Your business is ready to grow, but your current space isn't. Whether you're a veterinarian who's found the perfect location for expanding your practice, a manufacturer needing to retrofit a facility, or a dentist planning a new office, your path forward requires construction project financing. Many growing businesses face this challenge: they need to invest in new construction and renovation, but traditional commercial construction loans require substantial down payments.

This is where SBA 7(a) loans for construction and renovation projects emerge as an ideal financing solution. SBA 7(a) loans offer flexibility and terms that align with small businesses' needs, making it possible to undertake significant construction and renovation with minimal down payment.

Which Businesses Qualify for SBA 7(a) Loans For Construction And Renovation?

While SBA 7(a) commercial construction loans work in any industry, they're particularly popular among:

- Healthcare providers (doctors, dentists, chiropractors)

- Veterinary practices

- Retail businesses

- Manufacturing operations

- Childcare facilities

- Professional service firms, like accountants and attorneys

What Are The Benefits Of SBA 7(a) Loans For Business Construction And Renovation?

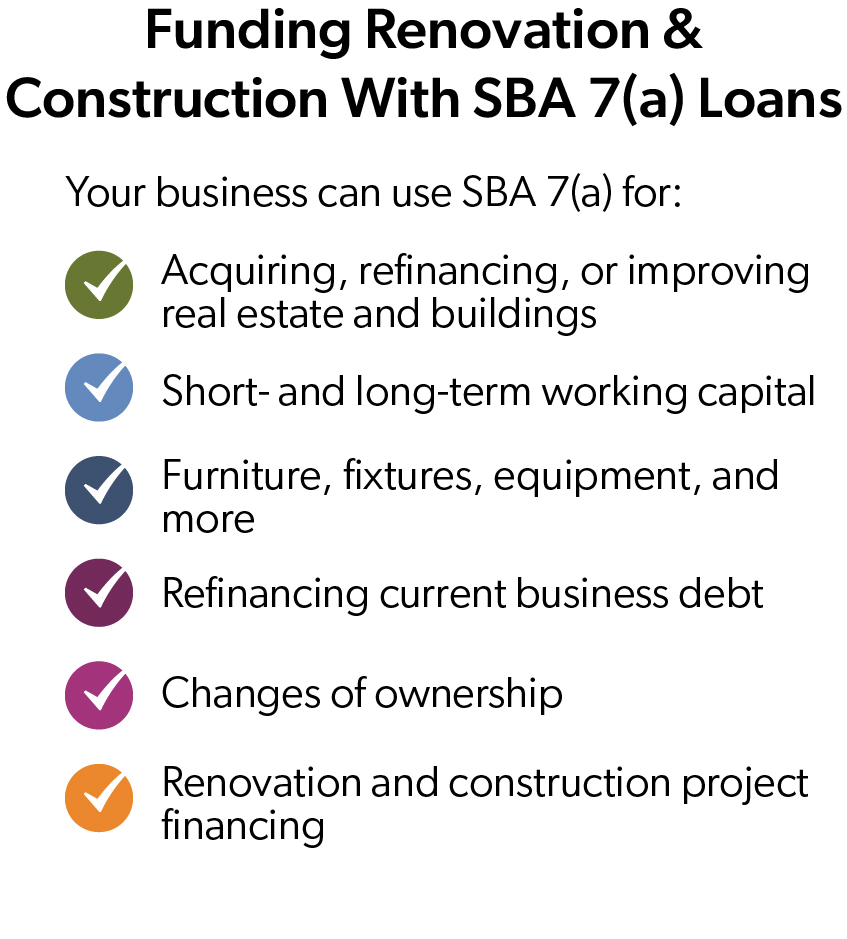

While SBA 504 loans and 7(a) loans can fund construction and renovation projects, many businesses prefer the SBA 7(a) loans program for its extra flexibility and cash flow advantages. SBA 7(a) loans allow you to finance needs beyond just real estate – including working capital, inventory, equipment, and furniture. Plus, while 504 loans require at least 10% down on the real estate portion, SBA 7(a) loans can offer down payments as low as 0%.

The SBA 7(a) loan program offers these advantages for your construction or renovation project:

The SBA 7(a) loan program offers these advantages for your construction or renovation project:

- Down payments as low as 0%, compared to 15-20% or more for conventional commercial real estate loans

- Ability to include working capital, furniture, and fixtures in the loan

- Built-in contingency funding for unexpected costs

- Interest payments can be wrapped into the loan during construction

- Professional third-party construction monitoring services

SBA 7(a) construction loans also consider your business's cash flow needs during the building phase. Unlike traditional loans that require immediate interest payments, SBA 7(a) loans can incorporate these payments into the loan amount during construction. This means you won't have to make payments until your new space is operational, which is important to maintain healthy cash flow during expansion.

Four Steps To Apply For SBA 7(a) Loans For Your Construction Or Renovation Project

Getting an SBA 7(a) loan for your construction and renovation project doesn't have to be complicated when you follow a proven process and work with an SBA-designated Preferred Lending Partner (PLP). Through years of helping businesses get SBA 7(a) loans for construction, we’ve developed a four-step process that guides you from initial planning through project completion.

