Strategic liquidity management allows forward-thinking businesses to respond to market shifts in the most advantageous way. When a major opportunity arises — like a rush order from a key client — some businesses can jump on it immediately. Others have to watch competitors take the deal because they don't have cash readily available.

For small and mid-sized businesses, effective liquidity management creates a competitive advantage. By optimizing cash management, businesses can run with growth opportunities, negotiate better terms with suppliers, and hold steady through financial instability that might tank their competitors.

In this article, we'll explore practical strategies to strengthen your liquidity position, identify warning signs of potential liquidity problems, and leverage banking tools to efficiently manage your liquidity.

What Is Liquidity Management?

Liquidity management involves making sure a business maintains adequate cash and cash equivalents to meet short-term obligations while optimizing otherwise available funds. It's about balancing immediate access to cash that aligns with your short-term needs in an efficient, cost-effective manner.

Liquidity management is more important now because of several factors:

Economic uncertainty creates unpredictable cash flow patterns, making it harder to forecast with confidence. When market conditions shift rapidly, you may need to be able to access and deploy cash quickly.

Supply chain disruptions mean you might need to pay suppliers earlier, maintain higher inventory levels, or make different purchasing arrangements, which can constrain your liquidity position.

Interest rates have made it more costly to borrow while increasing the opportunity cost of cash sitting around. Finding a balance has financial implications in both directions.

Market volatility has many businesses seeking a liquidity cushion without locking up too much capital that could be used to grow or to manage through rough patches.

Small and medium-sized businesses have less room for error relating to liquidity management, when one major customer’s extended payment can strain cash reserves. Done correctly, liquidity management can protect a business while allowing leaders to capitalize on opportunities faster than competitors.

What Are the Hidden Costs of Poor Liquidity Management?

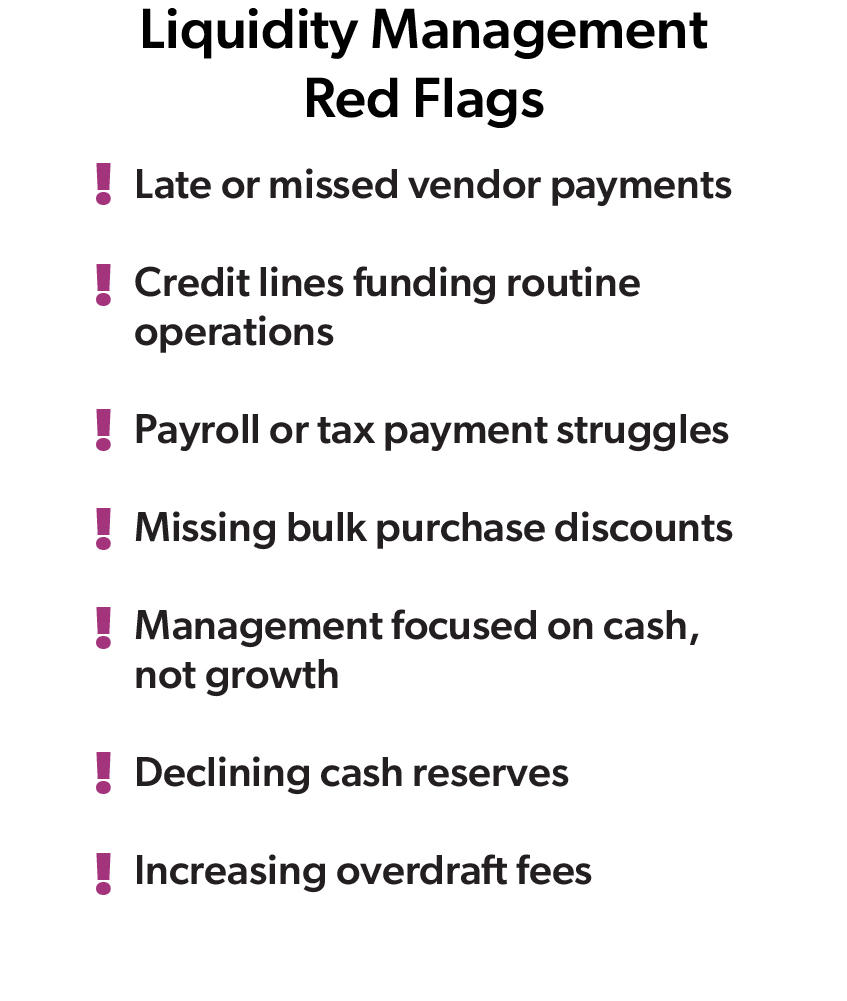

Liquidity shortages create cascading problems that affect immediate operations and long-term growth. Understanding these costs helps prioritize cash management improvements. When cash runs short unexpectedly, businesses face:

Higher financing costs. Emergency funding typically comes at premium rates, adding unnecessary expense.

