High interest rates can significantly reshape the dynamics and outcomes of selling a company in today’s competitive market. The consequences of high interest rates can be serious. Elevated rates often dampen buyer enthusiasm, recalibrate business valuation metrics, and alter financing structures. Before planning to sell a company, sellers should understand all the ways high interest rates can affect the process. In this article, we offer actionable insights for those poised to make strategic decisions in a high-rate environment.

Understanding the Impact of High Interest Rates When Selling A Business

Interest rates represent the cost of borrowing money, often expressed as a percentage of the principal amount. Central banks, like the Federal Reserve in the U.S., play a pivotal role in setting benchmark interest rates. Various economic factors, including inflation, unemployment, and overall economic growth, influence their decisions. By adjusting rates, central banks aim to stimulate borrowing and investment or cool down an overheated economy.

Elevated interest rates have historically narrowed the field of potential business buyers. Financing becomes more costly, which often suppresses sale prices and forces both sides of a transaction to adjust their strategies and expectations.

During the early 1980s, many countries, including the U.S., experienced soaring interest rates aimed at curbing inflation, which led to tightened credit conditions, reduced consumer spending, and stalled business expansions. Back then, it was expensive for companies to finance their growth, and potential buyers often faced prohibitive borrowing costs.

How High Interest Rates Impact Business Valuations

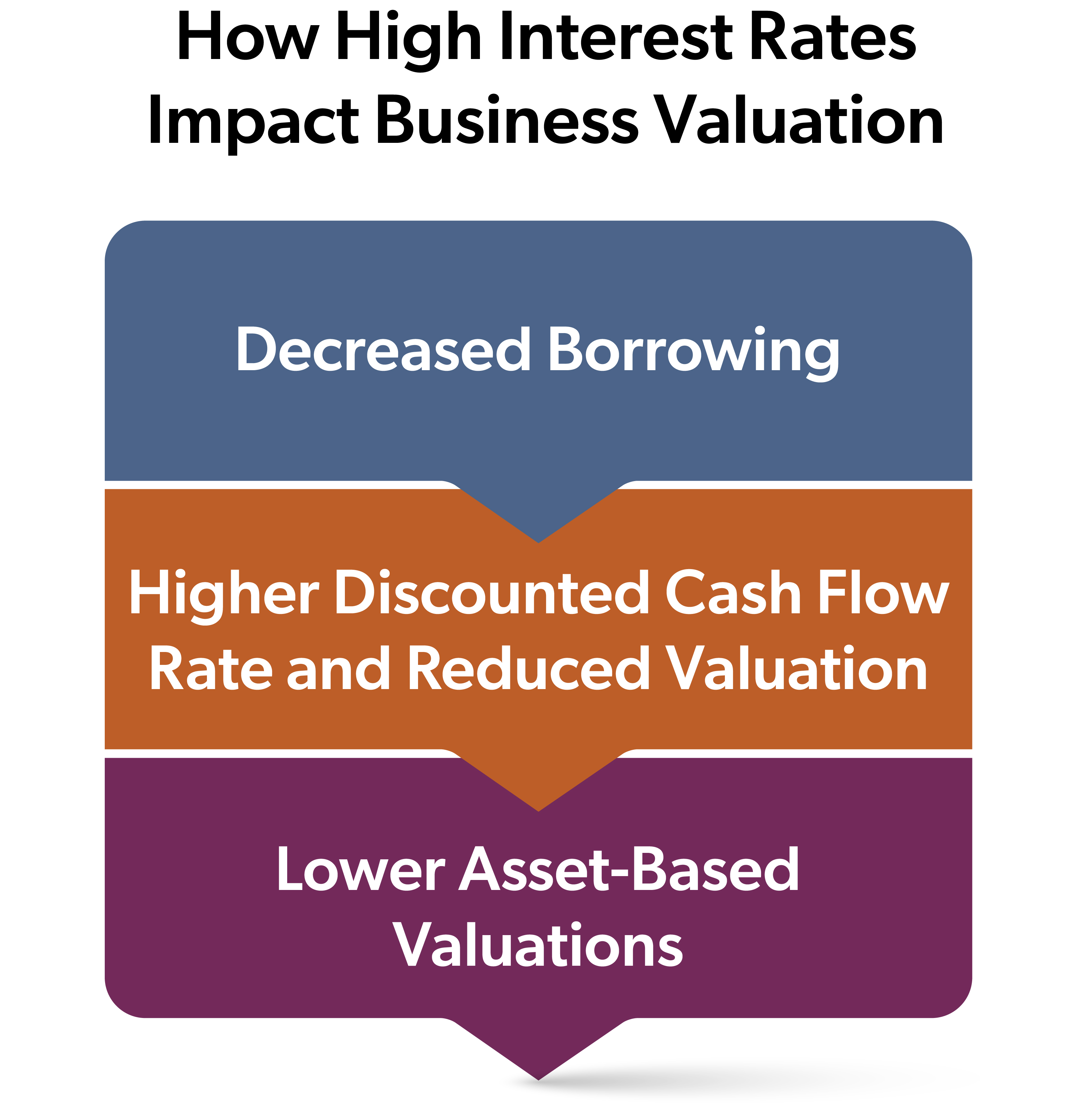

High interest rates introduce multiple challenges for business valuations, affecting both the financial and operational sides of a company. Rising rates directly shape three areas business owners need to watch closely: the cost of capital, projected cash flows, and the value of interest-sensitive assets. Each of these shifts can change what businesses are worth and what buyers are willing to pay. Business leaders preparing for a sale should understand how these forces work together and account for them well before going to market.

Decreased Borrowing: When interest rates rise, the cost of capital follows suit. This makes borrowing more expensive for potential buyers, often shrinking the pool of qualified acquirers. With fewer buyers able to secure the necessary financing, sellers may face longer times on the market or even downward pressure on price.

Decreased Borrowing: When interest rates rise, the cost of capital follows suit. This makes borrowing more expensive for potential buyers, often shrinking the pool of qualified acquirers. With fewer buyers able to secure the necessary financing, sellers may face longer times on the market or even downward pressure on price.

