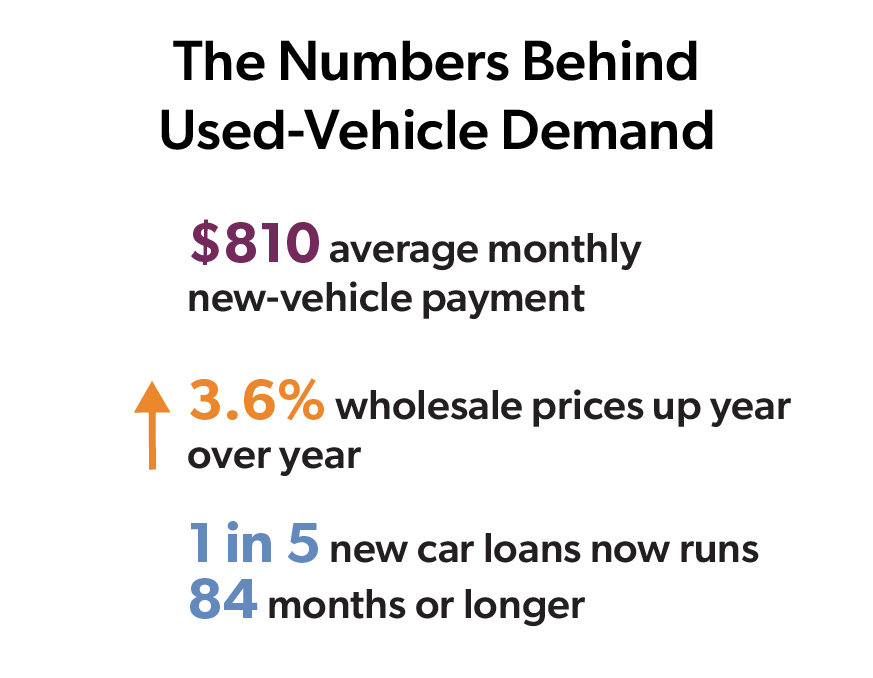

The math on new vehicles stopped working for a lot of buyers, and independent dealers are seeing that on their lots. According to recent data from the NIADA, May marked the auto market's first year-over-year gain of 2026, with wholesale prices up 3.6% year over year — strong conditions that also raise some floorplan decisions worth addressing while the market is in your favor. We put the numbers in context and address the strategy questions here.

When wholesale values rise, the margin between what you pay at auction and what you sell for compresses, and that pressure lands directly on your floorplan. Here's what the May data tells us and what to do about it.

Why Are Buyers Landing On Used Car Lots Right Now?

Affordability is doing most of the work. According to JD Power, the average new-vehicle monthly finance payment reached $810 in May, up 2.8% year over year, even as loan rates eased to 6.59%. More buyers are stretching into 84-month-plus terms to make the numbers work. When a buyer is already extending a loan to six or seven years to afford a new vehicle, pre-owned inventory becomes the smarter choice with more value.

New light-vehicle sales reached a seasonally adjusted annual rate of 16.1 million units in May, up 3.1% from a year earlier, but the year-to-date SAAR of 15.7 million remains down 4.5% from last year. That gap is partly a distortion because a significant share of buyers pulled purchases forward in early 2025 to get ahead of auto tariffs, inflating last year's comparison numbers. The underlying demand picture is more stable than the year-to-date figure suggests.

New light-vehicle sales reached a seasonally adjusted annual rate of 16.1 million units in May, up 3.1% from a year earlier, but the year-to-date SAAR of 15.7 million remains down 4.5% from last year. That gap is partly a distortion because a significant share of buyers pulled purchases forward in early 2025 to get ahead of auto tariffs, inflating last year's comparison numbers. The underlying demand picture is more stable than the year-to-date figure suggests.

Tariffs on imported vehicles and parts have pushed new-vehicle prices higher with no clear path to reversal, sending more buyers toward pre-owned inventory. That demand has staying power. Plan your inventory strategy with that in mind.

Powertrain trends are diverging as well, with hybrids reaching 15.2% of year-to-date new-vehicle sales. Buyers who want a hybrid and can't afford a new one are looking for used alternatives. If your lot carries hybrid inventory and prices it well, that's a demand source worth understanding and sourcing toward.

What Do Strong Wholesale Values Mean for Your Floorplan Line?

Here's where the good news on values gets more complicated. Rising wholesale prices mean the vehicles on your lot are worth more, but you also paid more to acquire them. Your floorplan line needs to reflect that reality, or you may be carrying more risk than you think.

A few specific floorplan pressure points:

Line utilization. If wholesale acquisition costs have risen 5-10% over the past year and your floorplan line hasn't moved, you're effectively carrying fewer units than your line was designed to support. That's a financing structure problem. Review your line size relative to what you're paying at car auctions today, not what you were paying 18 months ago.

Curtailment exposure. In a strong wholesale market, vehicles hold value longer, which can create a false sense of security about aging inventory. But when values soften, units that have been sitting 60 or 90 days become a problem fast. Strong markets reward dealers who turn inventory quickly. Know your average days-to-sale by vehicle segment and hold yourself to a discipline around it, even when the pressure feels lower.

Auction sourcing strategy. With analysts holding to a 16.0-million-unit full-year new-vehicle forecast and strong resale values, the window to stock the right inventory is open. But elevated wholesale costs mean sourcing decisions at auction carry more weight. Overpaying for a unit that fits the lot is a smaller problem in a rising market, but it becomes a bigger one when values flatten. Price discipline at acquisition, not just at the point of sale, protects margin when conditions shift.

