Explore This Report With These Links

- U.S. Economy Slows in Q1

- Consumer Spending Trends in 2023 and 2024: A Closer Look

- Manufacturing PMI Rebounds

- Federal Reserve Turns More Hawkish

- Inflation Remains Stuck In The Mid-3% Range

- Housing Market Stalls

- Jobs Market Remains Solid

- A Deeper Dive on the Employment Picture

- U.S. Consumer Spending Insights

- Global Growth Poised For Improvement

- Market Commentary

Executive Summary

The U.S. has seen solid economic activity and a sturdy labor market even as inflation has trended more slowly toward the 2% target. Recent indicators suggest that economic activity has continued to expand at a solid pace, with gross domestic product (GDP) expanding at an annualized rate of between 1.5% and 2%. Both consumption and investment are advancing at a moderate pace. Hiring continues to be strong, and wage gains are outpacing inflation. Inflation has eased over the past year but remains elevated. Should inflation continue to moderate, we can likely anticipate that the first rate cut will come later this year. So far, the Fed’s Federal Open Market Committee is assessing the data one month at a time, and any upward inflation surprise could push rate cuts further down the road.

Equity markets continue to advance, with the large-cap markets outperforming again in the quarter. Market breadth narrowed in as the technology and communications services sectors again asserted dominance. Bond yields have trended higher as the timeline for a Federal Funds rate reduction is extended. Bond returns on the short end of the yield curve were positive, with higher levels of income overcoming modest price declines. The Bloomberg Aggregate Bond Index, a proxy for intermediate maturity bonds, was up in the recent quarter but flat for the year to date.

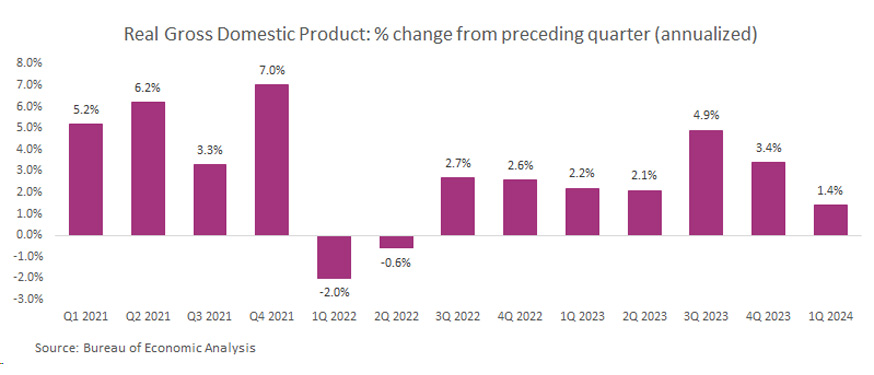

U.S. Economy Slows in Q1

Annualized GDP growth in the first quarter was 1.4%. The slower pace of growth in the first quarter reflected decelerations in consumer spending, exports, state and local government spending, and a dip in federal government spending. Imports rose by 6.1%, which reduced GDP growth by .65%. These declines were partly offset by a strong acceleration in residential fixed investment and higher nonresidential fixed investment. Consumer spending on health care, travel, and entertainment continues to grow strongly. However, spending on non-durable goods, such as food and clothing, was lower in April than in December, suggesting that lower and middle-income households are feeling the squeeze on discretionary income.

Early estimates and recent data suggest real GDP growth of roughly 2% in the second quarter, continuing a growth trend that is well above the Federal Reserve’s estimate of the long-run growth potential of the U.S. economy, currently projected to be 1.8%. The economic expansion, which started after a short but steep pandemic-induced recession, has now entered its fifth year. While growth has been stronger than expected and inflation is more stubborn to tame, the broader trend is of an extended expansion driven by strong consumer demand and fixed-investment spending. This growth is particularly remarkable given the widespread recession fears of the last two years. With an extended period of positive real wage growth and significant recent gains in wealth, consumer spending should continue to drive the expansion forward into 2025. Fixed-investment spending has been amazingly resilient in the face of higher interest rates and tighter lending standards. This resilience largely reflected healthy corporate balance sheets, federal government incentives, and a surge in demand for artificial intelligence (AI)-related technology. This also could continue into 2025, providing the potential for continued moderate economic expansion in the absence of a major shock.