Higher Discounted Cash Flow Rate (DCF) and Reduced Valuation: One of the foundational business valuation methods is DCF, which calculates the present value of projected future cash flows. As interest rates climb, the discount rate used in these calculations typically increases. This results in a lower present value for future cash flows, often translating to reduced business valuations.

Lower Asset-Based Valuations: For businesses that rely heavily on interest-sensitive assets, such as bonds or certain types of real estate, high interest rates can erode the value of these assets. This can have a cascading effect on a company’s balance sheet, which factors into the overall valuation.

How Buyers & Sellers React To High Interest Rates

When faced with high interest rates, sellers may expect reduced valuations due to potentially limited financing options for businesses. At the same time, buyers, mindful of higher borrowing costs, might negotiate more aggressively or postpone transactions altogether.

These behavioral shifts, caused by economic cues, can fundamentally modify the dynamics and valuations in business transactions. Beyond the practical mechanics of financing and valuation, the psychology behind these decisions also shifts in a high-rate environment.

Behavioral economics can help us understand the impact of high interest rates on the perspectives of sellers and buyers. One key concept is the endowment effect — the tendency for people to value something more simply because they own it — leading sellers to overprice their businesses, especially in a high-interest rate environment when buyers are more risk-averse.

Another concept is called anchoring, which is the tendency for people to rely too heavily on the first piece of information they receive when making a decision. Anchoring can make it difficult for sellers to negotiate a fair price in a high interest rate environment. Given the recent surge in real estate and mergers, a seller may still reference comparative valuations that were near all-time highs in a low interest rate environment.

The Impact of High Interest Rates on Potential Buyers

Understanding the impact of high interest rates on buyers is important for business owners looking to sell their businesses, as it can help to tailor sales strategies, anticipate challenges, and identify the most suitable buyers in a high-interest-rate environment.

Buyer Financing: High interest rates consistently increase the cost of borrowing. This uptick deters some potential buyers altogether, especially ones who rely on external financing. For others, the steeper borrowing costs can limit the scale or ambition of their acquisitions.