Higher financing costs. Emergency funding typically comes at premium rates, adding unnecessary expense.

Lost supplier discounts. Many vendors offer early payment terms that come with significant annual savings.

Rush fees and expedited services. Scrambling to meet liquidity obligations often leads to paying premium prices for speed.

Beyond immediate costs, poor liquidity management can directly undermine a business’s competitive position and long-term viability as several situations can develop:

Missed growth opportunities. When a business can't move quickly to get new equipment, more inventory, or hire to meet increased demand, its competitors are still moving forward and taking those new opportunities.

Business relationships become strained. When payments to vendors are inconsistent, relationships falter. Top suppliers may prioritize more reliable customers, leaving businesses with second-tier options and terms.

Strategy falls apart. When reactive cash management changes leaders’ focus from growth initiatives to financial firefighting, this can create a cycle of catching up rather than moving ahead.

Recognizing these patterns early allows you to address the structural issues rather than merely treating symptoms.

Which Liquidity Management Strategies Drive Better Business Results?

Developing solid liquidity management strategies starts with increasing visibility and ends with practical action plans that don't require complex financial infrastructure.

Cash forecasting provides the foundation for all liquidity decisions. Start with a rolling 13-week cash forecast that tracks expected inflows and outflows to balance short-term accuracy with enough forward vision to make strategic adjustments. Effective forecasting includes tracking accuracy to improve future predictions, identifying seasonal patterns, creating scenarios for different economic conditions, and updating weekly rather than monthly.

Working capital optimization often reveals hidden liquidity through three key components:

Accelerating accounts receivable. Speed up payments received by implementing clearer payment terms, sending invoices promptly, offering early payment incentives, and following up consistently on overdue accounts.

Accelerating accounts receivable. Speed up payments received by implementing clearer payment terms, sending invoices promptly, offering early payment incentives, and following up consistently on overdue accounts. - Managing accounts payable. This involves timing payments to preserve cash without damaging vendor relationships. Improve overall liquidity by negotiating extended terms where possible while taking advantage of early payment discounts when annualized savings exceed cost of capital.

