Most parents work their whole lives to earn as much as they can with the hope of making life easier for their kids or their grandkids. But what if everything you worked to pass on disappears within a generation or two?

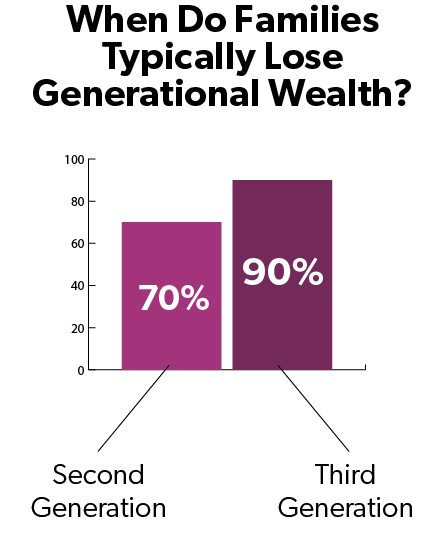

According to Fortune, 70% of wealthy families lose their wealth by the second generation and nearly all (90%) lose it by the third. A UBS survey also shows that while 83% of investors express concern about transferring wealth, less than half (40%) of them have spoken with their heirs about it.

According to Fortune, 70% of wealthy families lose their wealth by the second generation and nearly all (90%) lose it by the third. A UBS survey also shows that while 83% of investors express concern about transferring wealth, less than half (40%) of them have spoken with their heirs about it.

If you’d like your legacy to last, families should teach basic principles of financial literacy early to their kids, infusing it into their everyday lives so it’s a natural part of life as they mature.

Talk To Kids About Fiscal Responsibility

One of the first steps to help kids understand money is talking about it. Families are often uncomfortable discussing managing wealth , regardless of how much of it they have. That can be counterproductive, especially as kids mature into adults. Without a foundational understanding of where wealth comes from and how it works, they will approach their own quest for affluence on shaky footing.

In 2025, only 27 American states required high schools to teach financial literacy. Since many kids are not learning these fundamentals in school, it is essential that parents teach their children fiscal responsibility and the financial skills that they will need to make sound and wise financial decisions. They will thank you for it later in life! These issues can spill into other areas in their later years, too, when the need for financial planning, budgeting, and saving becomes more urgent — during estate planning, for example. The last thing you want is for your kids to fight over inherited assets they didn’t even know existed — let alone how those assets are structured.

It’s essential to talk about money with your kids so they can learn the same habits that allowed wealth to accrue in the first place, as well as what to do with it once they have it. At the end of the day, money is a matter of fact, and that calls for frank conversations.

Teach Financial Literacy To Kids

Start with the basics. Review some statements of your monthly bills and show them how to make payments both online and via a written check.

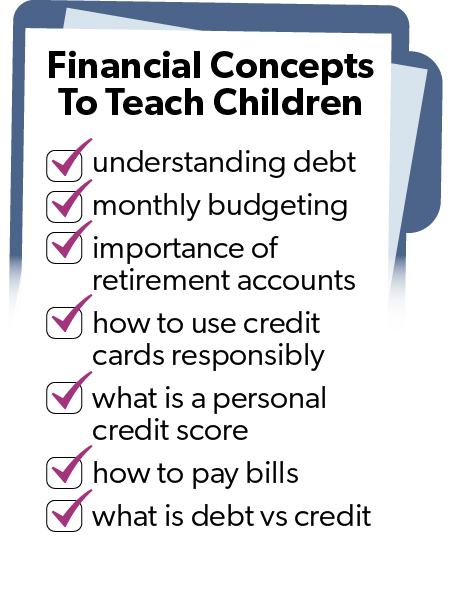

The benefits of financial literacy is that individuals who are financially literate are much more confident in making responsible financial decisions. Basic financial concepts include the following:

The benefits of financial literacy is that individuals who are financially literate are much more confident in making responsible financial decisions. Basic financial concepts include the following:

Basic financial concepts include the following:

- Understanding debt

- Monthly budgeting and saving

- Retirement accounts

- Credit cards/Personal credit scores

- How to pay a bill

- Debts vs Credits

When actions become behaviors and behaviors become characteristics, your kids will be well positioned to protect the family wealth — and potentially contribute to its growth.

Finding ways to help kids understand how money applies to their lives is another impactful way to teach by example. Kids don’t often make hands-on decisions about money, so your family’s wealth may be an abstract concept that’s difficult to understand.

As the old saying goes, “Money does not grow on trees.” Explain to them why they should turn off the lights or take a five-minute shower instead of a 20-minute one. These are examples of practical, money-saving techniques. These requests are often “in-one-ear-and-out-the-other" for many kids, so incentivizing their participation can help. For instance, telling them if next month’s utility bill drops, you will pay them the difference between the two utility bills. Suddenly, they become more aware of how they can help and might even call you out to leave the lights or TV on!

