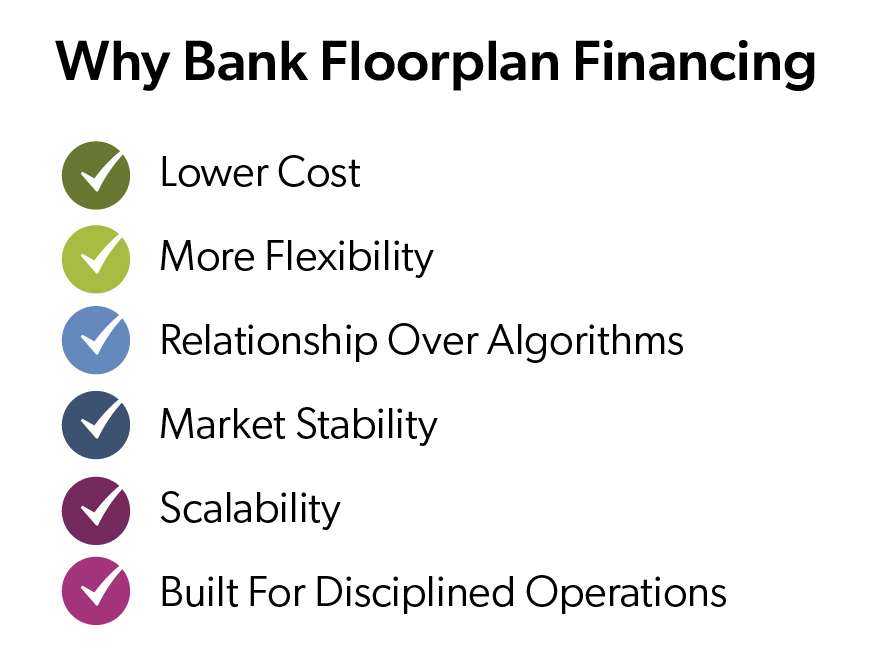

Many successful independent car dealers outgrow their floorplan provider — it starts showing when the line of credit isn’t keeping pace, decisions take longer, and rep turnover starts increasing. Bank floorplan financing is built for dealers who have reached that point and are ready for a bank floorplan that costs less, offers more flexibility, and grows with the business.

This guide is for established, profitable dealers evaluating whether their current floorplan provider is working in their favor.