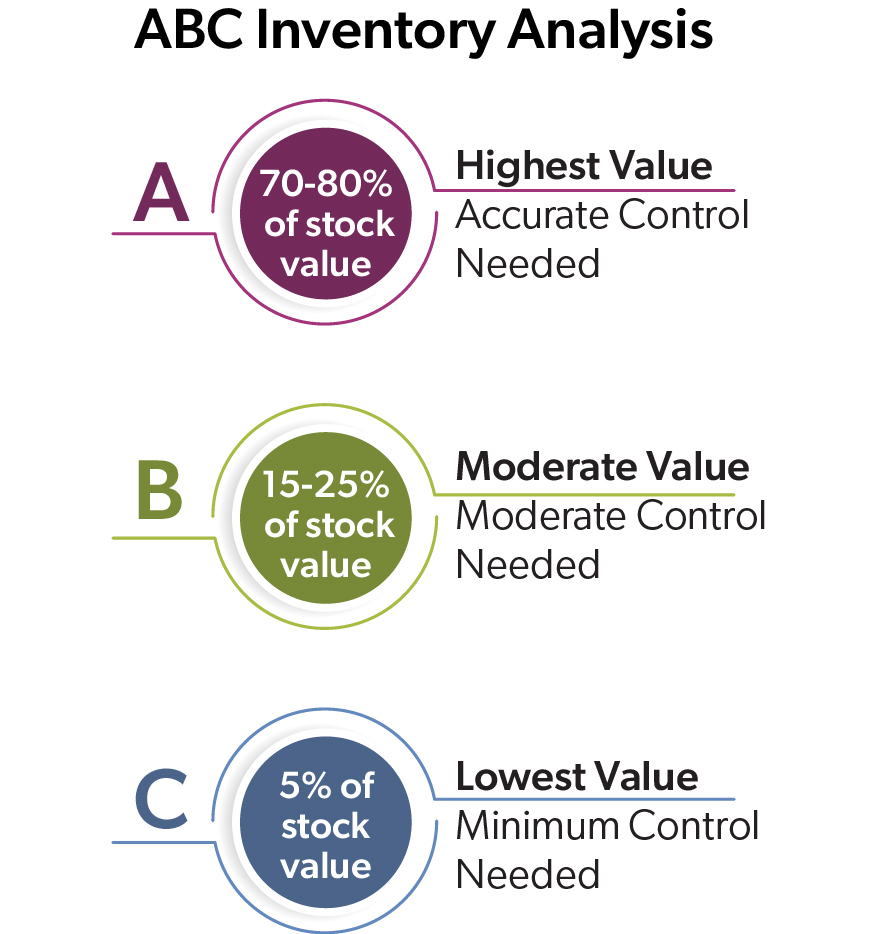

- Refine inventory management. Businesses free up significant liquidity through ABC analysis to focus tight control on high-value inventory, vendor-managed inventory for appropriate product categories, safety stock calculations based on lead time variability, and consignment arrangements with trusted suppliers.

Benchmarking liquidity metrics against industry standards helps identify improvement opportunities. Key metrics include cash conversion cycle, quick ratio, and operating cash flow ratio. Companies that consistently outperform their peers in liquidity management typically maintain better vendor relationships and respond quickly to market opportunities.

How Do Technology And Banking Tools Automate Liquidity Management?

Advanced treasury management solutions can help improve liquidity management without adding extra administrative duties by automating and streamlining cash management, giving businesses and organizations more control with less effort. For instance, businesses could incorporate these solutions into their liquidity management strategy:

