Gain Adequate Cash Flow To Pay Employees And Suppliers & Service Debt On Existing Long-term Obligations

As market volatility and other signs of potential economic slowdown continue to rear their heads, many business owners are beginning to prepare for financial headwinds. In fact, a recent study of more than 300 companies shows that more than two-thirds of manufacturers are preparing for an economic downturn. Among those preparing, they are doing things like trying to increase production efficiency, reducing inventory levels, and shying away from new long-term capital commitments.

Alongside this data, the Federal Reserve conducts a Small Business Credit Survey every year, which includes more than 6,500 responses from small businesses with 1-499 full or part-time employees from across the country. The latest survey shows that 64% of employer firms faced financial challenges in the previous 12 months. Reading this, it struck me that the top challenges often can be alleviated with accounts receivable factoring.

Otherwise known as accounts receivable financing or invoice financing, factoring helps many types of businesses ensure they have adequate cash flow to pay employees and suppliers, service the debt on existing long-term obligations, and more. If you are ever waiting on pins and needles for your customers to pay invoices, factoring can be a better way to run your finances. As you can imagine, a factoring agreement is smart to put in place before any kind of economic downshift. Reliable, timely invoice payments can be the difference between surviving and thriving.

Here’s how factoring addresses the Federal Reserve’s Small Business Credit Survey’s reported top four challenges:

1. 40% had trouble paying operating expenses

How Factoring Helps: Factoring addresses your wait of 30/60/90 days for invoice payments. Get paid quickly and count on reliable cash flow.

2. 31% had difficulty with credit availability

HOW FACTORING HELPS: Businesses are often approved for a factoring agreement based on the creditworthiness of their customers, not their own credit history.

3. 27% had trouble making payments on debt

HOW FACTORING HELPS: Factoring accelerates your cash flow, enhancing your ability to make timely debt service payments.

4. 17% had difficulty purchasing inventory or supplies to fulfill contracts

HOW FACTORING HELPS: With the additional cash flow provided by a factoring program, you have increased purchasing power. This enables you to purchase inventory in a timely manner and to potentially take advantage of trade discounts.

|

How Businesses Handle Financial Challenges

|

|

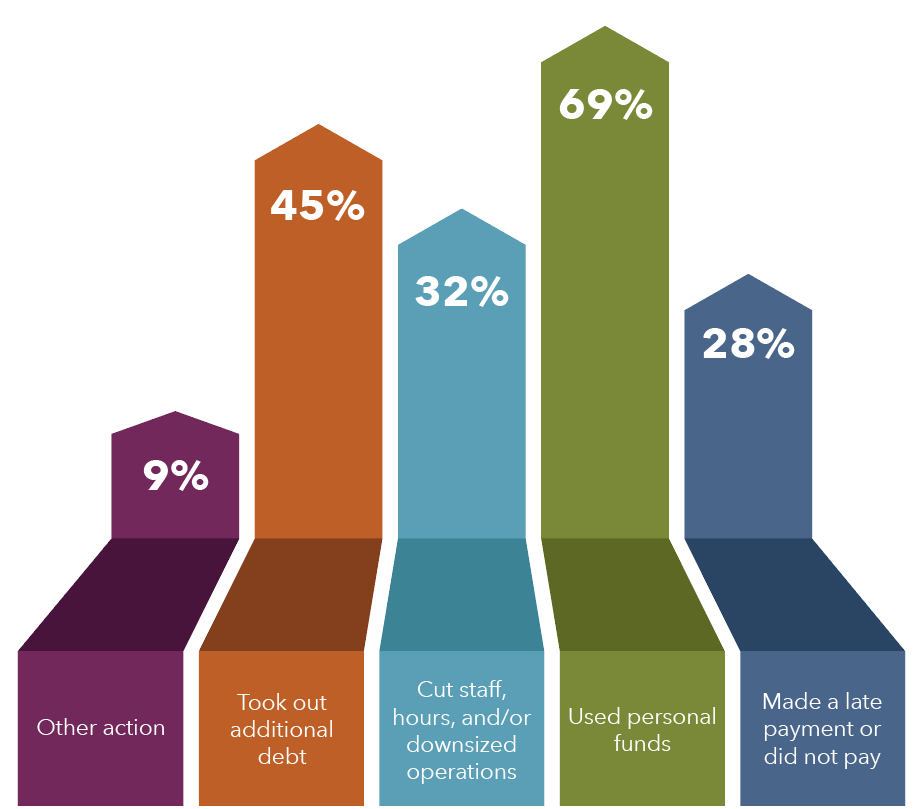

| Of 64% of small businesses who told the Federal Reserve they experienced financial challenges, 69% used personal funds to bridge the gap. |

The Fed’s survey also shows how businesses tried to overcome these financial difficulties. A huge portion – 69% - used personal funds. Another 45% took out additional debt, and 32% cut staff, hours and/or downsized operations. Twenty-eight percent made a late payment or didn’t pay some type of debt or bill.

When it comes to preparing for an economic slowdown, which option sounds better: struggling with cash flow problems on a daily basis or working with a reputable firm to turn around your customer invoices quickly and increase your operating cash flow? First Business Bank's Accounts Receivable Financing team prioritizes integrity and customer service. Our professionals are experienced in a broad range of industries and can improve your cash flow quickly.