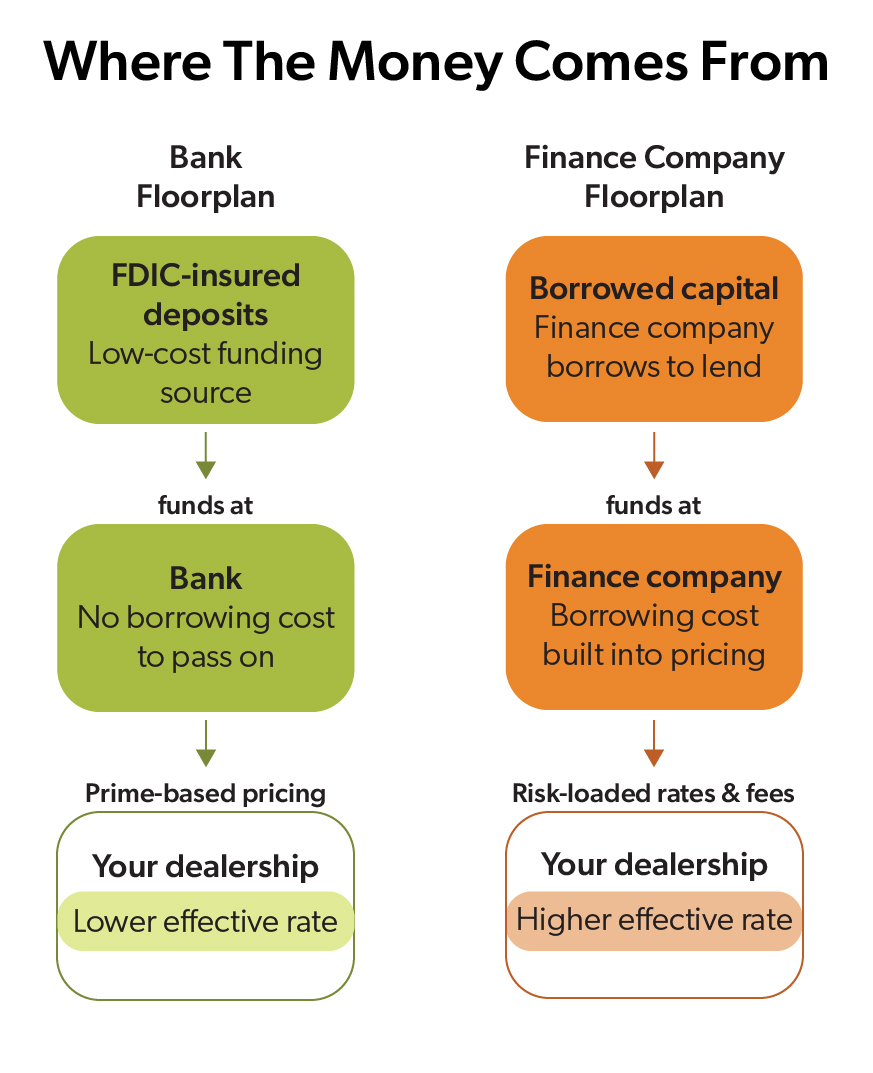

How Bank Floorplan Financing Works Differently

The structural difference between banks and finance companies matters more than most dealers realize.

Finance companies borrow the money they loan to dealers. That cost to borrow is built into their pricing, layered with fees, and passed directly to your bottom line. Alternatively, banks fund floorplan lines from their FDIC-insured deposits, which carry a significantly lower cost of funds. That advantage flows through to dealers as competitive pricing and fewer fees attached to the bank floorplan.

Finance companies borrow the money they loan to dealers. That cost to borrow is built into their pricing, layered with fees, and passed directly to your bottom line. Alternatively, banks fund floorplan lines from their FDIC-insured deposits, which carry a significantly lower cost of funds. That advantage flows through to dealers as competitive pricing and fewer fees attached to the bank floorplan.

There's also a portfolio difference, as finance companies usually serve thousands of clients across every dealer type. Banks that specialize in independent dealer floorplanning work with a smaller, more selective portfolio, so they get to know your business and give you faster decisions, building a valuable relationship over time, which is the core advantage of bank floorplan financing for independent dealers.

The Real Cost Difference Between Bank Floorplans and Finance Companies

Banks typically offer the lowest effective rates in the floorplan market. Here's how the math works in your favor:

Prime-based pricing: Banks fund at Prime-based rates, not risk-loaded interest rates with multiple fees

Prime-based pricing: Banks fund at Prime-based rates, not risk-loaded interest rates with multiple fees - Monthly compounding: Interest compounds monthly, not daily, which adds up significantly over time

- No title-absent interest: No interest charged on units until the auction holds the title

- No curtailment fees: Normal inventory turns don't trigger additional fees

- No non-auction purchase fees: Freedom to source inventory without penalty

- Delayed curtailment structures: Cash is preserved during standard inventory turns

The net effect is that more stays on your dealership’s bottom line.

How Does A Bank Floorplan Offer Inventory Flexibility?

Dealers often assume that banks are more restrictive about what they'll floor. With the right bank partner, that's not the case. A specialized bank floorplan gives dealers the freedom to source inventory the way their business operates, including:

- Auction-sourced and non-auction-sourced inventory

- Canadian auction purchases

- Trade-ins with lien payoffs

- No blanket mileage or age restrictions on floored inventory

That flexibility matters because buying strategies change. Market conditions shift, auction availability fluctuates, and the best unit on a given day doesn't always come from the expected source. A floorplan that flexes with how you actually buy is a competitive advantage.

When evaluating any floorplan partner, ask specifically about sourcing restrictions, mileage and age limits, and how trade-ins with existing liens are handled. The answers will tell you a lot about whether they understand how independent dealers operate.

When The Used Car Market Shifts, Your Lender's Commitment Matters

The floorplan relationship is easy to overlook when lending is good. It becomes critical when conditions change.

In recent years, several major lenders exited the floorplan market entirely, in some cases giving dealers as little as 90 days to find alternative financing. For dealers caught in those situations, the disruption was a crisis that forced rushed decisions under pressure.