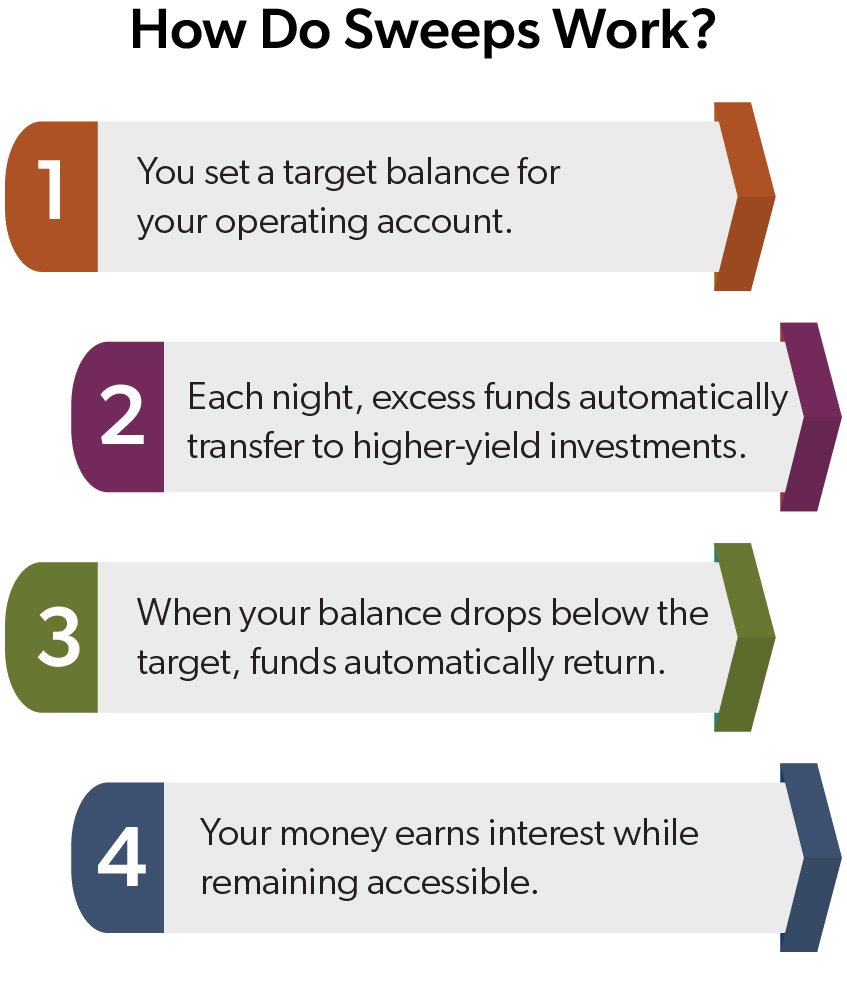

Automated sweep accounts eliminate manual transfers between accounts by automatically moving excess cash into interest-bearing investments overnight, then returning funds to operating accounts when needed. This automation uses money in a smart way while it remains accessible for daily operations.

Cash concentration solutions allow businesses with multiple locations to maintain local banking relationships while centralizing funds for better visibility and control. Each location maintains local bank accounts for depositing daily receipts, while centralizing funds as needed to a single operating account.

Two-way sweeps work particularly well with lines of credit. These arrangements monitor primary account balances and either pay down lines of credit with excess funds or draw from the line to cover shortfalls.

Two-way sweeps work particularly well with lines of credit. These arrangements monitor primary account balances and either pay down lines of credit with excess funds or draw from the line to cover shortfalls.

Zero-balance account structures reduce idle cash by linking subsidiary accounts to master accounts. Each subsidiary maintains a zero balance while the master account provides funds as needed – ideal for businesses with distinct divisions or expense categories requiring separate accounting but centralized cash management.

Digital dashboards provide real-time visibility into cash positions across all accounts and financial institutions. With a comprehensive view of liquidity, business leaders can identify concentration risks, track balance changes, monitor account trends, and set balance alerts based on predetermined thresholds.

Automated receivables management accelerates cash flow by streamlining the entire collection process. Electronic lockbox services capture check payments and match them to outstanding invoices. Benefits include reduction in days outstanding by 2-5 days, lower labor costs for payment processing, fewer misapplied payments, and less risk of check fraud.

Payables solutions, like integrated payables, help maintain control over cash outflows while maximizing efficiency. Virtual payment cards extend payment terms while providing suppliers immediate payment options.

When Should Businesses Consider External Liquidity Options?

Even with optimal internal liquidity management, most businesses benefit from strategically integrating external financing options that provide flexibility and growth capital.

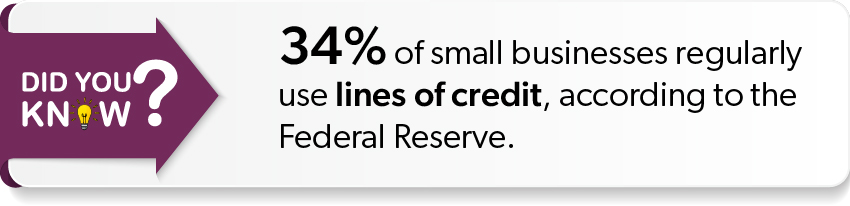

Lines of credit serve as valuable liquidity tools when used properly. Growing businesses often need additional working capital to fund inventory expansion or increased production before customer payments arrive. Lines of credit bridge this gap without disrupting cash flow or requiring permanent capital.

Lines of credit also provide protection during market volatility. When investment portfolios face temporary downturns, tapping a line allows organizations to avoid liquidating investments at unfavorable prices.

Trade finance solutions help businesses engaged in domestic or international trade manage timing mismatches between paying suppliers and collecting from customers. These specialized instruments include letters of credit, documentary collections, and banker's acceptances. For companies importing materials or finished goods, trade finance often provides more favorable terms than general-purpose lines of credit.

Creating A Liquidity Management Action Plan

Strategic liquidity management creates a strong platform for business growth and resilience. Business leaders looking to improve should:

- Calculate key liquidity metrics and compare to industry benchmarks

- Map cash flow cycles to identify bottlenecks and delays

- Evaluate if banking structures still fit business size and complexity

- Review recent cash shortfalls or surpluses to strengthen future forecasting

- Assess the integration between treasury management systems and accounting software

Partnering with treasury management experts who understand industry nuances helps identify the most appropriate solutions. Businesses that successfully manage liquidity seek banking partners who provide scalable solutions that grow with the business.