Running a business means managing cash flow challenges that can appear at any time. Invoice factoring is a practical solution when businesses need working capital but can’t wait 30, 60, or even 90 days for their customers to pay.

These cash flow hurdles aren't uncommon. More than half of companies experience challenges with uneven cash flow (51%) and difficulty paying operating expenses (56%), according to the Fed's latest Small Business Credit Survey. Even profitable businesses struggle when their capital is tied up in unpaid invoices, affecting their ability to fund growth or restructuring plans.

In this article, we’ll show you how invoice factoring works as a strategic financial tool, its advantages compared to traditional financing, and which businesses benefit most from it.

What Is Invoice Factoring?

Invoice factoring is a financial arrangement where a business sells its outstanding invoices to a firm (the factor) at a discount in exchange for immediate cash. Three players participate in every invoice factoring arrangement:

- The Business - Provides goods or services and generates invoices for its customers.

- The Customers - They receive products or services and are responsible for paying the invoices.

- The Factor – Factors, like First Business Bank, purchase the business’s invoices and manage the invoice collection process.

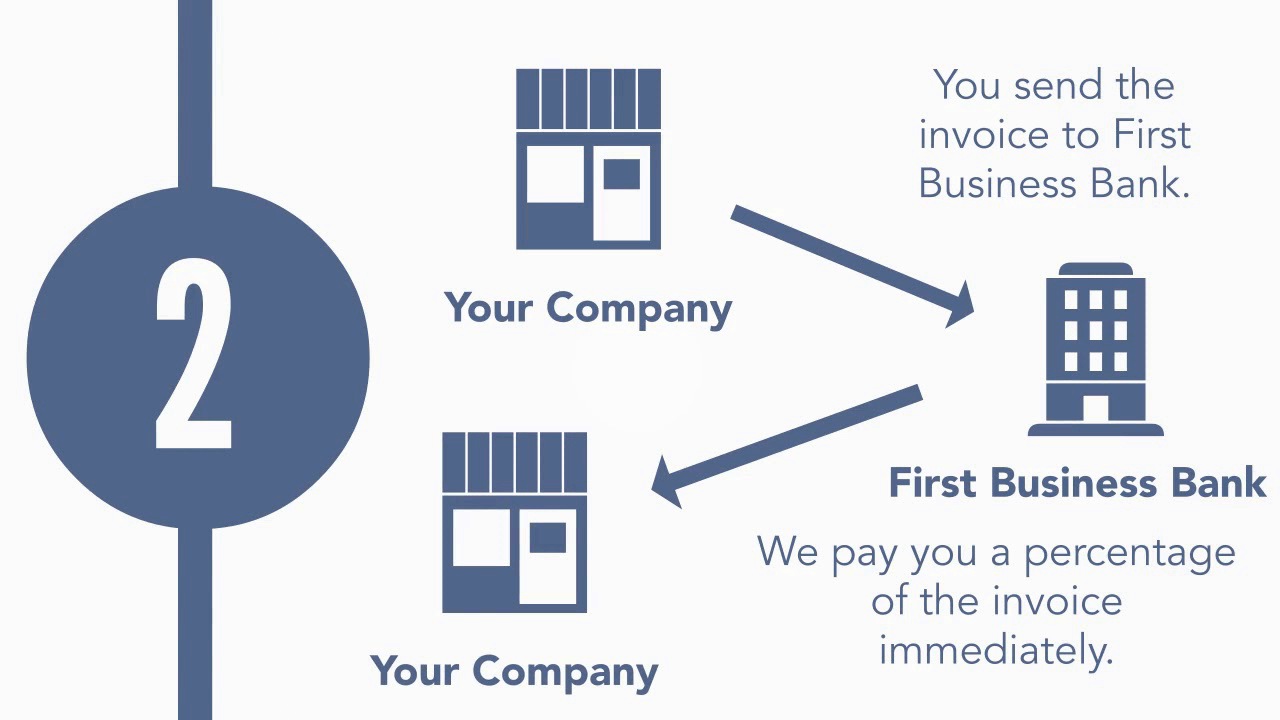

The invoice factoring process typically works in four steps:

- The business delivers products or services to its customers and issues invoices with payment terms.

- Instead of waiting for payments, the business sells invoices to an invoice factoring entity.

- The factor advances 70-90% of the invoice value immediately to the business.

- The factor releases the remaining balance, minus a fee, when the customer pays the invoice to the factor.

With invoice factoring, businesses generally receive 70-90% of the invoice value upfront, providing immediate access to capital that would otherwise be locked in invoices, waiting to be paid.

Why Do Businesses Choose Invoice Factoring?