Consumer Spending Trends in 2023 and 2024: A Closer Look

In 2023, personal consumption expenditures (PCE) within the GDP accounts rose by 2.2%. However, the quarterly breakdown reveals interesting dynamics. PCE consistently increased by more than 3% in every quarter except 2Q23, during which it grew by a modest 0.8%. 2023 achieved a healthy balance between goods spending (up 2%) and services spending (up 2.3%). Consumers continued to allocate funds toward durable goods, with spending in that category rising by 4.2% for the full year. Non-durable goods spending also saw a modest increase of .8% during the same period.

However, 2024’s first quarter presented a different narrative. PCE increased by 1.5%, but challenges emerged beneath the surface. Consumer spending on goods declined by 2.3% compared to 4Q23 levels. Durable goods spending experienced a sharp 4.5% decline — the steepest drop since 3Q21 when pandemic-related stimulus payments and supplemental unemployment benefits were winding down. Non-durable goods spending also dipped by 1.1%. On the other hand, consumer spending on services remained robust, rising by 3.3% in 1Q24.

Evidence would suggest that consumers are becoming more selective about their discretionary spending. Consumers are feeling pressured by the rising costs of rent, vehicle insurance, debt-service payments, and other unavoidable non-goods expenses that are squeezing their take-home pay. These financial pressures affected big-ticket purchases like cars and appliances while also impacting smaller-ticket goods such as apparel and personal electronics. Additionally, restaurant spending moderated after the initial post-pandemic surge when people were eager to venture out. Retail spending was up 0.1% in May but was weaker than expected. On a year-over-year basis, sales were up 2.3%.

Over the past two years, consumer spending has been supported by an increased use of credit. However, consumer credit, which rose by 9.9% in the year that ended in April 2022, rose only 1.9% in the year that ended in April 2024. Consumer total debt balances stand at $17.6 trillion as of the first quarter, with mortgage debt representing around 70% of that balance. A significant majority of outstanding consumer debt is at a fixed rate much lower than new loans, which has ultimately allowed consumers to be more resilient in this rate-hiking cycle. This is particularly true of higher-income consumers. For the one-third of households that rent their accommodations, rents continue to represent a larger share of disposable income than pre-pandemic, forcing consumers to economize in other areas.

Strong growth in both employment and real wages has led to solid year-over-year gains in real disposable income since the start of last year. Wages have been increasing at or above the rate of annual inflation since April 2023. Inflation has increased by 22%, based on CPI, in the four years ended in May 2024, compared to only a 6.8% cumulative increase in the previous four years (2016 to 2020). Cumulatively, over the last eight years, inflation has risen 31%. Increases in average hourly earnings outpaced inflation from 2012 to 2021 when a rapidly rising rate of inflation temporarily overtook wage gains. This inflationary pay cut persisted until April 2023, when cooling inflation restored a positive wage gap. In eight years, from May 2016 to May 2024, wages increased by 37%, outpacing inflation increases by almost 6%. But consumers are not feeling nearly as good about bigger paychecks as they are feeling bad about higher costs for everything.

Manufacturing PMI Rebounds

Manufacturing activity, as measured by the S&P Global U.S. Manufacturing Purchasing Manager Index (PMI), declined early in the second quarter but rebounded by June. Preliminary indicators show that the manufacturing PMI rose to a three-month high in June. The reading signaled an improvement in business conditions within the goods-producing sector for a second successive month. New orders and employment made increasingly positive contributions, with manufacturing payrolls rising the most in 21 months. Selling-price inflation eased to a six-month low, and input inflation also slowed. Higher raw material costs were reported related to shipping, with supplier delivery times also lengthening for the first time in five months. Despite broad improvement, business optimism fell to the lowest level in 18 months. Manufacturers’ concerns centered around the demand environment in the months ahead as well as election-related uncertainty, notably relating to policy.

