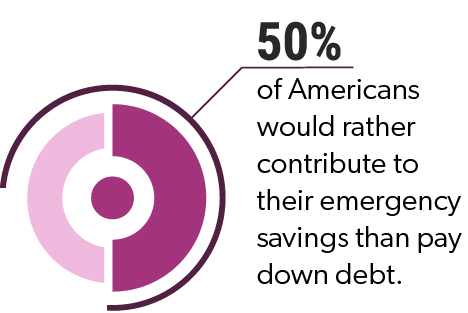

Paying down high-interest debt and investing excess funds can be great ways to help achieve your financial goals. You might often have to choose one strategy over the other. Financial planners often recommend most people pay off loans first, but in some situations, investing money is a better choice.

To help you answer this question, we need to consider various factors, such as the type of loans, interest rates, investment opportunities, and personal financial goals. In this article, Jessica Colby, Wealth Advisor, and Eric Engstrom, Investment Portfolio Manager, contribute their insights to help you evaluate whether to pay off loans or invest money.

Making The Choice To Pay Off Loans Or Invest

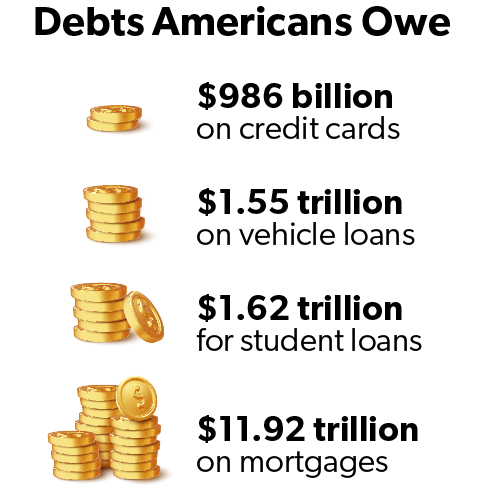

Depending on your overall financial picture, paying off debts with higher or variable interest rates may be the best place to start. For instance, credit card interest rates often run 25% or more, far above the rate of return on your average investments, and it makes sense for most people to pay those obligations down first.

“If your interest rate debts are higher than average returns, it’s common that you’d focus on paying down your debts,” said Jessica Colby. She is a Wealth Advisor at First Business Bank with more than 20 years of experience who helps clients take a holistic view of their financial health and create plans to work toward life goals.

Advantages Of Paying Down Debt Before You Invest

Some of the advantages of paying off loans before you invest include:

- Reducing your monthly expenses after your loans or credit cards are paid off

- Improving your credit score, as part of creditworthiness, is whether you pay loans on time as agreed upon

- Removing the unpredictability of paying more interest if you have a variable interest rate loan

“On the other hand, the main disadvantage of paying off loans is that it often limits your opportunity to make money on those funds,” said Eric Engstrom, Investment Portfolio Manager at First Business Bank. This is why Jessica and Eric both recommend looking individually at your debt and reviewing the interest rates. If your mortgage has a 3% interest rate, for instance, it might not make financial sense to pay it off sooner to forgo investing.

“Since the 1950s, investing in the S&P 500 has earned about 10% annually, so if you locked in a 3% interest rate, it makes more fiscal sense to invest your excess money than pay your mortgage off early,” Engstrom says.

Pay Off Loans & Invest At The Same Time

There’s also the peanut butter and jelly approach, though, where you can do some of both. Again, depending on your financial health and projected future, many people create financial plans that allow them to pay off loans while making small investments.

“The ability to accomplish both is an opportunity where, if you have a good strategic plan in place around paying down those debts, you can also take advantage of an employer 401k match to invest in your retirement,” Colby says.

Creating Your Strategy to Pay Off Loans Or Invest

First, when you start out to create your long-term financial plan that helps with decisions like whether to pay off loans or to invest, it's smart to work with a professional. “With all the variables in play, you need an expert to help you pull everything together and work toward your goals,” Engstrom says.

Next, realize that this is a good “problem” to have. When you’re considering these options, it means you have a little discretionary income. This isn’t a question of sacrificing your lifestyle.

If you do have some debt, it’s important to pay the minimum regardless so it doesn’t affect your credit score, which affects your entire financial situation. Also, make sure to maximize your 401(k) provider match. You leave what’s essentially free money on the table if you don’t take advantage of your employer’s match.