A committed bank partner operates differently. Banks underwrite the dealer relationship, not just the inventory data. That involves:

- Human credit decisions rather than algorithmic approvals

- The ability to explain one-off events like tax timing, recon delays, or expansion expenses

- Flexible limit restructuring when the market shifts, whether temporary or permanent

- Regulatory stability with consistent terms that don't change overnight

- No haircut risk during market stress, a real exposure with some non-bank providers

That human relationship also shows up in day-to-day operations. Inventory audits are a reality with any floorplan provider, but the experience varies significantly. A bank with a smaller, more focused dealer portfolio typically delivers a more efficient audit process, with less disruption to daily operations than dealers report with finance companies.

During market downturns, periods of rapid growth, and temporary liquidity crunches, a bank floorplan financing partner that knows your business is worth more than one that only knows your collateral.

How A Bank Floorplan Grows With Your Dealership

For dealers focused on long-term growth, a bank floorplan financing relationship is a starting point, not a ceiling. A bank partner can scale with the dealership in ways a finance company often can’t.

Bank floorplans flex with:

Bank floorplans flex with:

- Higher limits with faster decisions and less red tape as the relationship matures

- Support for additional locations without starting the credit process from scratch

- Flexible structures that adapt as inventory volume and mix evolve

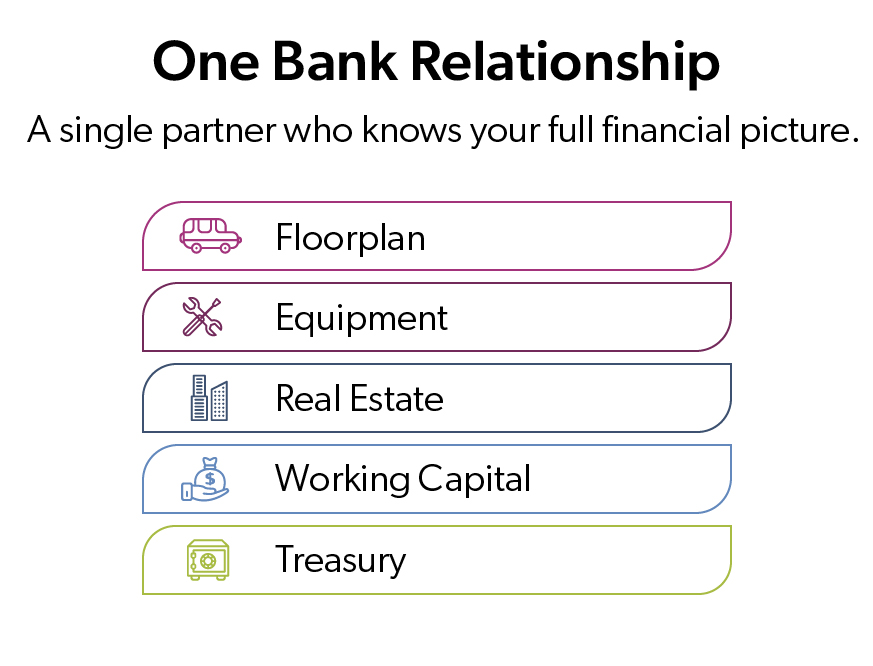

Beyond the floorplan, banks offer:

- Real estate and facility loans

- Working capital lines

- Equipment and service department financing

- Treasury and operating accounts

That last point is worth unpacking. One banking relationship can replace three or four disconnected lenders, simplifying operations, and giving the dealership a single point of contact who understands the full financial picture. Over time, that institutional knowledge compounds. The bank comes to understand seasonal patterns, growth plans, and the specific dynamics of the dealership, making every subsequent decision faster and more informed.

For dealers who have outgrown their current provider, that kind of integrated relationship is often what was missing all along.

Is Your Dealership A Good Candidate For Bank Floorplanning?

Bank floorplan financing isn't the right fit for every dealer, and that selectivity works in qualified dealers' favor. Banks that specialize in independent dealer floorplanning are looking for a specific profile, and dealers who meet it are rewarded with better pricing, faster approvals over time, and access to lending products that go well beyond the bank floorplan line.

Strong dealer candidates typically share these characteristics:

- Turns inventory in 75 days or fewer

- Consistently profitable with clean, current financials

- Sources inventory from documented, traceable channels

- Operates with lower leverage and disciplined reporting

- Looking for a stable, reputable long-term bank floorplan partner

For dealers who fit this profile, the benefits compound over time. Trust builds, decisions get faster, and the bank becomes a genuine strategic asset rather than a transactional vendor.

One thing worth noting: many dealers who would qualify for bank floorplan financing assume they won't. If your dealership has outgrown its current provider but you haven't explored the bank option, it's worth a conversation.