As 2025 draws to a close, individuals and families considering year-end charitable and personal gifts face a significantly altered tax landscape. The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, introduced significant changes that impact how gifts to individuals and charities are treated for tax purposes. With thoughtful planning, donors can still maximize both their philanthropic impact and tax efficiency.

Key Tax Law Changes Affecting Year-End Charitable Giving

Several provisions of OBBBA take effect in 2026, but 2025 offers a unique window of opportunity. Here’s what you need to know:

1. Expansion of the SALT Deduction

- The State and Local Tax (SALT) deduction cap has been increased from $10,000 to $40,000 for 2025.

- This change may encourage more taxpayers to itemize deductions, making charitable contributions more tax-efficient this year.

- However, the benefit phases out for those with Modified Adjusted Gross Income (MAGI) over $500,000, reverting to the $10,000 SALT deduction cap at $600,000 MAGI.

2. New AGI Floor And Deduction Cap Effective In 2026

- Starting in 2026, itemizers can only deduct charitable gifts above 0.5% of Adjusted Gross Income (AGI).

- The maximum deduction benefit will be capped at 35%, even for those in the 37% tax bracket.

- These changes do not apply in 2025, making this year a strategic time to accelerate planned giving and get the full tax benefit of your charitable gifts.

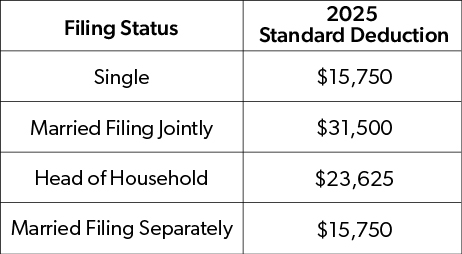

3. Standard Deduction for 2025 Permanently Increased

The standard deduction for 2025 has been permanently increased and is indexed for inflation going forward. An additional $6,000 per person (or $12,000 per couple) deduction for seniors age 65+ is available from 2025 through 2027. This benefit phases out at $75,000 MAGI for single filers and $150,000 MAGI for joint filers.

Here are the updated standard deduction amounts:

Strategies for Effective Year-End Charitable Giving in 2025

1. Accelerate Charitable Contributions

If you’re considering a large gift in the next few years, 2025 is the year to act. By giving now, you can:

- Avoid the 0.5% AGI floor and 35% deduction cap.

- Maximize the value of your deduction at your full marginal rate (up to 37%).

2. Structure Donor-Advised Funds (DAFs)

- DAFs allow you to “bunch” multiple years of giving into 2025, take the deduction now, and distribute funds to charities over time.

- This is especially useful if you itemize your charitable deductions and add them to the State and Local Tax (SALT) deductions (capped at $40,000) to exceed the standard deduction this year.

3. Maximize Cash Donations

- Under OBBBA, cash contributions to qualified public charities can now permanently be deducted up to 60% of a donor’s adjusted gross income (AGI).

- OBBBA also clarified that this 60% limit can be “stacked” on top of deductions for non-cash gifts, as long as the combined total does not exceed 60% of AGI.

4. Gift Appreciated Assets to Charity

- Donating appreciated stock or real estate avoids capital gains tax and provides a deduction for the full fair market value. This is particularly attractive in 2025, given the strong market performance and growth in many investment portfolios.

- Your deduction is limited to 30% of your AGI each year, but you can carry over any excess deductions for up to five additional years.

5. Consider Qualified Charitable Distributions (QCDs)

For those over age 70½, QCDs from IRAs remain a powerful tool.

QCDs allow you to donate up to $108,000 with a direct transfer of IRA funds to charity, satisfying required minimum distributions (RMDs) without increasing taxable income. The charitable distribution from your IRA is not included in your AGI and thus allows a tax break even if you can’t itemize and are taking the standard deduction.

Reminder: QCDs may NOT be made from company retirement plan accounts, and QCDs to private foundations or DAFs are not permitted.

Best Practice: Work with your IRA custodian to initiate the QCD well before year-end so the charity can cash the check in a timely manner. QCDs must be completed by December 31, 2025.

In cases in which IRA owners make QCDs using “checkbook IRAs,” the checks must actually be cashed by the charity by year-end, or they won’t be included as a qualified distribution for RMD or 2025 tax reporting purposes.

Important Year-End Giving Deadlines

Planning your year-end giving strategy requires careful attention to timing to ensure gifts are completed before December 31 so they qualify for 2025 tax benefits.

Different types of gifts require different processing times, and missing these deadlines could push your intended 2025 gifts into 2026, when the new tax restrictions take effect. Here's what you need to know:

- December 1: Mutual Fund Transfers. Begin transfers of mutual fund shares to charities or family members to allow sufficient processing time

- December 9: Stock Gifts. Complete stock transfers to ensure they settle before year-end, whether for charitable or personal gifts.

- December 31: Cash Gifts and Checks. Final deadline for cash donations, donor-advised fund contributions, and mailed checks (must be postmarked by 12/31).

Planning tip: For large or complex gifts, start the process earlier. Work with your financial advisor or our Private Wealth team to ensure proper documentation and timing, especially for appreciated assets that may require additional paperwork.

Year-End Giving to Individuals: Estate and Gift Tax Considerations

Whether helping children with a downpayment for a home purchase, supporting a grandchild's education, or covering a friend’s medical expenses, there are several tax-efficient ways to give meaningfully to the ones you care most about at year-end.

- Annual Gift Tax Exclusion. The annual gift tax exclusion is $19,000 per recipient in 2025. Married couples can double the gift through “gift-splitting” for a total of $38,000 per recipient. Consider using year-end gifts to children and grandchildren to reduce your taxable estate while taking advantage of the current exclusion limits.

Gifts of appreciated assets to individuals are transferred with a carryover basis. The gift recipient will realize and pay any applicable capital gains tax upon sale of the assets. Depending on the tax bracket of the recipient, annual exclusion gifts of cash may be the best option. - Lifetime Estate And Gift Tax Exemption. The lifetime estate and gift tax exemption is currently $13,990,000 per individual in 2025 and is set to increase to $15 million per individual ($30 million per married couple) in 2026 under OBBBA.

- Tuition and Medical Expenses. Payments made directly to educational institutions or medical providers on behalf of someone else are not subject to gift tax and do not count against your annual exclusion.

- 529 Plan Contributions. Contributions to a 529 college savings plan can be front-loaded with up to five years’ worth of annual exclusion gifts, allowing you to contribute up to $95,000 ($19,000 x 5 years) per beneficiary in 2025 without gift tax consequences. Contributions are often deductible from state income tax as well.

Final Thoughts On Year-End Giving In 2025

The OBBBA has introduced both opportunities and complexities in charitable and personal giving. For many, 2025 represents a “last best chance” to make impactful gifts under more favorable tax conditions. Whether you’re supporting a favorite nonprofit, funding a donor-advised fund, or making gifts to family, now is the time to act.

Date: 12/1/2025

The tax information provided herein is general and educational in nature and should not be construed as legal or tax advice. First Business Bank does not provide legal or tax advice. Content provided relates to taxation at the federal level only. Rules and regulations regarding tax deductions for charitable giving vary at the state level and laws of a specific state or laws relevant to a particular situation may affect the applicability, accuracy, or completeness of the information provided. As a result, First Business Bank cannot guarantee that such information is accurate, complete, or timely. Tax laws and regulations are complex and subject to change, and changes in them may have a material impact on pre- and/or after-tax results. First Business Bank makes no warranties with regard to such information or results obtained by its use. First Business Bank disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Always consult an attorney or tax professional regarding your specific legal or tax situation.