Congress delivered on its promised deadline, revising tax and estate planning by passing the federal budget bill, One Big Beautiful Bill (OBBB), on July 4, 2025. Unlike prior tax laws with sunset provisions, these changes don’t expire automatically, but Congress could still revise them at some point in the future.

For high-net-worth individuals and business owners, this legislation shifts estate tax exemptions, personal tax structures, and business deductions. The changes create new planning opportunities while requiring careful review of existing strategies.

At First Business Bank, our expertise in wealth management and estate planning positions us to help you understand these modifications and adapt your financial strategies accordingly. Though not an exhaustive list, here are some key changes and what they might mean for your planning.

How Does The OBBB Change Estate Planning?

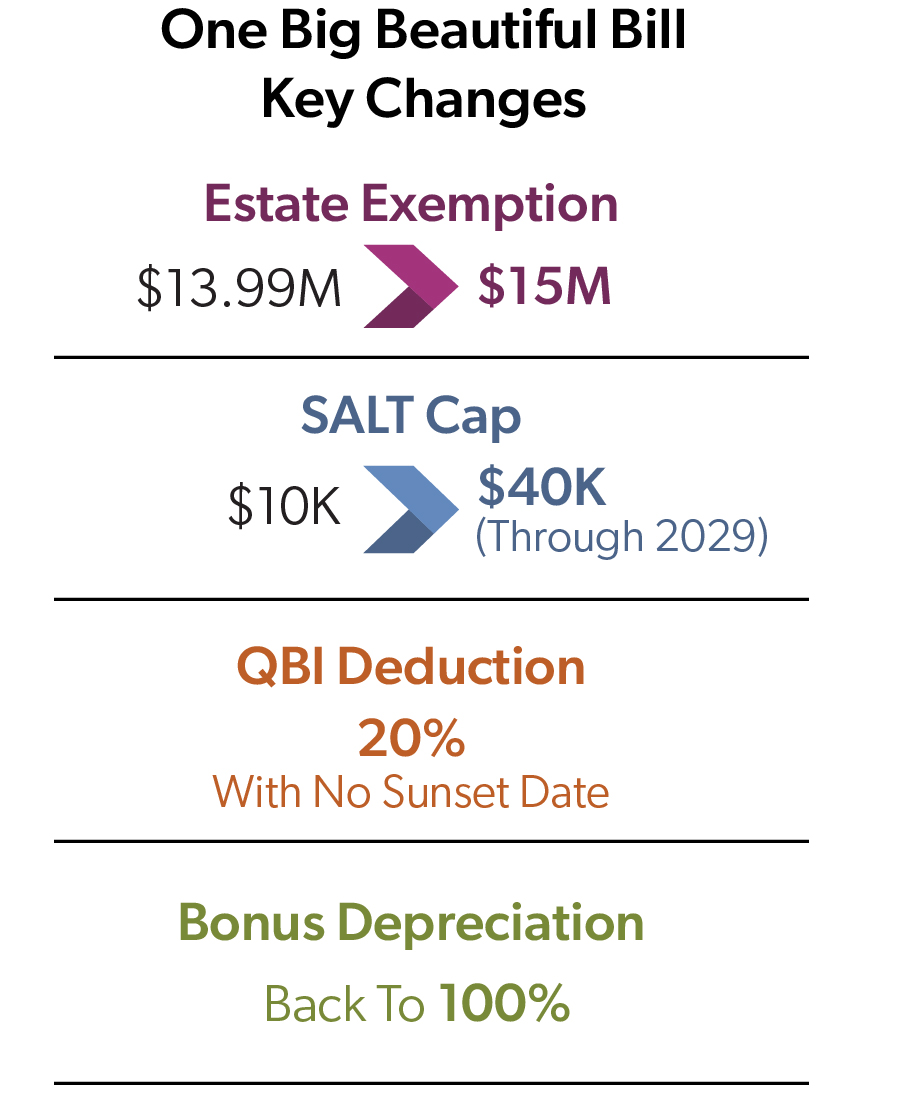

The federal budget bill increases the federal estate and gift tax exemption to $15 million per individual, starting January 1, 2026, up from $13.99 million in 2025. For married couples, this creates a combined exemption of $30 million when properly structured.