Federal Reserve Turns More Hawkish

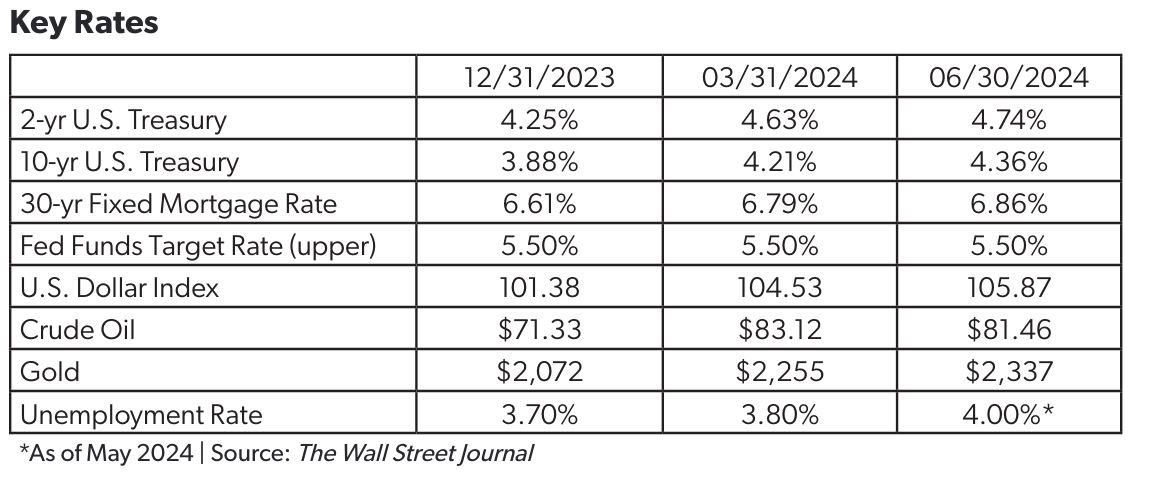

The Federal Reserve held rates steady in June, in a range between 5.25% and 5.5%, as was widely expected. The rate remains at its highest level since 2000 and is above the long-term average of 4.4%. The decision came only hours after the Labor Department reported that inflation, as measured by the Consumer Price Index (CPI), was essentially flat in May and up 3.3% from a year earlier. The latest core PCE Price index reading (the Fed’s favorite metric) was 2.6%, the lowest annual rate in three years. Yet despite progress, both measures are still well above the Fed's target of 2.0%, and the slope of the downward trajectory has flattened lately. That is a problem for a central bank that failed to raise rates when inflation shot higher in 2020-2021 and would eagerly like to restore credibility. Also, the Fed appears to be trying to balance the positive impact of restrictive inflation policy versus the negative impact of inflation on low- and moderate-income earners. Fed Chair Jerome Powell noted “pretty good progress” on inflation but stated that they would need to see more good data to feel comfortable initiating rate cuts. The majority, 15 of 19 officials, anticipate one to two 0.25% rate cuts in 2024, versus the prior forecast of three, a decidedly more hawkish tone. Bond traders are still betting on two cuts before year end.