If you do have some debt, it’s important to pay the minimum regardless so it doesn’t affect your credit score, which affects your entire financial situation. Also, make sure to maximize your 401(k) provider match. You leave what’s essentially free money on the table if you don’t take advantage of your employer’s match.

Make sure you’re also regularly saving for emergencies. “The rule of thumb is to save around six months of expenses,” Colby says. “You need it to cover expenses in an emergency so you don’t put yourself in a situation where you’re racking up revolving debt to cover lifestyle expenses or potentially creating a situation where you have to liquidate securities, which can create further penalty and tax implications.”

What Happens To Your Loan Plan If You Get A Bonus Or Inheritance?

This is even more reason to work with a professional to come up with a solid plan that’s customized to your goals. You might be jazzed to pay off a car loan with a bonus, while someone else might put a down payment on a home. Creating a plan allows you the confidence to know exactly what each of your choices will do to your long-term financial health.

How Do Rising Loan Interest Rates Affect These Decisions?

“As we go through periods of higher interest rates, there’s a greater argument for paying off your variable interest rate debt sooner,” Engstrom says. “Your debt obligation goes up, so it might change your plan and you might consider paying off debt sooner. It also affects what the market and sectors of the market do, so you’ll need to reassess with your portfolio manager and assess your asset allocation to ensure it’s appropriate.”

“As we go through periods of higher interest rates, there’s a greater argument for paying off your variable interest rate debt sooner,” Engstrom says. “Your debt obligation goes up, so it might change your plan and you might consider paying off debt sooner. It also affects what the market and sectors of the market do, so you’ll need to reassess with your portfolio manager and assess your asset allocation to ensure it’s appropriate.”

“Your plan is really important with a rising interest rate environment,” Colby says. “When it comes to revolving debt – there is an opportunity to tackle short-term needs. We have clients who have larger liquidity leveraging a line of credit to cover short-term liquidity knowing later in the year they’ll be able to pay down the debt. People borrow to add to their overall asset pool with an intent to purchase investment real estate and then flipping it. Make sure you have a plan because it’s not for everyone.”

The Emotional Side of Paying Off Loans Or Investing

When it comes to money, you often have logical answers, but emotions also factor into individual strategies. Some people really hate having debt, and they would rather pay off loans than invest their money, regardless of the interest rate. Alternatively, some people might have a mountain of debt and rather take a big swing to invest their money. Considering both the logical and emotional factors in this decision is key to developing a strategy that you will stick with.

Assess Your Risk Tolerance When Making Decisions

Any time we’re talking about investing, we have to find a balance between the ability or willingness to take on risk. When you have a long time horizon, your ability to take on risk goes up because you have a lot of time to ride the waves of the market. Theoretically, you won’t pull out money at the wrong time.

“What’s your price for peace of mind?” Engstrom says. “If you like seeing your money go up incrementally over time and hate seeing it go down, your willingness for risk is probably lower. It’s a fine balance we work on with all our clients.”

“If your debt is in lower interest rates, you should sleep very well at night,” Colby says. “Try not to let your emotions govern your decisions. If you have assets for long-term investment purposes, don’t be afraid of the volatility of the market. Be afraid of the purchasing power you could lose out on over time if you’re not in the market.”

How Does Secure 2.0 Help Pay Off Loans?

The SECURE Act 2.0, passed in late 2022, includes new provisions designed to help people save for retirement as they pay off student loans.

“The new update takes effect in 2024,” Colby says. “Under the SECURE Act 2.0, when you make student loan payments, your employer can match your student loan payment to your qualified retirement plan. So, check with your employer to see if you have that benefit.”

Deciding between paying off loans or investing money can be a difficult decision. However, by evaluating the individual’s specific situation and considering the advantages and disadvantages of each option, individuals can make an informed decision that is best for their individual situation.

“Assessing your specific situation with the help of an experienced financial or wealth manager can help you determine a sustainable strategy for paying off loans or investing your money with an unbiased viewpoint,” Engstrom says.

If you tackle it yourself, consider interest rates, your risk tolerance, investment time frame, and tax implications in your approach to achieving your financial priorities.