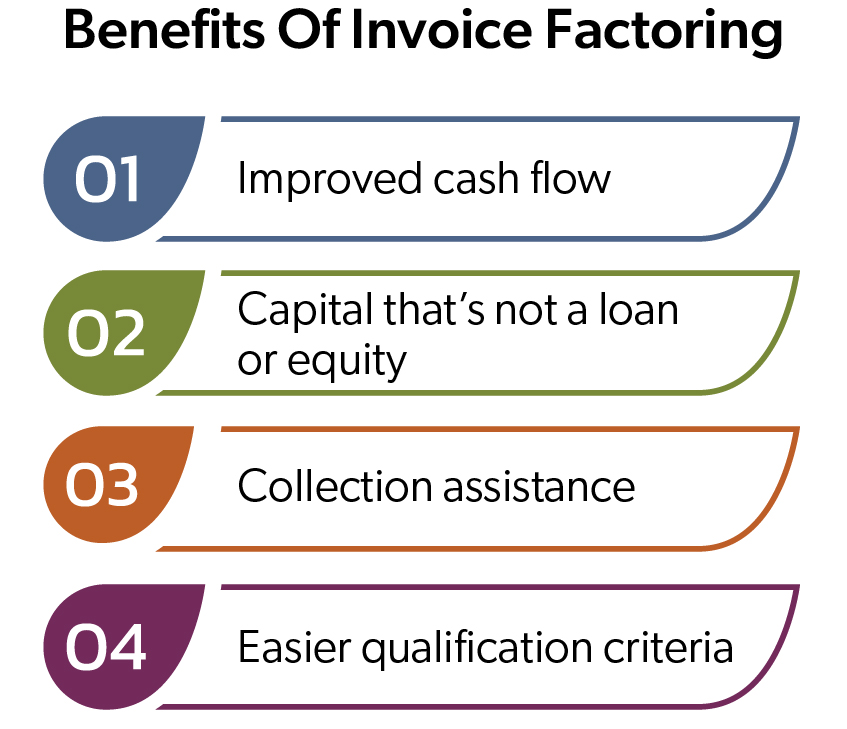

Invoice factoring offers distinct advantages that make it particularly valuable for businesses in growth phases or undergoing restructuring. Here are some benefits:

Fast Capital Access. While traditional financing, like a business loan or line of credit, can take months to establish, invoice factoring arrangements can fund in as little as 10 days because the process eliminates time-consuming field exams and extensive underwriting, saving time and money for businesses.

Fast Capital Access. While traditional financing, like a business loan or line of credit, can take months to establish, invoice factoring arrangements can fund in as little as 10 days because the process eliminates time-consuming field exams and extensive underwriting, saving time and money for businesses.

Off-Balance Sheet Financing. Invoice factoring doesn't create new debt. Instead, it converts an existing asset (invoices) into immediate cash, helping to maintain healthy debt-to-equity ratios.

Professional Collections. The factor handles payment follow-up, freeing staff to focus on core operations and growth initiatives rather than collections.

Different Credit Criteria. Invoice factoring approval involves evaluating the creditworthiness of the business's customers rather than the business. This makes invoice factoring accessible to startups, companies in transition, and businesses facing temporary financial challenges. Read how one company used invoice factoring to make millions.

How Can Invoice Factoring Fuel Business Growth?

With reliable working capital from invoice factoring, businesses can pursue growth projects and new opportunities that might otherwise remain out of reach. These initiatives might include:

Investing in Equipment and Technology. Businesses often need new equipment or technology to increase production, improve efficiency, offer new services, and expand to new markets. Invoice factoring provides capital quickly without tapping into operational funds or taking on loans.

Expanding the Workforce. Growth often requires more employees, but hiring has immediate costs — well before businesses see the payoff from adding staff. Invoice factoring bridges this gap by providing funds for onboarding and training new employees, making payroll, covering benefits and employment taxes, investing in talent acquisition or development.

Supporting Accounts Receivable Growth as Revenues Increase. As a business grows and offers its customers terms of net 30 to net 90, invoice factoring finances the cash flow deficit caused by increasing unpaid invoices. This acceleration of cash flow allows a business to turn its capital faster, allowing it to further increase its sales and profitability.

Taking on Larger Projects and Contracts. Invoice factoring gives businesses the ability to accept larger projects and more contracts than their current cash position allows. When a company knows it can quickly convert invoices into working capital through invoice factoring, it can bid on bigger contracts, accept more simultaneous projects, buy supplies and materials upfront, and more.

More capacity leads to more business which also generates more invoices that can be factored to increase capacity and grow.

How Does Invoice Factoring Work For Business Restructuring?

Businesses in transition need funding that is flexible and available quickly. Here are a few reasons why businesses turn to invoice factoring during transitions and restructuring.

Stabilizing Cash Flow During Financial Challenges. When businesses face financial difficulties, consistent cash flow is key to survival. Invoice factoring is a reliable source of working capital to enact transition plans, especially if a business’ existing lender is restricting loan availability.

Streamlining Back-Office Operations. Restructuring often requires businesses to consolidate operations and reduce overhead expenses. As invoice factoring outsources collections, it helps to reduce AR staff, eliminate the use of collections software and systems, decrease payment processing costs, and allow staff to focus on core business functions.