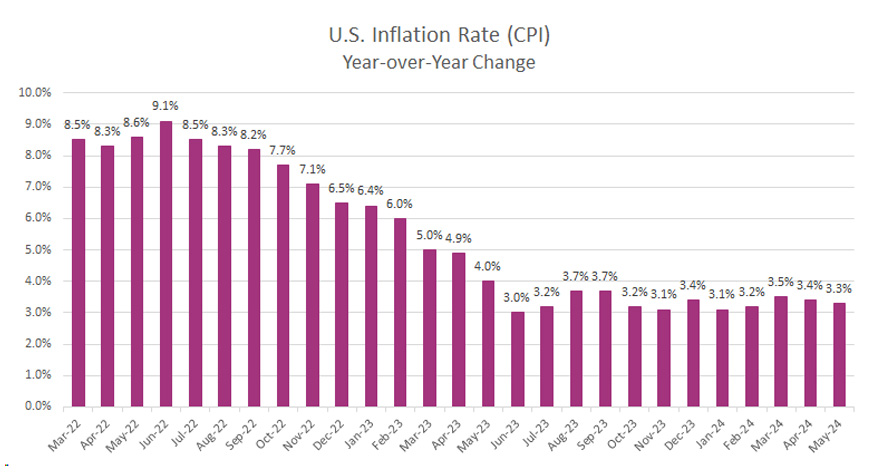

Inflation Remains Stuck In The Mid-3% Range

The CPI was unchanged in May after rising 0.3% in April. Prices are 3.3% higher compared to a year ago. Since hitting a year-over-year low of 3% in June of 2023, the CPI has remained stuck in the mid-3% range, buffeted about by volatility month to month in energy prices, food away from home, and core goods. Another reason for this slightly hotter-than-expected inflation is stubbornly strong shelter inflation. After declining by 2% from 8.2% year over year in March of last year to 6.2% in December, it only fell a further 0.8% by May of this year, to 5.4%. The shelter category is expected to continue easing based on newly negotiated rents. Remember that owners’ equivalent rent of residences (OER) and rent of primary residence (rent), which account for about 35% of the CPI basket, are sampled only every six months. Some negative contributors to rising costs, like skyrocketing auto and homeowner insurance rates, are considered to be temporary factors.

The Producer Price Index (PPI) increased 2.2% year on year in May 2024. Increases in PPI averaged 3.1% from 1950 until 2024, reaching an all-time high of 19.6% in November of 1974 and a record low of -6.9% in July of 2009.

Housing Market Stalls

In April, home prices reached another record high despite rising mortgage rates and increased home supply. You would expect this dynamic to cause prices to weaken, but today’s housing market is unlike any other in recent history. Home prices set another record in April, even as mortgage rates rose and the supply of homes for sale increased. The average prices of single-family houses with mortgages guaranteed by Fannie Mae and Freddie Mac increased by 6.3% in May 2024 and are 49% higher than early in 2020. Prices continue to be supported by an imbalance in supply and demand. With the exception of home prices, most other indicators from the housing economy are well below past peaks. Housing starts and permits peaked in the 2020-21 timeframe, with permits for all of 2021 reaching 1.74 million. In May, the permits seasonally adjusted annual rate was 1.39 million, and housing starts, which peaked in the 1.60 million range in 2021, were reported at 1.28 million. Housing inventory is at a 3.7-month supply, while a mere six-month supply is considered a well-balanced market between buyer and seller. This would indicate a very bearish environment for housing prices, but that is not the dynamic of today.

Rising home prices, followed by mortgage rates near 7%, are pushing prospective buyers to the sidelines and could be a drag on second-quarter GDP as millions have been priced out of the market. Fannie Mae’s Home Purchase Sentiment Index fell to an all-time survey low in May. Many would-be buyers expressed optimism early in the year that mortgage rates would trend lower, and the current sentiment reflects the pent-up frustration with the lack of purchasing power. Housing starts are tracking 1.32 million units annualized for the second quarter, down from 1.46 million a year earlier. Based on recent data, residential fixed investment is poised to decline by an annualized 1.3% in the second quarter after 15.4% growth in the first quarter.

For renters, even though rent growth is slowing due to a big increase in new apartment units this year, prices are still 26% higher than they were in 2020. Half of all renter households — more than 22 million — spent more than 30% of their income on housing, which is considered “cost-burdened” by Harvard’s Joint Center for Housing Studies.

