As our population ages, protecting seniors from financial elder abuse has become increasingly critical. One in six people in the United States are now over age 65, and financial elder abuse has reached alarming levels, with the Better Business Bureau reporting that older adults lose more than $36 billion to financial fraud annually. This crisis affects millions of seniors and their families across the nation, often occurring behind closed doors because of the emotions and shame involved.

"Scams are definitely more sophisticated, tech-driven, and bolder now," said Kevin Pomarnke, Senior Vice President - Trust Advisor at First Business Bank. He notes a shift from in-person schemes to online tactics: "Ten years ago, an 80-year-old person might not have been using a computer. Now, unfortunately, they're much more susceptible to financial elder abuse perpetrated online or through other electronic means such as text messages or calls."

By understanding the warning signs, applying preventive strategies, and knowing how to respond when you suspect financial elder abuse, we can create a strong defense to help protect our loved ones. Awareness and proactive measures are key to safeguarding our elders' financial well-being and preserving the legacy they've worked so hard to build.

What Is Financial Elder Abuse?

Financial elder abuse encompasses a wide range of exploitative actions that target older adults' finances. This form of abuse occurs when someone illegally or improperly uses an elderly person's money, assets, or property for their own benefit. The perpetrators can be strangers, but often they are people the victim knows and trusts, including family members, caregivers, or financial advisors.

Sadly, adult children are the most frequent perpetrators of theft from their relatives. Nearly 40% of cases reported through the Bank Secrecy Act to the Financial Crimes Enforcement Network (FinCEN) are of adult children exploiting their relatives’ finances.

Financial elder abuse takes many forms:

- Theft: Directly stealing money or valuables from an elderly person.

- Fraud: Using deception to gain access to an elder's finances, such as through scam phone calls or emails.

- Misuse of authority: Abusing power of attorney or guardianship to misappropriate funds.

- Coercion: Pressuring an elder to change their will or sign over assets.

- Exploitation: Using an elder's resources for personal gain without their full understanding or consent.

Financial elder abuse often causes devastating harm. Sometimes victims lose their life savings, leaving them unable to afford necessities or healthcare. The emotional impact can be equally damaging, leading to depression, anxiety, and a loss of independence. Families also face unexpected financial burdens, heartbreak of seeing their loved ones exploited, and sometimes even loss of trust. When a family member is the abuser, it can create lasting conflicts.

“The simple theft isn't as common anymore,” Pomarnke said. “You can't just steal someone's mail and get their Social Security number. As our protective measures evolve, so do the scams and as technology advances, scams become more complicated and more difficult to uncover.”

How Do You Identify Financial Elder Abuse?

While some signs of financial elder abuse may be subtle, others can be obvious. Vigilance and regularly communicating with elderly loved ones are key to finding potential problems.

"I can't tell you all the times over the years I've seen someone creep into the picture later in life,” Pomarnke said. “Often, it’s a caregiver or non-family member, and checks suddenly are written out to this person with no valid explanation as to the reason(s). You really have to be on the lookout for situations like that."

Here are some warning signs of financial elder abuse:

- Unexplained financial transactions: Sudden, large cash withdrawals or transfers to family members or outsiders that seem out of character.

- Changes in financial documents: Sudden changes in wills, trusts, or power of attorney documents.

- Unusual credit card activity: Unexpected charges, especially for items or services that don't make sense for the elder's lifestyle or needs.

- Unpaid bills: Despite having adequate resources, a senior suddenly unable to pay bills may point to financial abuse.

- Unauthorized account access: Unexpected additions to a signature card or signs of forged signatures on financial documents.

- Missing valuables: Disappearing jewelry, art, or other valuable possessions.

- Funds disappear: Unexplained depletion of savings or investment accounts.

- New "friends" show interest in finances: Be particularly cautious of new acquaintances who seem interested in the senior’s finances.

- Sudden isolation: Abusers often try to limit an elder's contact with others who might detect the financial elder abuse.

- Changes in financial behavior: If an elder who was previously financially savvy suddenly seems confused about their finances, it could indicate manipulation or cognitive decline being exploited.

If you notice any of these red flags, it's crucial to investigate further and take appropriate action to protect the elder's financial well-being.

What Are Common Financial Scams Targeting Seniors?

Understanding the most common scams can help seniors and their families stay ahead of the game to prevent financial loss. In financial elder abuse cases, data from FinCEN shows that checks and wires are the most frequently used methods for transmitting scam funds.

