The Private Wealth team at First Business Bank offers the following update to summarize the key points around the final IRS Regulations that impact IRA owners and beneficiaries taking distributions from inherited IRAs under the 10-Year Rule.

History of the Inherited IRA 10-Year Rule

In 2020, Congress eliminated the “stretch IRA,” which had allowed most beneficiaries of inherited IRAs to calculate and take their Required Minimum Distributions (RMDs) over their entire lifetime, thus deferring and minimizing taxes.

Instead, a new 10-Year Rule was adopted, requiring certain non-spouse beneficiaries to distribute the entire IRA balance by the end of the tenth year following the date of death of the original IRA owner. Most advisors and tax experts initially assumed the 10-Year Rule meant that an IRA beneficiary could take the IRA balance out of the account anytime within ten years of the death of the IRA owner but would not have to take an annual minimum distribution.

Instead, a new 10-Year Rule was adopted, requiring certain non-spouse beneficiaries to distribute the entire IRA balance by the end of the tenth year following the date of death of the original IRA owner. Most advisors and tax experts initially assumed the 10-Year Rule meant that an IRA beneficiary could take the IRA balance out of the account anytime within ten years of the death of the IRA owner but would not have to take an annual minimum distribution.

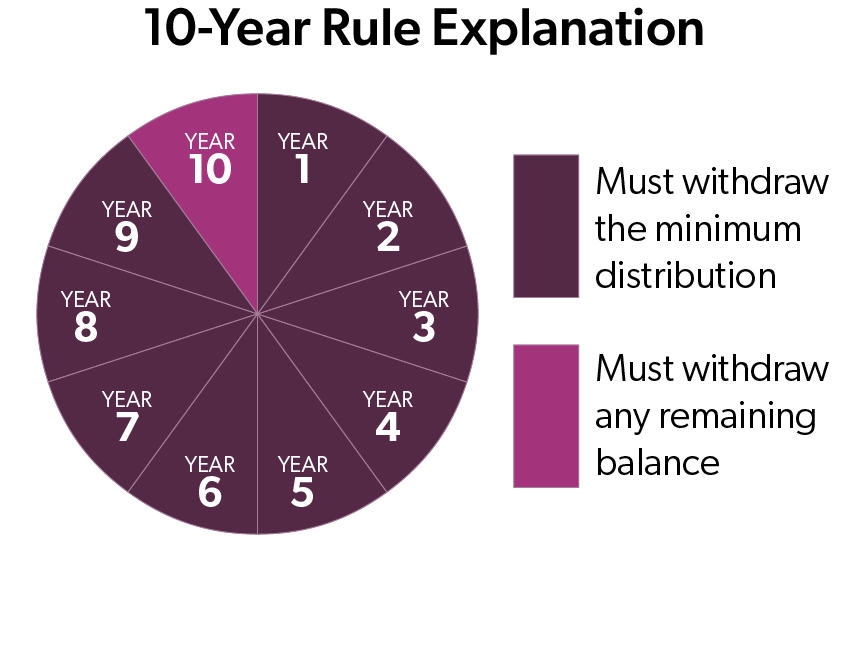

The IRS interpreted the 10-Year Rule differently, stating in their proposed regulations that annual RMDs are required during the 10-year period if the owner was already in RMD status at the time of their death. Thus, beneficiaries of IRAs would have to take a minimum distribution for nine years, with a final distribution of any remaining balance by the end of the tenth year. The IRS acknowledged that thousands of beneficiaries did not follow the distribution rule according to the proposed regulation from 2021 to 2024. Therefore, the IRS did not impose a penalty in those years for failure to withdraw a minimum distribution from an inherited IRA.

