with your Treasury Management team creates a strategic advantage that creates advantages from interest rate fluctuations. When they understand your company's goals, they can help identify opportunities in rising and falling interest rate environments, spotting advantages others miss.

Businesses that thrive during interest rate fluctuations combine flexible financial strategies with advice from proactive, trusted banking partners. This collaboration turns market volatility into strategic opportunities, giving you a competitive edge regardless of which way interest rates move.