A potential buyer focuses on certain measurements like Earnings Before Interest, Taxes and Depreciation/Amortization (EBITDA), profit margins, and Return on Equity (ROE). The higher the ROE potential, the more incentivized the buyer is to leverage (finance) the purchase. Buyers often only finance a purchase when there is “positive leverage.” Positive leverage is when the return on the investments is greater than the financing costs, with a comfortable margin to profit from. Even in a high interest rate environment, there still may be an opportunity for positive leverage. Therefore, it is important to understand your business reporting metrics. Key Performance Metrics (KPM), such as growing customer base or patented technology, communicate the value proposition.

Private Equity and Institutional Investors: These groups are typically known for leveraging financial mechanisms to fund acquisitions. In a high-interest-rate environment, their return-on-investment expectations might be more challenging to meet, which can cause them to be more cautious, potentially opting for fewer deals or looking for businesses with robust cash flows to offset higher financing costs.

This caution shows up most clearly in a shift away from leveraged buyouts (LBO), where buyers use significant debt to acquire a company. As borrowing costs climb, these deals lose much of their appeal. In their place, strategic acquisitions tend to gain ground. Buyers, often companies operating in related industries, look for synergies and longer-term value rather than the short-term financial returns that drive LBO activity.

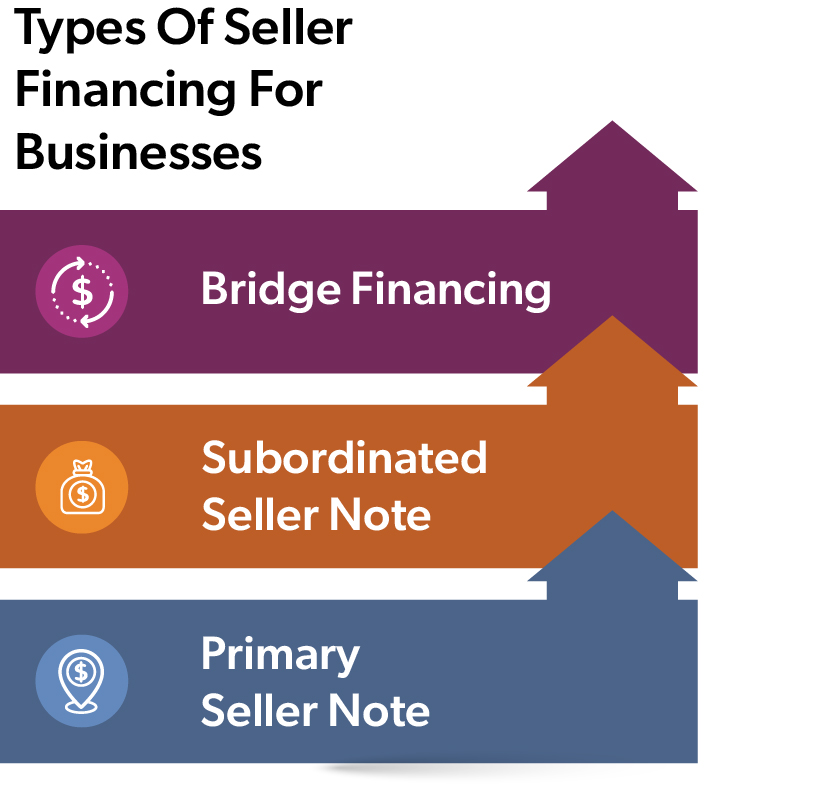

Seller Financing Options For Business Acquisitions: Sellers sometimes offer loans directly to buyers in an alternative lending arrangement called “seller financing.” This method can be particularly useful when high interest rates might make traditional bank loans less accessible or more expensive for potential buyers. The terms of seller financing, including the repayment schedule, interest rate, and the duration of the loan, are mutually agreed upon and documented in a promissory note — a binding legal document that outlines the buyer’s obligation to repay the seller according to the specified terms.