This change broadens access to advanced estate planning, giving wealthy families more flexibility to transfer assets tax-free.

This change broadens access to advanced estate planning, giving wealthy families more flexibility to transfer assets tax-free.

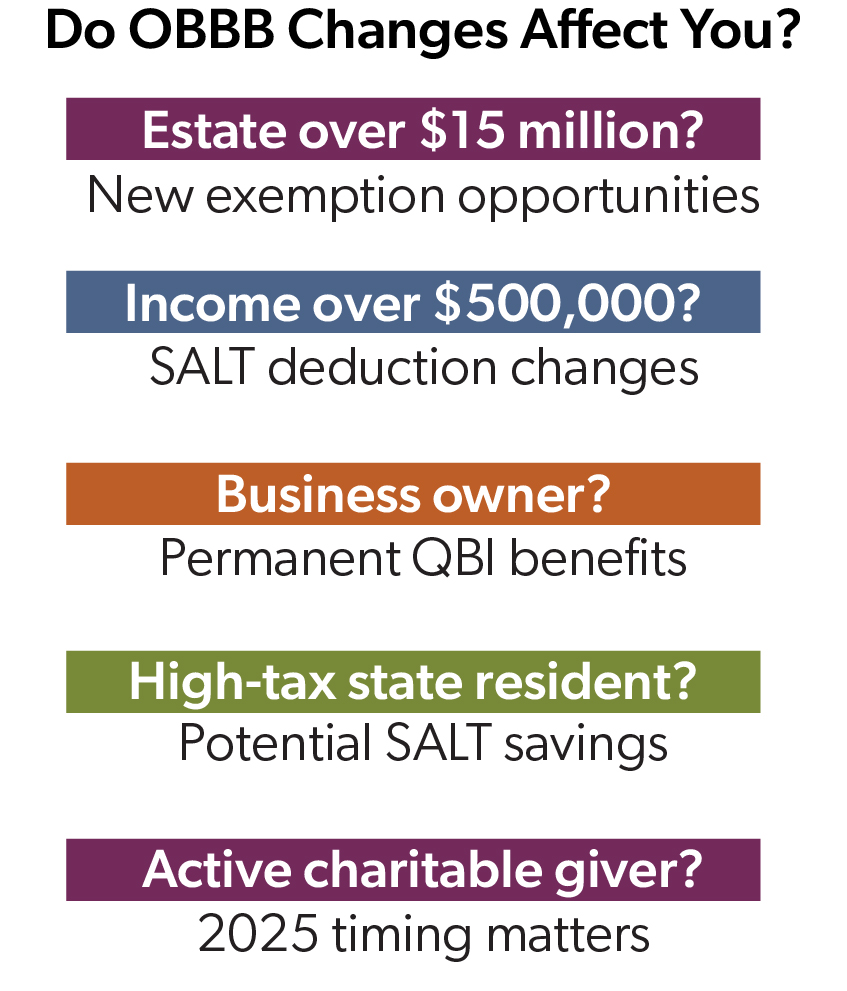

If your estate currently approaches or exceeds the 2025 threshold, you'll have additional capacity for wealth transfer strategies beginning in 2026. Existing irrevocable trusts and gifting programs may need reevaluation because you might have more options available.

The nature of these changes offers planning stability that wasn't available in prior legislation. However, "permanent" in tax law means until Congress decides otherwise. This might create an opportunity to implement strategies now while higher exemptions remain in effect.

How Does The OBBB Change Personal Taxes?

The federal budget bill delivers significant relief for many high-income taxpayers through increased deductions and modified tax structures. The most substantial change affects the state and local tax (SALT) deduction, which increases substantially for many taxpayers.

SALT Deduction Changes

SALT Deduction Changes

The SALT cap increases to $40,000 in 2025, rising to $40,400 in 2026, then increasing 1% annually through 2029, before reverting to $10,000 in 2030. However, this benefit phases out for higher earners. The higher SALT cap phases down for taxpayers with modified adjusted gross income over $500,000, reducing the deduction by 30% of the excess, but never below $10,000.

For married couples filing separately, both the SALT cap and phase-out threshold are halved to $20,000 and $250,000 respectively.