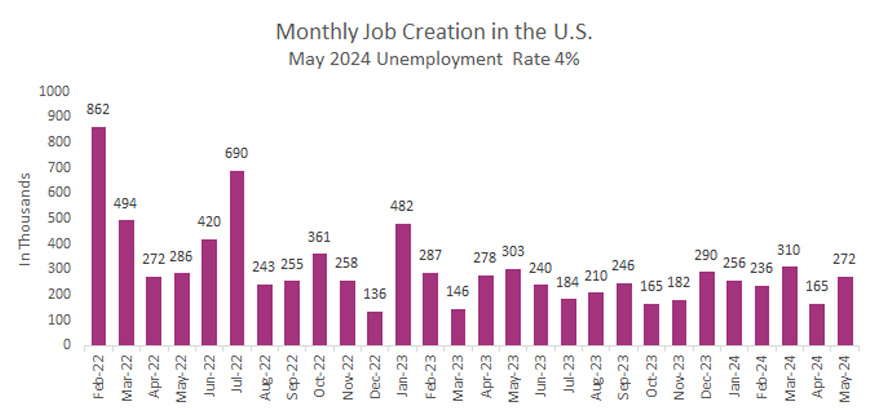

Jobs Market Remains Solid

In a further sign of economic resilience, job growth exceeded expectations in May. The labor market remains more robust than many expected, creating an average of 248,000 net new jobs each month this year through May. One caveat to the strong report was the unemployment rate, which reached 4%. The unemployment rate at the end of 2023 was tied for a 50-year low of 3.5%. Despite the increase, it should be noted that 4% is a historically low number. The unemployment rate has been at or below 4% for 30 months, a milestone last achieved during the Vietnam War in the late 1960s and the Korean War in the early 1950s.

Job openings were down in April to an estimated 8.1 million, the lowest reading since February of 2021. The ratio of job openings to persons looking for work, which has been as high as 2 to 1 since the pandemic, stands at 1.25. Layoffs are steady at around 1%. The big picture shows a still-healthy labor market that is slowly softening.

A Deeper Dive on the Employment Picture

When analyzing the economic environment, published economic data can sometimes present conflicting narratives. A prominent example of this is the U.S. Bureau of Labor Statistics (BLS) monthly Employment Situation report. This closely monitored report incorporates data from both a household survey and an establishment survey.

The establishment survey reports employer data from approximately 119,000 nonfarm establishments, representing 629,000 worksites. According to this payroll survey, the economy added a substantial 2.8 million new jobs over the past year. However, the household survey, which provides data on the labor force, employment, unemployment, persons not in the labor force, and labor force characteristics, shows a more modest increase of 376,000 workers during the same period. The wide disparity between the two results is directly linked to the differing data collection methods.

It's important to note that the household survey data is estimated based on a monthly sample survey of 60,000 households. As with any survey-derived data, there may be biases due to self-reporting, opting out, sample bias, and exclusion of underrepresented populations. The household survey measures employed individuals and is derived from a smaller sample size. In contrast, the establishment survey measures employed individuals, counting multiple job holders twice. Given the evidence, it appears that the establishment survey may be providing a clearer picture of the labor market’s health, supported by other indicators showing strong gains.

Small companies are the backbone of the U.S. economy. According to the Small Business Administration, small businesses create an estimated 1.5 million jobs annually. Based on data from the U.S. BLS, businesses with fewer than 250 employees contributed 55% of the total net job creation from 2013 to 2023 and accounted for an estimated 44% of the private sector employment. A recent National Federation of Independent Businesses (NFIB) report on employment states that an exceptionally high number of small businesses are still struggling to fill open positions, with many small business owners reporting job openings they could not fill in May. Overall, 60% of small business owners reported hiring or trying to hire in May. 51% of owners and 85% of those hiring or trying to hire reported few or no qualified applicants for the positions they were trying to fill. Despite hiring challenges and other headwinds in the form of higher borrowing rates and higher prices, small business optimism is holding steady.

Global Growth Poised for Improvement

Outside the U.S., the European economy is expanding once again, with its best quarter since Q3 2022. Activity in China is stabilizing, and the global goods cycle is showing signs of improvement. As U.S. growth moderates while other regions improve, global growth looks set to be well-supported and more broadly based. Improving conditions globally have created some near-term divergence between the Federal Reserve and most G-10 central banks.

In early June, the Bank of Canada lowered its benchmark interest rate by 25 basis points to 4.75%, its first downward move in four years. The Canadian central bank noted that "with continued evidence that underlying inflation is easing, the Governing Council agreed that monetary policy no longer needs to be as restrictive." Consumer price inflation in Canada decelerated to 2.7% in April, still above their 2% target. The Canadian economy added 27,000 jobs in May, yet unemployment still rose to 6.2%. Meanwhile, Canada's GDP grew by a slower-than-forecasted 1.7% in the first quarter after growing only 1% in the fourth quarter.