Seller Financing Options For Business Acquisitions: Sellers sometimes offer loans directly to buyers in an alternative lending arrangement called “seller financing.” This method can be particularly useful when high interest rates might make traditional bank loans less accessible or more expensive for potential buyers. The terms of seller financing, including the repayment schedule, interest rate, and the duration of the loan, are mutually agreed upon and documented in a promissory note — a binding legal document that outlines the buyer’s obligation to repay the seller according to the specified terms.

In a high interest rate environment, seller financing becomes a key negotiating tactic for closing business sales. It opens the door for buyers who might be edged out by traditional lending barriers and can offer a better return for the seller through interest income earned on top of the sale proceeds. At the same time, sellers should approach seller financing with a clear understanding of the risks involved and structure the deal carefully to protect their financial interests.

There are a few advantages of seller financing. Bypassing banks can create a straightforward transaction between seller and buyer, accelerating and streamlining the process. Also, the flexibility offered by seller financing can make a business more attractive to buyers, potentially allowing the seller to negotiate a higher price because the seller is providing a valuable service by easing the buyer’s credit burden.

At the same time, seller financing also presents some risks. For instance, there’s the possibility the buyer could default on their payments. Unlike traditional lenders, sellers may not have the same resources to assess buyers’ creditworthiness, which can increase the financial risk. Also, consider that seller financing means the seller has an ongoing financial stake in the business until the buyer fully repays the loan, which delays the final payout and emotional separation from the company.

Tips For Structuring Seller Financing Deals

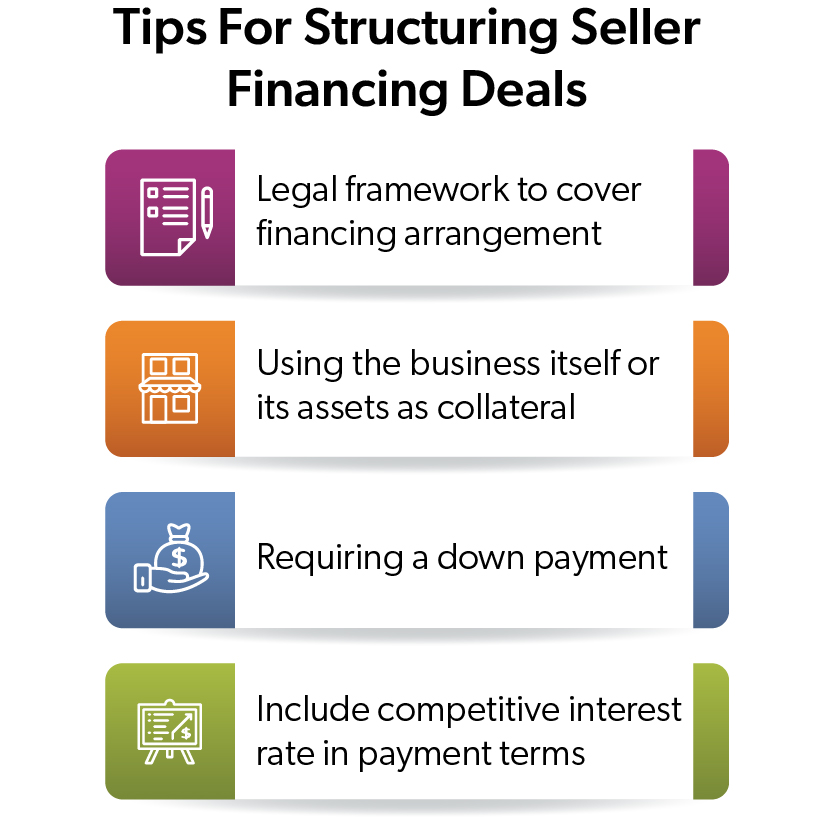

Legal Framework: A comprehensive legal agreement is crucial. It should cover every aspect of the seller financing arrangement, including recourse if the buyer defaults.

Collateral: Usually, the business itself or its assets serve as collateral, securing the seller’s interest. Should the buyer fail to meet the repayment terms, the seller can claim these assets.

Collateral: Usually, the business itself or its assets serve as collateral, securing the seller’s interest. Should the buyer fail to meet the repayment terms, the seller can claim these assets.