For Private Wealth clients in high-tax states, this change provides meaningful tax relief for the next several years, though income limitations may reduce benefits for ultra-high earners.

Standard and Itemized Deduction Updates

The standard deduction increases to $15,750 for single filers and $31,500 for joint filers, with annual inflation adjustments after 2025. For those who itemize, the legislation introduces new limitations on charitable deductions.

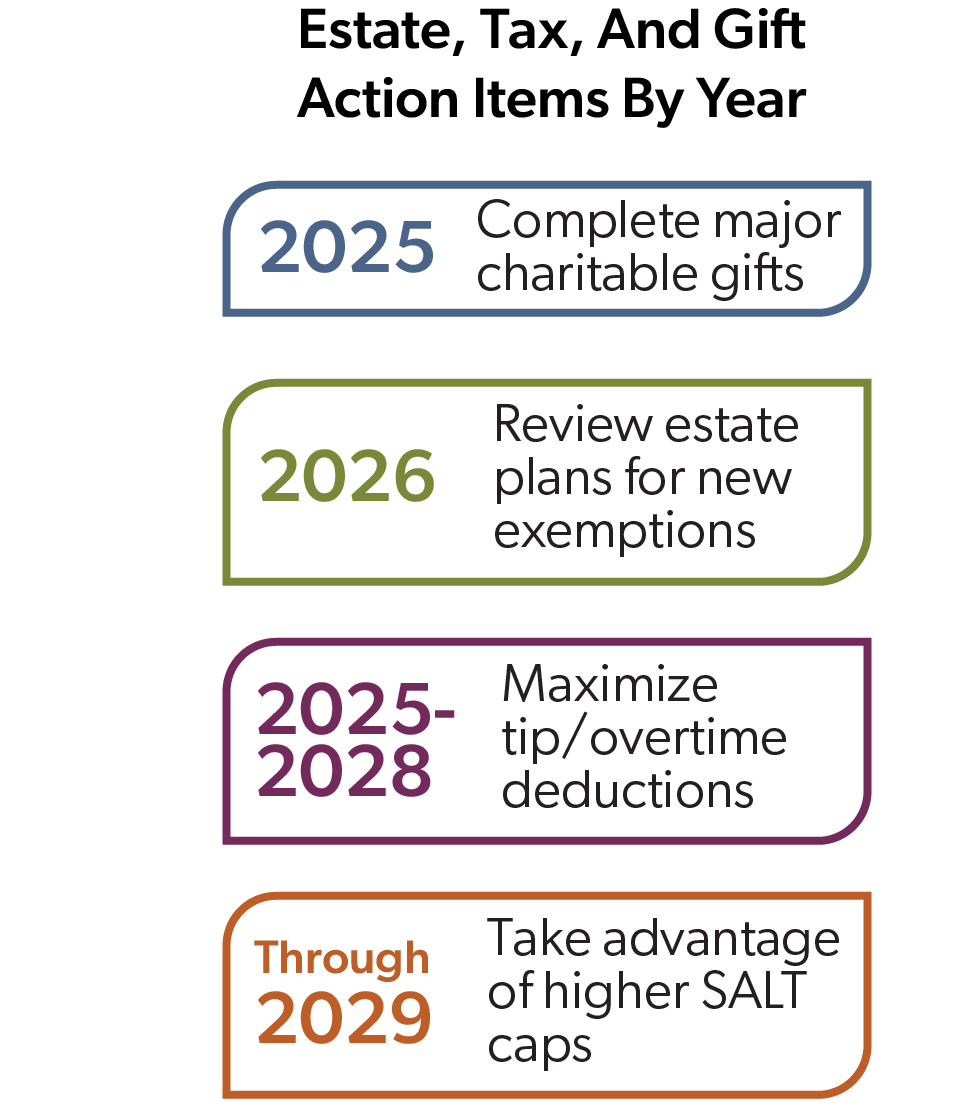

Starting in 2026, charitable deductions for itemizers will include a floor of 0.5% of adjusted gross income (AGI), and the value of itemized deductions is limited to 35 cents on the dollar for taxpayers in the top 37% tax bracket. This means large charitable gifts may be more tax-advantageous if completed in 2025 rather than deferred to later years.