"When elders receive unsolicited phone calls, emails, or text messages, there's usually a sense of urgency," Pomarnke said. "From an outsider looking in, these offers often seem too good to be true. For instance, they might promise $10,000 back in a year for a $5,000 investment, which is simply unrealistic. They're going to try to get you right there and then – if you don't act now, this won't be good tomorrow." He points out that seniors who are often alone can be particularly vulnerable to these tactics.

Here are some of the most prevalent financial scams targeting elders:

- Telemarketing Scams: Using high-pressure sales tactics, these scams manipulate seniors into making quick decisions. Scammers might offer "limited time" investments, miracle health products, or unnecessary services. They create a sense of urgency, pushing them to act before they can talk with family or financial advisors.

- Grandparent Scams: In this common scheme, scammers impersonate a grandchild in an emergency situation. The “grandchild” claims to be in jail, in an accident, stranded in a foreign country, in a medical emergency, or another time-sensitive situation. They beg for money to be wired immediately, playing on grandparents’ emotions and desire to help.

- Romance Scams: Exploiting loneliness, these scammers build fake romantic relationships, often through online dating sites or social media. After gaining trust, they invent emergencies or business opportunities, asking for financial support. These scams can drain savings over time as the victim believes they're helping a loved one.

- IRS or Government Impersonation Scams: Scammers pose as IRS agents or other government officials, claiming the senior owes back taxes or fines. They threaten legal action, arrest, or deportation unless immediate payment is made. The pressure and fear tactics often cause seniors to comply without verifying the claim.

- Lottery and Sweepstakes Scams: These scams inform seniors they've won a large prize but must pay fees or taxes upfront to claim it. Scammers might use official-looking documents or websites to appear legitimate, tricking seniors into paying for a nonexistent windfall.

Each of these scams manipulates seniors by exploiting common vulnerabilities. They may play on emotions, create fear, or offer false hope. Scammers often pressure seniors to keep the interaction secret from family members, isolating them from potential help.

By educating seniors about these common scams and encouraging open communication about financial matters, families can create a strong defense against financial elder abuse. Legitimate organizations won't use high-pressure tactics or demand immediate, secretive action.