Down Payment: Requiring a down payment mitigates the risk of default by ensuring the buyer has substantial equity in the deal from the start.

Payment Terms: The terms should include a competitive interest rate reflective of the higher rates prevalent in the market and a realistic payment schedule. It’s also critical to spell out penalties for late or missed payments to maintain financial discipline.

Effectively structured, seller financing can be a powerful tool for sellers in a high-interest-rate economy, providing a balanced approach to selling a business while managing risk. In addition to financing terms, this also includes tax effects of how the deal is structured legally (i.e. stock sale vs. asset sale).

Owners selling a business who are contemplating this route should consult financial and legal experts to ensure that the agreement is both protective and fair, reflecting the interests of both parties involved.

Alternative Business Exit Strategies In High Interest Rate Eras

In periods of high interest rates, traditional exit strategies can become less effective or desirable for business owners who want to sell. Sellers might want to explore alternative options, such as:

Mergers and acquisitions (M&A) can provide greater financial stability, shared resources, and access to new markets. Aligning with companies that offer complementary strengths or resources can create a more competitive and financially sound entity, making it more resilient against economic turbulence.

Employee Stock Ownership Plans (ESOPs) transfer company ownership to employees through a trust. ESOPs allow employees to become owners, buying the business over time. This strategy not only ensures business continuity but also can boost employee morale and strengthen employee satisfaction and retention. ESOPs can provide tax benefits and can be an easier route for financing compared to traditional sales, especially when loan terms are unfavorable during times of high interest rates.

Delaying the sale until economic conditions improve can mean a better selling price. However, this decision carries the risk of market conditions worsening, potentially leading to lower business valuations in the future. Delaying a sale often means continuing to manage the company longer than intended, which might not be attractive to all business owners.

In each of these alternatives, business owners must balance immediate financial needs with long-term goals and the current economic landscape. A comprehensive understanding of each option, along with professional advice, can guide you in choosing the most suitable exit strategy in a high-interest-rate environment.

Selling a Business: How to Prepare for Sale in a High Interest Rate Climate

In a high interest rate environment, selling a business requires a strategic approach to make it appealing to prospective buyers grappling with expensive borrowing costs.

Preparing a business for sale in a high interest rate climate calls for a focused strategy. Sellers should tighten their financials and strengthen non-financial assets like brand reputation and customer loyalty to offset the borrowing hesitance buyers bring to the table. Flexibility on valuation and a clear read on current market dynamics matter as much as the financial fundamentals. Tips to prepare your business for sale in these challenging financial conditions include:

Streamline Operations: Optimize your business’s financials by reducing unnecessary expenses and focusing on efficient operations. A lean, financially sound business is more attractive, as it suggests lower risks and higher profitability for potential buyers.

Solid Financial Reporting: Ensure that all your financial statements and records are accurate, transparent, and up to date. Strong financial records reassure buyers of the business’s health and stability. There are many instances where solo entrepreneurs or family businesses may run additional expenses through the business as perks, but when preparing for a sale, review to ensure all expenses are business-related.

Highlight Intangible Value: When buyers scrutinize financial assets under the high interest microscope, intangible assets like a strong brand, loyal customer base, or an excellent reputation can be significant selling points.

Document Success Stories: Provide evidence of your business’s unique strengths, such as customer testimonials, case studies, or industry awards, which can enhance its perceived value.

Obtain a Business Valuation: Understand that the market value of your business might differ from your expectations due to the prevailing economic conditions. Conducting a professional business valuation can provide a realistic picture.

Flexibility in Pricing: Be prepared to negotiate on price. Flexibility can make the difference between closing a deal and having your business remain on the market for an extended period. However, be aware of your bottom line to avoid underselling.

By proactively addressing these areas, you position your business as a more compelling and secure investment, even when high interest rates add an extra layer of complexity to the selling process. Preparation, strategy, and working with your trusted advisors will help you navigate a sale or exit successfully.

Although the impact of high interest rates may lead to a slowdown in acquisitions or cause hesitancy, many businesses remain strong through the cyclicality of higher rates and are looking for the right buyer and opportunity.