A lot has changed for banks since the first quarter of 2023. Bankers, boards of directors, and finance teams have learned important lessons about balance sheet management, customer behavior, interest rate exposure, and liquidity. We should not leave 2023 behind us but instead, use it as an opportunity and planning guide to strengthen our balance sheets and reduce risks in 2024 and beyond.

In this article, our Bank Consulting team brings together topics from our series that focused on a central theme – lessons learned from bank failures early in 2023 and the rapid rise of interest rates. In 2023, we addressed investment portfolio best practices, interest rate risk, liquidity/contingency planning, and wholesale funding. Now, after almost two years of Fed policy tightening putting pressure on bank profitability, we may be heading into a more stable banking environment in 2024.

In this article, our Bank Consulting team brings together topics from our series that focused on a central theme – lessons learned from bank failures early in 2023 and the rapid rise of interest rates. In 2023, we addressed investment portfolio best practices, interest rate risk, liquidity/contingency planning, and wholesale funding. Now, after almost two years of Fed policy tightening putting pressure on bank profitability, we may be heading into a more stable banking environment in 2024.

However, some important questions persist: Is the market ahead of itself expecting interest rate cuts perhaps earlier than the Fed – a position favoring banks? Have deposits fully stabilized, or will deposit clients continue to seek higher-costing deposits, placing added pressure on net interest margins and liquidity? Can banks live up to investor and shareholder earnings expectations for 2024?

As our Bank Consulting team works to understand these market dynamics and offer solutions to our clients, we are asking bank executives to consider five important questions as part of their balance sheet planning.

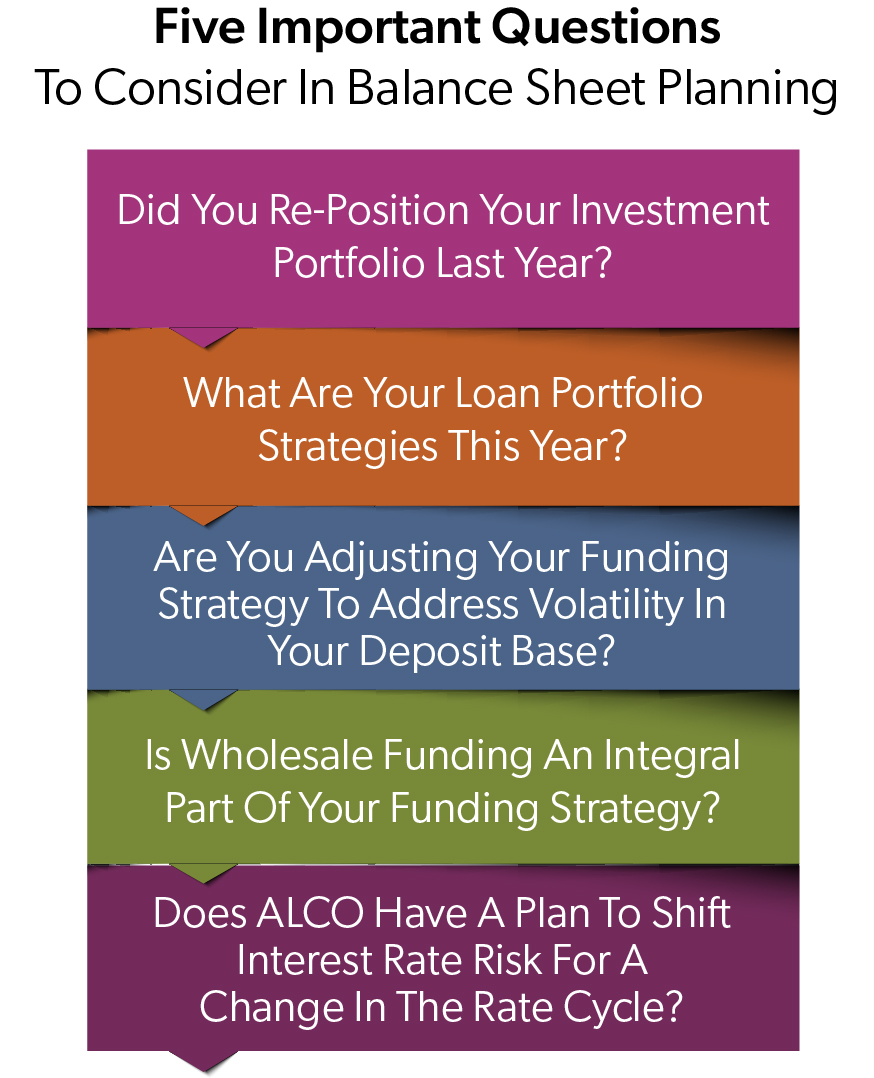

Did You Re-Position Your Investment Portfolio in 2023?