How Should You Think About Vehicle Inventory Mix in This Market?

Independent car dealers have always had to make sharper inventory decisions than franchise stores, but this market raises the stakes on vehicle inventory mix.

Buyers migrating from new vehicles tend to have clearer expectations about condition, mileage, and pricing transparency. A well-presented, well-priced used vehicle at a credible dealership can close faster than it would in a softer market, but only if the inventory matches what buyers in your market are looking for. Stocking toward demand, not just toward availability, can be the difference between a lot that turns four times a year and one that doesn't.

The tariff environment adds complexity here. As new-vehicle prices stay elevated, buyer interest in lower-mileage, late-model used vehicles tends to increase. These units cost more to acquire, but they also command stronger retail prices and tend to turn faster. If your current mix skews older or higher-mileage than it used to, scrutinize whether that’s a deliberate strategy or a sourcing habit.

Does Your Floorplan Partner Understand This Market?

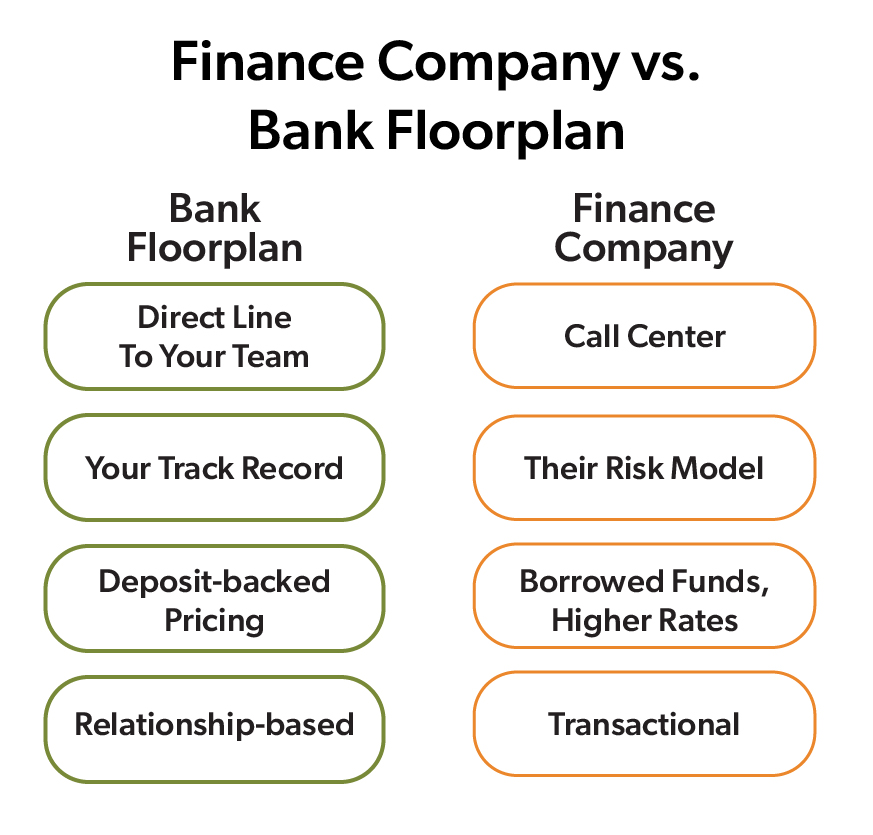

Not every floorplan lender reads the same data you do — or, frankly, reads it at all. Dealers who work with captive finance companies or independent floorplan providers often find themselves managing a line with little strategic input and no one on the other end who understands inventory cycles, seasonal demand patterns, or what a sustained move in wholesale values means for their specific operation.

The difference shows up most clearly when the market is moving and you need to act fast. A bank floorplan partner with 30 years of auto industry experience speaks your language, knows your business, and can help you make better decisions without having to explain the basics every time you call. When you need to adjust your line, tighten your turn targets, or move on an auction opportunity, you reach a person who already knows your dealership — not a call center.

The difference shows up most clearly when the market is moving and you need to act fast. A bank floorplan partner with 30 years of auto industry experience speaks your language, knows your business, and can help you make better decisions without having to explain the basics every time you call. When you need to adjust your line, tighten your turn targets, or move on an auction opportunity, you reach a person who already knows your dealership — not a call center.

There's also a distinct pricing advantage you can’t overlook. Banks fund floorplan lines from FDIC-insured deposits, which carries a structurally lower cost of funds than finance companies that borrow to lend. That difference flows directly to your rate. For elite independent dealers who have built a track record, bank floorplan pricing can be meaningfully better than what a captive or independent finance company offers — and you get the stability of a regulated financial institution.

That stability matters more than it might seem. A floorplan partner backed by a publicly traded bank with $4.3 billion in assets isn't going anywhere. Your line, your relationship, and your access to decision-makers are there when you need them.

Three Floorplan Questions To Answer Before The Market Shifts

The May data is encouraging, but it also sets up a decision point. Strong wholesale values and steady retail demand don't last indefinitely, and the dealers who use this window well come out of it with tighter operations, better-aligned floorplan lines, and stronger lender relationships.

A few questions to think about now:

- Is your floorplan line sized for what you're paying to acquire inventory today?

- Are your turn rates where they need to be to protect margin if wholesale values soften?

- Do you have a floorplan partner who proactively brings you this kind of market perspective?

With strong resale values and well-priced used stock positioning independent dealers well heading into summer, the conditions are favorable. The question is whether your financing structure and your lender relationship are set up to help you take full advantage of them.

Last updated: 6/23/2026