Funding Strategic Pivots. Restructuring sometimes involves breaking into new markets or developing products or services, all of which require capital.

Supporting Turnaround Strategies. When banks ask financially distressed companies to exit their portfolios, invoice factoring often becomes a key component of formal turnaround plans. The invoice factoring structure often works well with other restructuring initiatives and invoice factoring provides immediate cash flow for businesses turning around their operations. Once they stabilize, businesses often transition back to traditional financing arrangements.

What Types of Businesses Benefit from Invoice Factoring?

Businesses that typically fit well with invoice factoring share some common characteristics, like operating in the business-to-business (B2B) space with long payment terms, working with creditworthy customers, potentially managing seasonal demand, and experiencing high growth. Let’s take a closer look at why these are a good fit for invoice factoring.

Businesses that typically fit well with invoice factoring share some common characteristics, like operating in the business-to-business (B2B) space with long payment terms, working with creditworthy customers, potentially managing seasonal demand, and experiencing high growth. Let’s take a closer look at why these are a good fit for invoice factoring.

B2B Companies with Extended Payment Cycles. Businesses that sell to other businesses often deal with long payment terms, which can stretch 30, 60, 90, or even 120 days. This payment gap causes cash flow challenges even for financially healthy companies. Manufacturing suppliers, wholesale distributors, and professional service firms frequently turn to invoice factoring to bridge extended payment cycles.

High-Growth Businesses with Limited Capital. Invoice factoring scales naturally with their growth as more sales generate more invoices, which then provide more working capital. Technology service providers, expanding logistics companies, and growing businesses often fall into this category.

Companies in Transition or Restructuring. Businesses with a change in ownership, restructuring, or market repositioning need flexible financing that doesn't depend on historical performance. Invoice factoring focuses on current invoices rather than the past, making it ideal for restructuring.

Startups and Young Businesses. New ventures often lack a financial history for conventional loans. Invoice factoring is accessible funding based on the strength of their customers rather than their own limited track record. This advantage helps startups build capacity without diluting ownership.

Service Providers. Service businesses must pay staff and cover operational expenses before they collect from clients. Professional services, IT consulting, security services, and staffing agencies benefit from invoice factoring because it aligns their cash inflows more closely with their payroll and outflows.

How To Choose The Right Invoice Factoring Partner

Not all invoice factoring businesses operate with the same practices, fee structures, or client service standards. When evaluating invoice factoring partners, carefully consider their financial stability, funding speed, fee transparency, collection practices, and industry expertise before making a decision. Here’s more about those important aspects of an invoice factoring partner:

Financial Stability. Publicly traded companies like First Business Bank (Nasdaq: FBIZ) offer financial transparency, allowing anyone to review their financial statements and confirm their stability. Some invoice factoring companies make it difficult to evaluate their stability.

Financial Stability. Publicly traded companies like First Business Bank (Nasdaq: FBIZ) offer financial transparency, allowing anyone to review their financial statements and confirm their stability. Some invoice factoring companies make it difficult to evaluate their stability.

Funding Speed. It’s important to know how quickly the invoice factor can convert invoices to cash. Along the same lines, ask about Initial setup timeframe, typical processing for new invoices, whether there are wire transfer or ACH options to receive funds, and about any minimum invoice processing periods

Fee Transparency. The best invoice factoring partners are open and honest about their fees and rates. Unfortunately, not all factors embrace this strategy with their clients. Business leaders should understand their base invoice factoring rate, whether rates vary by invoice volume or customer, any additional fees for services or transactions, minimum monthly fees or volume requirements, and contract duration and termination conditions.

Banks operating as factors are regulated and required to maintain rigorous compliance standards that prevent hidden fees or misleading terms, helping to protect businesses from predatory practices. First Business Bank combines banking stability with specialized invoice factoring expertise.

How To Tell If Invoice Factoring Is Right For A Business?

Invoice factoring works exceptionally well for some businesses but isn't the ideal solution for everyone. Consider these questions to help determine if invoice factoring is a fit.

- Do the business’s customers typically take 30-90 days to pay invoices?

- Are cash flow gaps affecting the ability to meet obligations or pursue opportunities?

- Does the business need a financing solution that grows alongside sales?

- Is the business being held back by limited credit history or recent financial challenges?

Industries that traditionally benefit most include staffing, manufacturing, wholesale distribution, transportation, and professional services. The consultation process is straightforward, with decisions typically made within 24-48 hours after reviewing basic documentation, including:

Industries that traditionally benefit most include staffing, manufacturing, wholesale distribution, transportation, and professional services. The consultation process is straightforward, with decisions typically made within 24-48 hours after reviewing basic documentation, including:

- Industry and business model

- Customers' creditworthiness

- History of receivables turnover (ideally under 90 days)

This targeted approach allows for quick decisions – typically providing a term sheet within 24-48 hours after reviewing basic documentation.

The best way to determine if invoice factoring fits a specific situation is to speak directly with an invoice factoring expert who can evaluate the circumstances.