It’s tempting to assume our kids have no interest in financial literacy , even if they knew what we were talking about. However, they often know more than we give them credit for. Try to involve them in the process in a way that will resonate.

This is an excellent way to give kids experience with thinking critically about personal finance, while also bringing some of those complex topics down to earth.

Encourage Your Children To Earn & Save Their Own Money

Many families are comfortable allowing their wealth to carry their kids into adulthood, and there are plenty of reasons for doing so. For example, allowing them to focus on their studies during college without having to work can translate into better academic performance. However, managing a job while managing their studies can also teach them time management skills.

Unless your child has an innate desire to work, it may take them a while to fully grasp the need to earn their own keep. Installing a work/reward mentality will benefit them throughout their lives. Assign them chores in exchange for allowance or motivate them by using academic performance for larger purchases. This helps to set their expectations that wealth isn’t just a part of the air they breathe and follows them wherever they go.

The French economist Thomas Picketty points out that income from wages rewards work done in the present, while income from inheritance rewards work done in the past. Because of this, it’s important to instill a strong work ethic in kids so they are less inclined to take their wealth for granted. Financial stewardship is an essential discipline among families who want to keep their wealth intact.

Frequently Asked Questions About Teaching Children Financial Literacy

How can I talk to my children about managing wealth without spoiling them?

Open and honest conversations with your children about money and managing wealth are critical. Be clear about the family's financial situation and set clear expectations and boundaries. Teach your children to appreciate hard work and the importance of budgeting and saving. Encourage them to establish good money habits and to set financial goals early, including saving and donating to charity, and work towards achieving them.

At what age should I start talking to my children about money and wealth?

It's never too early to start talking to your children about money and managing wealth. As soon as they begin asking questions about money or talk about buying items, you can introduce financial concepts and good money habits, sticking with age-appropriate, basic discussions they can understand. Consider emphasizing saving to purchase specific items, talk about waiting for a sale or finding a discount, and discuss how you do the same in your life.

How can I instill good money habits in my children?

Lead by example by demonstrating good money habits yourself. Encourage your children to save a portion of any money they earn or receive as gifts. Teach them the importance of budgeting and living within their means. Involve your children in financial decision-making and show them how to prioritize spending.

What are some common mistakes parents make when talking to their children about wealth?

Some common mistakes include giving children everything they want, not setting clear expectations or boundaries around money, and not being open and honest about the family's financial situation. It's important to have a balanced approach to teach your children to be responsible with money and make good financial decisions.

How can I help my children understand the importance of saving and investing?

Encourage your children to set financial goals and work towards achieving them. Teach them about the power of compound interest and how saving and investing can help their money grow over time. Show them the potential long-term benefits of investing in stocks or mutual funds.

A recent survey found that 48% of high schoolers learn about investing from social media. This could lead to disastrous consequences. Teach them the fundamentals of investing, including the potential risks and rewards.

What are some age-appropriate ways to introduce financial concepts to my children?

Money can be an interesting and fun topic if it is presented in a way that can get them excited. There are many fun games that can teach children about money management, like Monopoly, The Game of Life, or Payday. Kids can learn about budgeting, saving, and investing while playing them. Try to create learning opportunities whenever possible. Many spouses avoid discussing money with one another and unfortunately their children will learn this same negative behavior. An open and honest dialogue will do wonders for your child as they get older.

Encourage your children to earn their own money through chores or other tasks. This can help them understand the value of hard work and develop a sense of responsibility. Discuss needs versus wants to help them develop money-saving techniques and budget for items they’d like to purchase.

When they turn 18, have your child open their first credit card account. This will teach them how to borrow and pay back money and give them exposure to interest charges if the balance is not paid every month.

Should I disclose my own personal finances to my children?

It's up to your personal discretion but disclosing some basic information about your family's financial situation can help your children understand the value of money and the importance of responsible financial behavior. You don't need to share all the details, but being open and honest can help build trust and foster good money habits.

How can I ensure that my children don't develop a sense of entitlement around wealth?

Encourage your children to work hard and earn their own money. Teach them the value of money and the importance of fiscal responsibility. Treat everyone respectfully and teach your children that all work has value. Your child can learn the value of hard work as well as a trade by working in the summers doing construction, landscaping or even starting their own business. Set clear expectations and boundaries around money and avoid spoiling them by giving them everything they want.

How can I teach my children about philanthropy and giving back to the community?

Encourage your children to volunteer and get involved in community service projects. Talk to them about the importance of giving back and helping others in need. Set a good example by donating to charity or volunteering your time. Involve your children in the decision-making process by allowing them to choose a cause they are passionate about supporting. Teach them the importance of having compassion for others and assisting those in need.