Banks likely needed to re-position investment portfolios in 2023 amid a volatile market environment. A loss-earnback strategy early in 2024 could help recoup some losses, capitalizing on attractive opportunities before a potential decline in rates. This entails extending duration beyond benchmarks to pick up added yield. The strategy does incur more price risk should rates rise. However, the extended duration means banks can capture gains when rates ultimately fall.

Looking ahead, banks should focus efforts on rebuilding resilient and diversified portfolios. The anticipation of declining rates in 2024 presents a chance to add highly rated bonds at favorable spreads. Thoughtful restructuring now can ensure income stability and guard against market fluctuations later. Strategically rebalancing and selecting securities this year sets up portfolios for success.

What Are Your Loan Portfolio Strategies in 2024?

As we enter 2024, it is prudent to align our loan growth strategy with realistic pricing and spread expectations. We anticipate lagging pressure on cost of funds as interest rates stabilize or possibly fall later this year. During this transitional period, we must maintain disciplined loan pricing and profitability rather than prematurely reducing rates. Once the cost of funds declines, we can reassess pricing accordingly. Additionally, purchasing loan participations could supplement organic growth this year.

With many lower-yielding loans coming up for renewal, we have an opportunity to reprice to current higher market rates. This repricing effort will help stabilize net interest margins in 2024 as cost of funds catches up. By taking a patient, strategic approach to loan pricing amid shifting rate environments this year, we can support loan portfolio growth while protecting profitability over the longer term.

Are You Adjusting Your Funding Strategy To Address Volatility In Your Deposit Base?

With deposits remaining volatile entering 2024, banks should reevaluate funding strategies. Analyzing large, unstable deposits can forecast potential outflows to more expensive products. We expect the migration to interest-bearing accounts to continue in 2024; however, it will likely be at a slower pace than what was experienced in 2023. Pricing shorter-term CD specials can incentivize stability and shorten the duration of liabilities. As this mix shift continues, funding betas may stay elevated in 2024.

Expanding deposit intermediary relationships can supplement retail channels and provide flexibility to change interest rates to manage deposit balances. Additionally, comprehensive incentive programs focused on deposit growth and retention can fund loan growth ambitions without over-relying on wholesale funding. The sophistication of our funding approach must match an increasingly complex deposit environment this year.

Is Wholesale Funding An Integral Part Of Your Funding Strategy?

As funding challenges persist in 2024, it’s prudent to revisit the purpose and integration of wholesale funding into your strategy for the long term. Whether for liquidity, contingency planning, or interest rate risk control, a process for effectively employing avenues like brokered deposits and Federal Home Loan Bank (FHLB) advances should be formalized. Understanding key differences in activation lead times, costs, and flexibility is paramount.

Wholesale funding enables balance sheet flexibility when retail deposit trends shift. Defining its intended usage and optimizing its deployment in coordination with other mitigation strategies allows banks to access diverse economic funding this year despite mounting uncertainty on the horizon.

Does ALCO Have A Plan To Shift Interest Rate Risk For A Change In The Rate Cycle?

With the potential for an inflection in rates, your asset-liability committee (ALCO) should reevaluate tolerance for interest rate risk exposure in 2024. We must also project how declining rates could alter prepayments or trigger loan floors. Repricing below-market loans and securities presents an opportunity, too.

By quantifying rate cycle impacts and proactively aligning fund mix, asset yields, and hedging strategies, we can shift interest rate risk to profiles that perform through turbulence. Even if a lower-rate environment does not emerge, these measures build resilience. With uncertainty ahead, our plans must provide flexibility to pivot with agility when conditions warrant.

The financial ambiguities of 2023 underscored the need to reevaluate balance sheet vulnerabilities and risk management strategies as we move into 2024. By refreshing policies, modeling stressed scenarios, improving communication around capital planning, and weighing solutions to bolster stability, banks can become more adaptive enterprises.

While we’ve outlined recommendations, each bank faces unique risks and opportunities. With a customized, proactive approach informed by big-picture perspectives and specialized analysis, bank executives can work toward profitable growth that withstands whatever lies ahead this year. Working collaboratively with our Bank Consulting team to validate assumptions, enhance forecasting, and evaluate options ensures readiness for multiple environments. That evergreen readiness provides the foundation for banks to keep communities thriving no matter what the coming years may hold.