Step 1: Planning Your SBA Real Estate Construction Project

You found the right building, so where do you start? Begin by gathering accurate bids from trusted architects and general contractors. Our SBA loan experts emphasize that it's very important to schedule physical site visits with these professionals to discuss your requirements in detail.

Even for smaller jobs and leasehold improvements, relying on estimates without thorough site walk-throughs can lead to inaccurate bids. This can result in unexpected delays, cost overruns, and complications with your SBA 7(a) loan and overall project. Taking time for proper planning gives you a solid foundation to proceed with your trusted SBA loan expert.

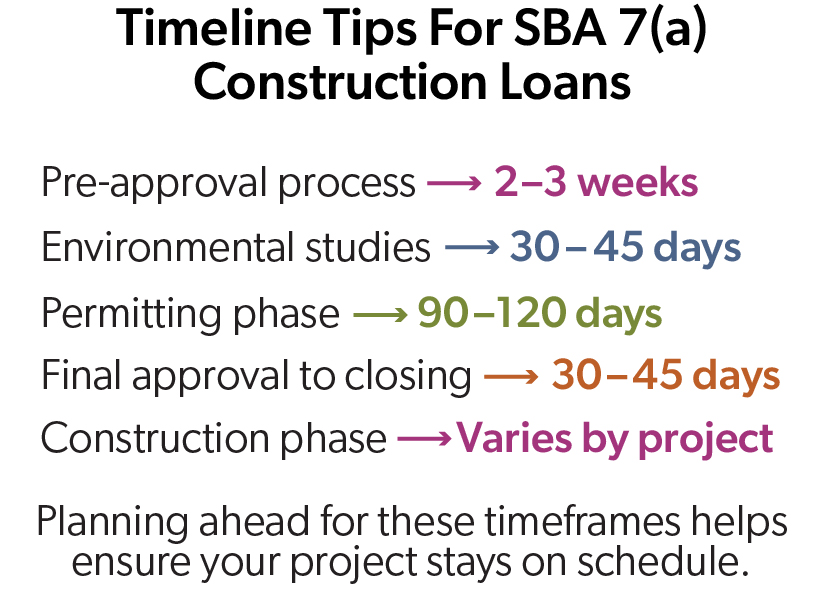

Step 2: Securing Pre-Approval for Your SBA 7(a) Loan For Construction

Start involving your SBA loan representative early – ideally while you’re gathering contractor bids. Sometimes business owners focus on project planning and are busy with daily business operations only to discover they've waited so long to meet with their lender that not enough time is now a problem.

Working with your SBA loan expert early in the project helps you avoid costly missteps in your construction project, like:

- Potentially spending thousands of dollars on environmental studies and traffic impact studies before you know if you qualify for financing.

- Permitting and zoning issues that might affect your budget — and could be identified earlier by working with your lender.

- Avoiding extra project costs because you’ll understand all the SBA requirements that might affect your project.

Step 3: Completing Your SBA 7(a) Commercial Construction Loan Permitting Requirements

Getting permits for your renovation or construction project is a critical step in the process that requires careful planning and patience. While your SBA loan expert conducts their due diligence during this stage, you'll need to address various municipal requirements and potential timeline challenges before your SBA 7(a) loan can close:

Municipal or industry-specific licensing requirements often introduce unexpected costs, such as mandatory sprinkler systems or accessibility upgrades that can add costs

Municipal or industry-specific licensing requirements often introduce unexpected costs, such as mandatory sprinkler systems or accessibility upgrades that can add costs - Your SBA loan expert will conduct thorough due diligence during the permitting phase, including contractor analysis, construction document and cost reviews, environmental reviews and appraisals

- Final loan closing should only occur after all required permits are fully secured and approved

This permitting phase often takes the longest in your SBA 7(a) construction loan process, but it's very important. Your lender will use this time to complete environmental studies, appraisals, and other due diligence requirements. While it might seem like a delay, this thorough approach helps prevent costly surprises and ensures a smooth transition to closing once all permits are in hand.

Step 4: Closing Your SBA 7(a) Loan & Launching Your Construction Project

With permits secured and due diligence complete, you'll close your SBA 7(a) construction loan and move into the construction phase. One of the most valuable features of SBA 7(a) construction loans is the third-party construction monitoring service that manages your project. This professional monitoring service:

- Performs comprehensive site inspections on a scheduled basis

- Delivers detailed progress reports to protect your investment

- Assists in contractor payment verification and documentation

- Allows you to maintain focus on your core business operations

With this structured oversight in place, your construction project has the professional support needed to stay on track and on budget. Regular monitoring also helps ensure your project meets all SBA requirements through completion.

How To Find The Best SBA Loan Expert for Construction Projects

The success of your construction project depends on working with an experienced SBA loan representative. When you’re decided between potential lenders for your construction or renovation project, consider these key factors:

- Look for an SBA PLP lender with successful construction and real estate expertise

- Check their track record with similar projects in your industry

- Confirm they offer dedicated support throughout the construction process

If you're considering a construction or renovation project for your business, start by assembling your project team and reaching out to an experienced SBA loan expert. The earlier you bring these experts into your planning process, the smoother your path to project completion will be.

Successful construction projects require a lender who understands the complexities of construction financing and can guide you through each step of the process. As a leading SBA Preferred Lending Partner, First Business Bank brings the expertise and dedication needed to help make your construction project a success.