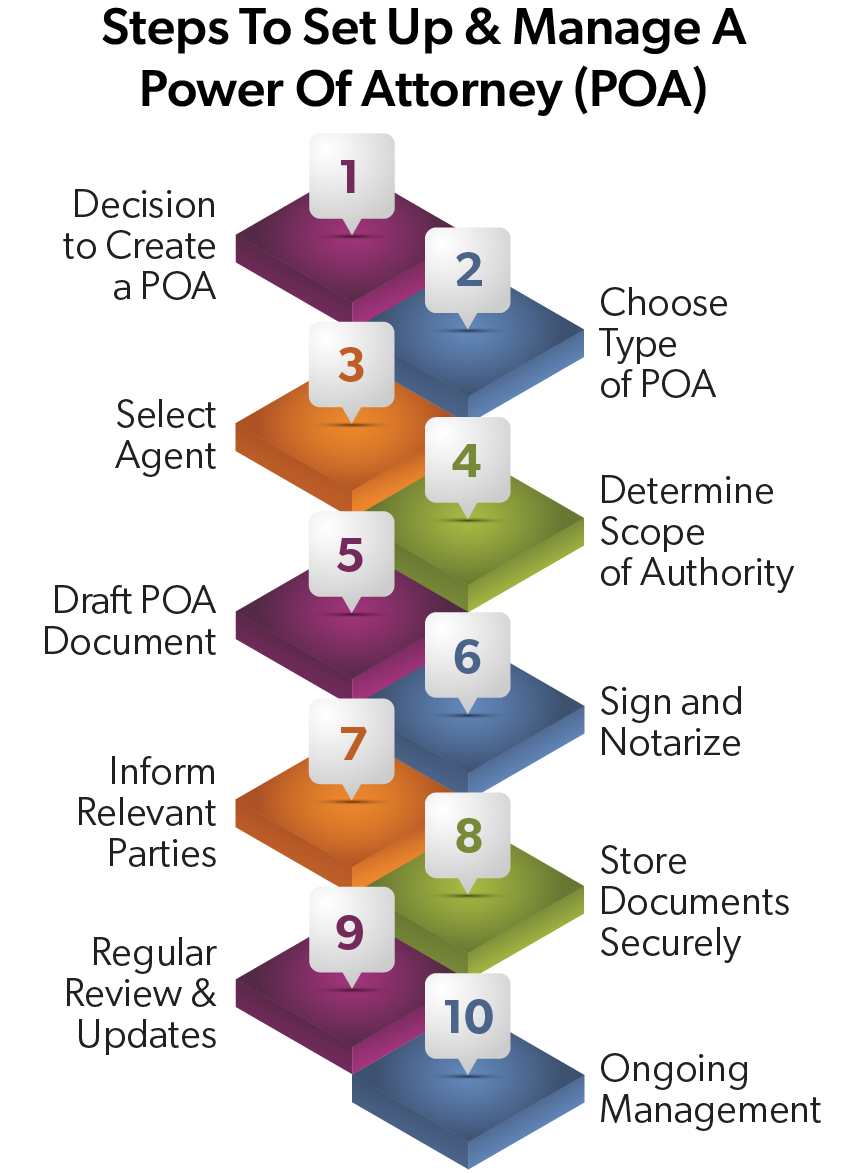

How Can You Use Power Of Attorney to Prevent Financial Elder Abuse?

When used correctly, a Power of Attorney (POA) can be a powerful tool in preventing financial elder abuse. There are two main types of POA: financial and healthcare. To prevent financial elder abuse, we'll focus on the financial POA.

A financial POA grants an individual (the agent) the authority to make financial decisions on behalf of another person (the principal). This can include managing bank accounts, paying bills, and making investment decisions. It's crucial to choose the right person and establish clear guidelines to ensure the elder's financial interests are protected.

A financial POA grants an individual (the agent) the authority to make financial decisions on behalf of another person (the principal). This can include managing bank accounts, paying bills, and making investment decisions. It's crucial to choose the right person and establish clear guidelines to ensure the elder's financial interests are protected.

Key points to consider:

- Choose wisely: The agent should be someone the elder trusts completely, often a family member or close friend with a track record of responsible financial management.

- Understand responsibilities: The agent has a fiduciary responsibility to act in the best interests of the principal, making decisions that align with the elder's wishes and financial well-being.

- Set limitations: You can customize a POA to grant specific powers or limit the agent's authority to certain transactions or accounts.

- Maintain transparency: Open, regular communication between the POA, the senior, and family members can prevent misunderstandings and detect any potential abuse.

- Multiple agents: Appointing co-agents can provide an extra layer of oversight and protection.

A well-structured POA can prevent opportunistic abuse by giving a trusted individual the legal authority to oversee and protect the elder's finances. It can also allow quick action if signs of financial exploitation by others are detected.

What Steps Can You Take To Prevent Financial Elder Abuse?

Preventing financial elder abuse requires a proactive approach, ongoing education, open communication, and getting to know your Wealth or Trust Advisor and other financial professionals, Pomarnke said.

"A big part of an advisor-customer relationship is conversation and getting to know people's patterns and behaviors,” he said. “If I have a client who's never mentioned travel suddenly calls and wants $50,000 for a cruise, I’ll ask further questions to make sure it's legitimate – or if they're being prompted by someone else. It's crucial for advisors to know their clients' typical activities, just as family members do. For added protection, consider locking down credit reports with the credit agencies. Older folks may not know how to check these regularly, so having a trusted person do that for them can be invaluable in preventing financial elder abuse."