Despite a slight upside surprise in May’s preliminary inflation data, inflation in Europe has stabilized since February, remaining relatively flat and below levels seen in the United States. The European Central Bank (ECB) began hiking rates in August 2022, five months later than the Federal Reserve. Since then, both central banks have largely raised rates in tandem. In June, the ECB diverged from its usual alignment with the Federal Reserve and cut rates by 25 basis points to 3.75%.

China is the second-largest economy in the world, with an estimated GDP of $17.9 trillion. Since China began to open and reform its economy in 1978, GDP growth has averaged over 9% per year. China’s strong growth has been based on investment and export-oriented manufacturing, an approach that has largely reached its limits and has led to economic, social, and environmental imbalances. Reducing these imbalances will require a shift from manufacturing to high-value services and from investment to consumption. In recent years, growth has moderated in the face of structural constraints, including declining labor force growth, diminishing returns to investment, and slowing productivity growth. Following moderate post-pandemic growth of 5.2% in 2023, growth is projected at 4.5% in 2024.

Market Commentary

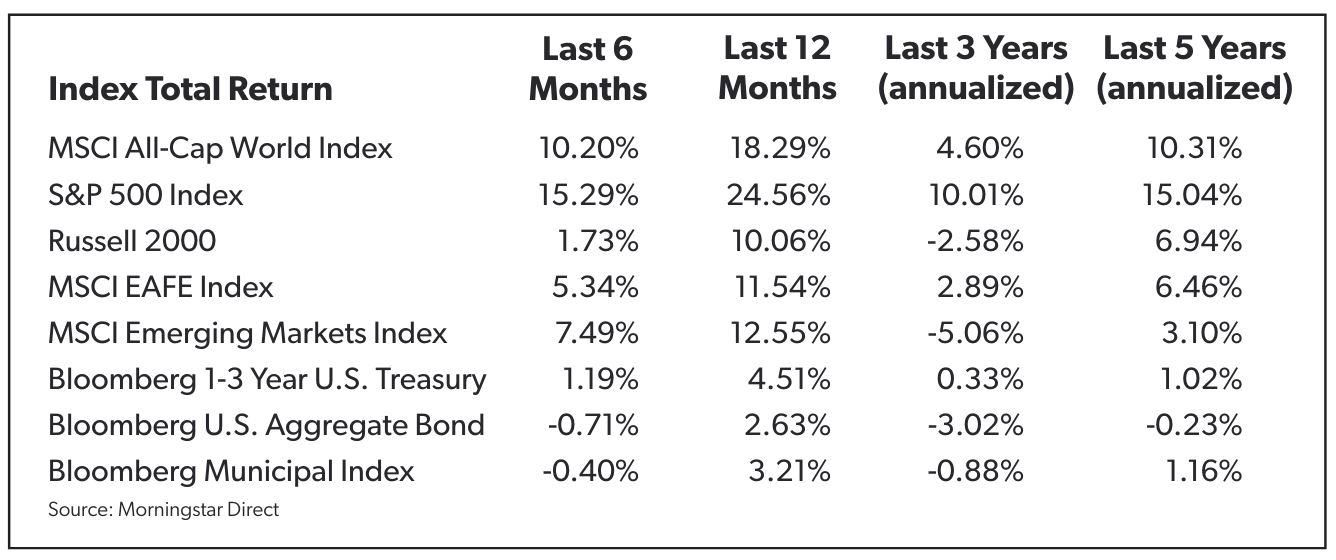

The large-cap market, as measured by the S&P 500, had a strong start to the year, logging 33 new all-time highs since January 1. At the mid-year point, the year-to-date total return for the S&P 500 is 15.3%; the tech-heavy Nasdaq is up 18.6%; and the Russell 2000 small-cap index is positive by 1.7%. International markets have posted decent, low double-digit returns in local currency. However, due to a strong U.S. dollar, those returns translate to mid-single digits for U.S. investors. The developed markets are up 5.3% for the year to date, and emerging markets are up 7.5%. The MSCI All-Cap World Index, which is an excellent proxy for a globally diversified portfolio, is up 10.2% for the year.