Final Regulations for Inherited IRA 10-Year Rule

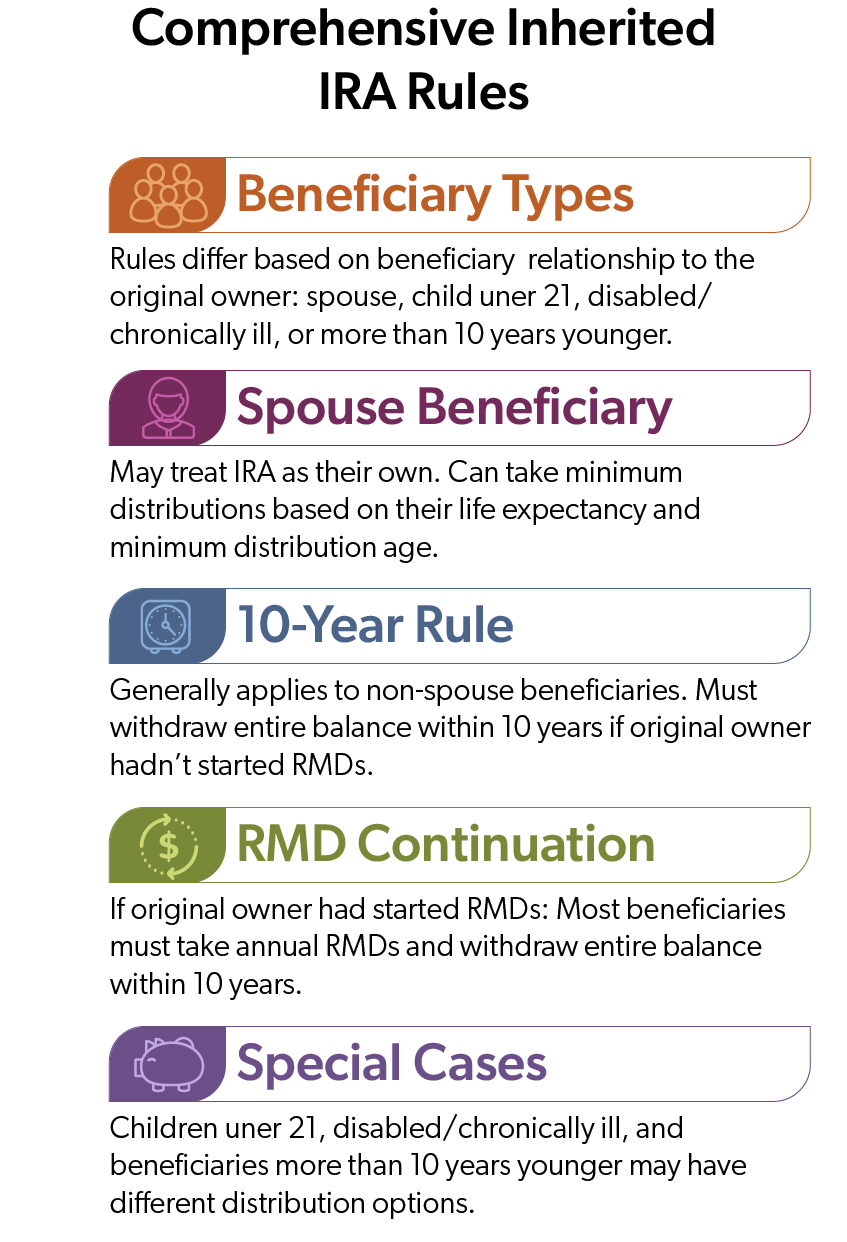

On July 19, 2024, the Department of Treasury issued final regulations to resolve the apparent ambiguity around RMDs and clarify that beneficiaries who inherit from an IRA owner who has already reached the minimum distribution age must take annual distributions during the course of the subsequent 10-year distribution period. Importantly, if the original owner has not begun taking minimum distributions, then beneficiaries can choose to take RMDs either based on their own life expectancy or the 10-Year Rule (this is similar to the old “stretch IRA” rules).

On July 19, 2024, the Department of Treasury issued final regulations to resolve the apparent ambiguity around RMDs and clarify that beneficiaries who inherit from an IRA owner who has already reached the minimum distribution age must take annual distributions during the course of the subsequent 10-year distribution period. Importantly, if the original owner has not begun taking minimum distributions, then beneficiaries can choose to take RMDs either based on their own life expectancy or the 10-Year Rule (this is similar to the old “stretch IRA” rules).

Note that different distribution rules apply to IRA beneficiaries who are spouses, children under 21, disabled or chronically ill individuals, and those who are more than ten years younger than the IRA owner. For example, a surviving spouse may treat the original IRA as their own and take out minimum distributions based on their life expectancy and minimum distribution age.

No Inherited IRA RMD Penalties in 2024

The good news is that in 2024 there will be no penalty for beneficiaries who did not follow the proposed regulations regarding distributions from Inherited IRAs. For minimum distribution purposes, the final regulations will only apply for calendar years beginning on or after January 1, 2025.

IRA distribution rules can be complex and vary based on individual circumstances. Whether you have a tax-deferred IRA, an inherited IRA, or are planning for future distributions, it's important to understand how these rules apply to your unique situation. For personalized guidance on managing your IRA distributions effectively, we encourage you to reach out to First Business Bank's Private Wealth team. Our experienced advisors can help you navigate these rules and develop a strategy tailored to your financial goals.

Updated: 9/12/2024