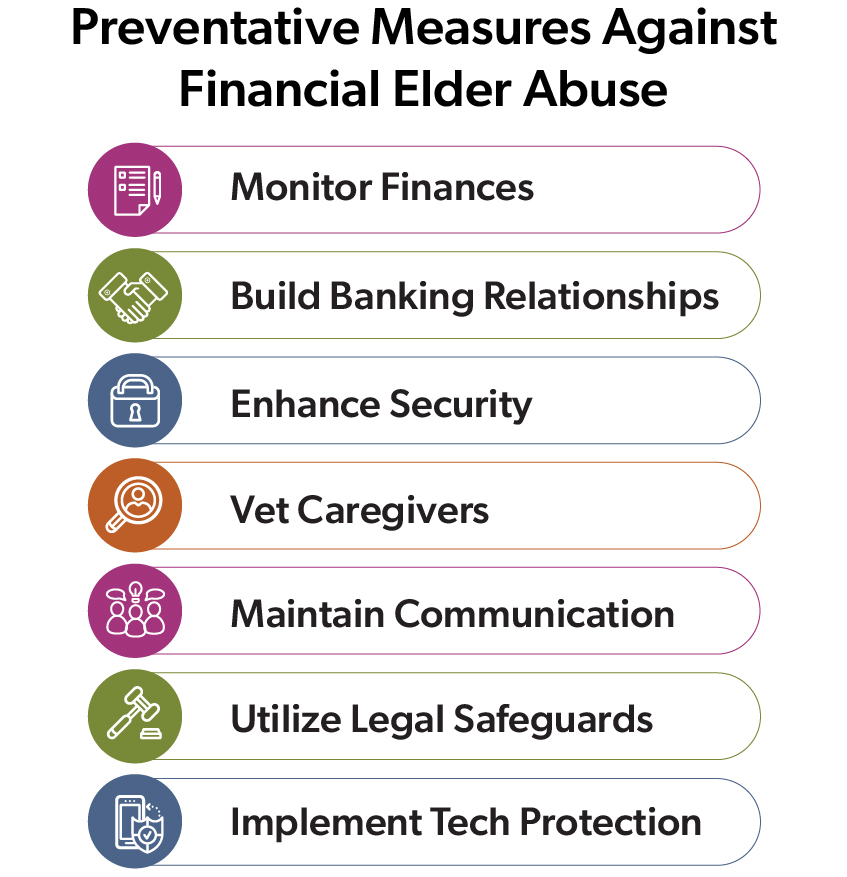

Here are key steps to protect seniors from financial exploitation:

Monitor finances closely: Regularly review financial statements and credit reports to spot unusual activity early.

Monitor finances closely: Regularly review financial statements and credit reports to spot unusual activity early.- Partner with financial institutions: Build a relationship with your advisor to create an additional layer of oversight for suspicious transactions.

- Enhance security measures: Secure sensitive financial documents and limit access to cash or valuables. Consider freezing their credit report and subscribing to identity theft protection services for added security.

- Discuss thoughtful decision-making: Encourage elders to avoid quick financial decisions, especially those involving time pressure or unsolicited offers.

- Vet caregivers and advisors: Thoroughly check references and credentials of hired caregivers or financial advisors who will have access to the elder's personal information or finances.

- Educate and communicate: Keep seniors informed about common financial scams and the importance of verifying requests for money or personal information. Maintain open communication about financial matters within the family.

- Utilize legal safeguards: Set up a durable POA or create a trust to provide additional oversight and protection.

By implementing these preventive measures, families can significantly reduce the risk of financial elder abuse and ensure their loved ones' financial well-being in their later years. Preventing financial elder abuse is an ongoing process requiring consistent attention and adaptation as circumstances change.

How Do You Report Financial Elder Abuse?

If you suspect financial elder abuse, act quickly to report it through the following:

- Report to law enforcement: File a report with your local police department or sheriff's office.

- Notify financial institutions: Alert the elder's bank or credit union about suspicious activity.

- Reach out to legal authorities: Contact your District Attorney's office or the State Attorney General. For online scams, file a complaint with the FBI’s Internet Crime Complaint Center (IC3).

- Use national resources: Call the Eldercare Locator at 1-800-677-1116 or the National Elder Fraud Hotline at 833–FRAUD–11 (833–372–8311) for guidance.

- Contact Adult Protective Services: Each state has an APS agency that investigates reports of elder abuse. Find your local APS office through the National Adult Protective Services Association website.

When reporting, provide as much evidence as possible:

- Gather relevant financial records

- Document any suspicious interactions or transactions

- Collect statements from witnesses

Reporting financial elder abuse is often legally required and can prevent further exploitation and help protect other potential victims.

Protecting Our Elders: A Shared Responsibility

Financial elder abuse is a growing threat, but vigilance, communication, and proactive measures can help prevent it. By understanding the signs, implementing preventive strategies, and knowing how to respond, we can create a strong defense against those who would exploit our seniors. Stay informed, seek professional advice when needed, and share this knowledge with the elders in your life. Resources like the National Center on Elder Abuse and the Consumer Financial Protection Bureau offer valuable information and support. Together, we can ensure our elders enjoy their golden years with the financial security and peace of mind they deserve.