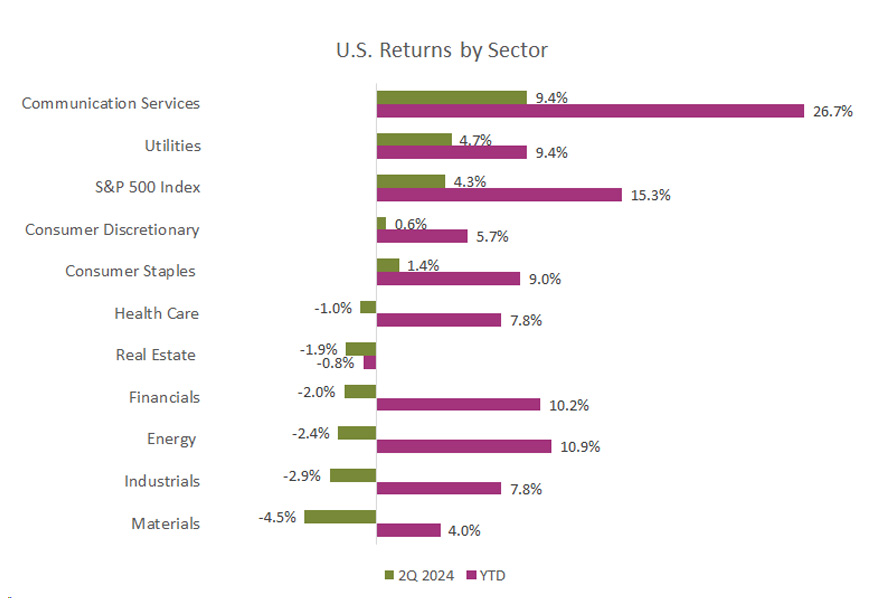

One dynamic in the second quarter was the narrowing of the market advance. Exiting April 2024, eight sectors were approximately tracking the S&P 500's year-to-date gain. As of mid-year, two sectors — Information Technology and Communication Services — are pulling away with 28.2% and 26.7% year-to-date gains. While Utilities and Energy are delivering low-double-digit total returns for 2024 to date, both lag the S&P 500 by more than six percentage points. And every other sector is even further behind the broad market return.

The first half can also be characterized as having a lower level of market volatility. The S&P only experienced seven trading days with declines of greater than 1%, and the market has now gone 340 trading days without a decline of 2% or greater in a single trading session. The CBOE Volatility Index (VIX), which measures market expectation of near-term volatility as conveyed by stock index option prices, is trading near the lowest levels seen over the last ten years.

Accelerating earnings growth is preventing the market from stretching into deep overvaluation territory even as stocks repeatedly hit new highs. The 1Q24 earnings season is winding down. With 98.2% of a market cap having been reported, the current estimate for S&P 500 operating earnings is growth of 4.7% year over year. Across sectors, information technology and communication services are expected to have another strong quarter, while resilient consumer demand should support the consumer discretionary sector. Revenues, supported by resilient economic activity and solid inflation, are expected to be the largest contributor to operating earnings growth, although margins will play an increasingly important role as momentum slows.

The tech rally has added to the concentration of the few largest companies, with Nvidia, Microsoft, and Apple worth almost $10 trillion combined, which was the value of the entire S&P 500 as recently as 2010. In fact, the individual market cap of Microsoft, Apple, or Nvidia exceeds the cumulative value of all stocks in Germany, France, and the United Kingdom, as measured in U.S. dollars. Only India, Japan, and China have stock markets bigger than each of these companies individually. In June, Nvidia briefly topped the $3.3 trillion mark and surpassed Microsoft to become the most valuable public company in the world before losing some steam at month’s end. The “Magnificent Seven” (Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia, and Tesla) continue to outperform with year-to-date performance as a group of 33% year to date. The rest of the S&P 500 index, minus those seven, is up 5%.