The changes create planning opportunities for some while requiring strategy adjustments for others, particularly around the timing of major charitable contributions.

How Does The OBBB Affect Business Owners?

The OBBB delivers substantial benefits for business owners through deductions and tax advantages without a sunset date. These changes can create immediate cash flow improvements and long-term planning opportunities across multiple business structures.

Qualified Business Income (QBI) Deduction Enhancements

The legislation sets the QBI deduction at 20% for pass-through entities, eliminating the previous sunset timeline. The income thresholds for specified service trades or businesses increase, with phase-in ranges expanding from $50,000 to $75,000 for single filers and from $100,000 to $175,000 for joint filers.

This benefits LLCs, S-corporations, partnerships, and sole proprietorships by providing predictable tax planning around the 20% deduction. The OBBB also introduces an inflation-adjusted minimum deduction of $400 for taxpayers with at least $1,000 of QBI from active businesses where they materially participate.

100% Bonus Depreciation Returns

The OBBB reinstates 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025, and makes this provision permanent. It also expands eligibility to include manufacturing buildings placed in service before January 1, 2031.

This allows businesses to immediately deduct the full cost of equipment, vehicles, and certain buildings—rather than depreciating them over several years—creating significant cash flow advantages.

While bonus depreciation is available to businesses of all sizes and has no dollar cap, it differs from Section 179, which also allows upfront deductions but with annual limits and income-based restrictions. Read more about Section 179, which is often more flexible for small to mid-sized businesses, especially when planning around taxable income.

Tax-Free Tips and Overtime Provisions

Business owners should prepare for new reporting requirements as the legislation provides temporary deductions for employee tip income up to $25,000 and overtime compensation up to $12,500 ($25,000 for joint filers) for tax years 2025 through 2028.

While employees receive these deductions, employers must separately report qualified overtime compensation on Form W-2. Employers will need to use "reasonable methods" to estimate tip amounts for 2025, which might require HR and payroll system updates.

Should You Adjust Your Estate, Gift, And Tax Plans?

Well-drafted estate and tax plans likely remain fundamentally sound — the new tax regulations in the OBBB require a strategic review to ensure the benefits are maximized. While our Private Wealth team’s advice for clients differs depending on their personal wealth, estate, charitable, and tax goals, below are some general recommendations.

Estate Planning

Estate Planning

Review your estate plan. All estate plans need to be reevaluated at least every 10 years or when a significant life event or tax law change, like the OBBB, occurs. Read more about the nine other situations when we recommend you review your estate plan.

Higher exemption considerations. If your estate previously exceeded the $13.99 million threshold ($27.98 million for married couples) and you implemented irrevocable strategies to reduce taxable assets, those transferred assets will remain outside your estate permanently. However, if your estate falls under the new $15 million threshold ($30 million for married couples), you might continue operating under existing plans while monitoring growth.

Growth-focused planning. Estates that have grown significantly since initial planning or now approach the higher thresholds should work with estate planning professionals to evaluate new opportunities under the new legislation.

Charitable & Family Gift Planning

2025 timing advantage. Large charitable contributions may provide better tax benefits if completed in 2025 before new charitable deduction limitations take effect in 2026.

Annual exclusion gifts. Continue maximizing annual exclusion gifts ($19,000 per recipient for 2025), which remain unchanged and reduce your taxable estate regardless of exemption levels.

Business interest transfers. The QBI deduction and enhanced depreciation benefits may affect valuations for family business transfers, creating new opportunities for estate and tax planning.

Business Structure Planning

Pass-through entity evaluation. With QBI deduction status and expanded income thresholds, review whether current business structures maximize tax advantages.

State tax considerations. Higher SALT deduction caps through 2029 may influence decisions about business location and structure, particularly for multi-state operations.

Given the complexity and interconnected nature of these changes, now is the time to consult with estate planning professionals and tax experts. First Business Bank’s Private Wealth team combines extensive expertise in wealth management and estate planning to help you adapt your strategies and maximize the opportunities the OBBB creates for your financial future.

At First Business Bank, our expertise in wealth management and estate planning positions us to help you understand these modifications and adapt your financial strategies accordingly. Let's examine key changes and what they might mean for your planning.

Last Updated: 8/29/2025