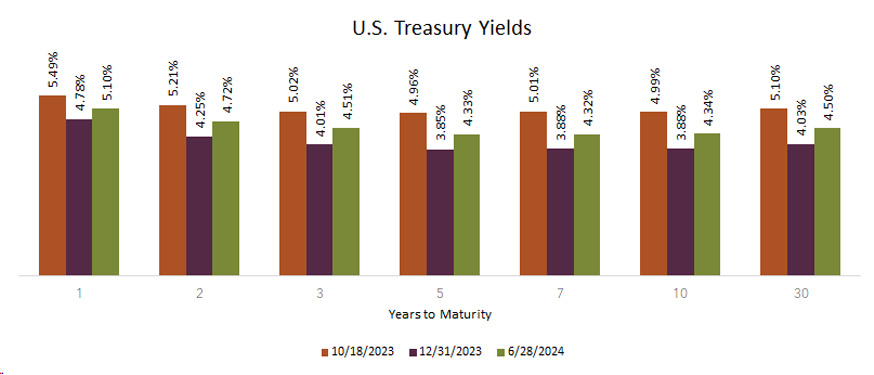

In the bond market, rates trended higher in the first half as the timeline for rate reductions changed significantly from year end. The yield on both the 2-year and 10-year Treasury notes rose by 40 basis points since the start of the year. The chart below illustrates where yields are as of the end of June as compared to both year-end 2023 and mid-October of 2023, which represents the recent peak in rates.

The yield curve remains inverted by around 40 basis points. June marks the 24th consecutive month of yield curve inversion without a recession, the longest streak on record. Bond indices posted mostly positive returns in the quarter. The Bloomberg 1-3 year U.S. Treasury index is up 1.2% for the year, and the Bloomberg Aggregate Bond index is off by .26%. The municipal market continues to be supply-constrained. The intermediate maturity Bloomberg Municipal index is down .4% year to date.

Within the last quarter, we initiated an evolution of our fixed-income portfolios to include a floating-rate income fund. The strategy we selected is designed to complement the existing traditional fixed-income portfolio by increasing portfolio yield with a selectively constructed portfolio of senior-secured loans. Our portfolios remain overweight in equities, although fixed income does offer a more attractive opportunity to generate income in today’s rate environment. In our equity portfolios we are very modestly reducing small-cap and developed international to enhance our emerging international participation. While emerging has underperformed, we believe that relatively depressed valuations offer an attractive longer-term opportunity. We expect these changes to result in both an increase in future returns as well as a reduction of overall portfolio volatility.

The wild economic ride triggered by the pandemic and the policy response, which was characterized by enormous swings in output, unemployment, and inflation, has mostly abated. While our base case is that the economy continues to modestly expand, inflation trends lower over time, and the labor market slowly softens, we are also cognizant of the lingering potential for economic disruption. Some of the most significant disruptions have occurred due to unforeseen events, including the pandemic and September 11th. As we contemplate the future, potential risks to the soft-landing scenario include policy missteps, geopolitical conflict, weather-related events, and a resurgence in inflation.

The 2024 presidential election adds an element of uncertainty to the investment landscape. Top of mind for investors are the policy decisions that loom for either administration. The tax cuts from the 2017 Tax Cuts and Jobs Act are set to sunset at the end of 2025. These cuts simplified individual income taxes and reduced tax rates across income levels. This is a gnarly issue because extending the cuts will increase debt, but allowing the cuts to expire could hurt growth. Budget deficits, as projected by the Congressional Budget Office, are expected to be nearly $2 trillion in 2024 and $22 trillion over the 2025-2035 period. Trade and immigration are also key issues for both campaigns.

As we conclude our Q2 market review, it's important to highlight key developments within the Midwest that reflect broader economic trends. In Wisconsin, We Energies is making a significant $34 million investment in a new service center in West Bend, signaling strong infrastructure growth and job creation (BizTimes - Milwaukee Business News). Meanwhile, the acquisition of Waukesha-based metalworking distributor ApTex by a New York firm highlights the ongoing trend of strategic mergers and acquisitions reshaping local industries (WisBusiness).

In Kansas City, the U.S. Conference of Mayors recently held its 92nd Annual Meeting, bringing together over 200 mayors to discuss crucial issues such as housing, public safety, and economic growth (United States Conference of Mayors). This event underscores Kansas City's role as a significant hub for policy and economic discussions, reinforcing the city's strategic importance in the region.

These developments across the Midwest demonstrate the region's resilience and adaptability. Drawing inspiration from the innovation and perseverance seen across the Midwest, we look forward to helping our clients to be prosperous and successful. Please feel free to reach out to our team of advisors so that we may help you achieve your goals.