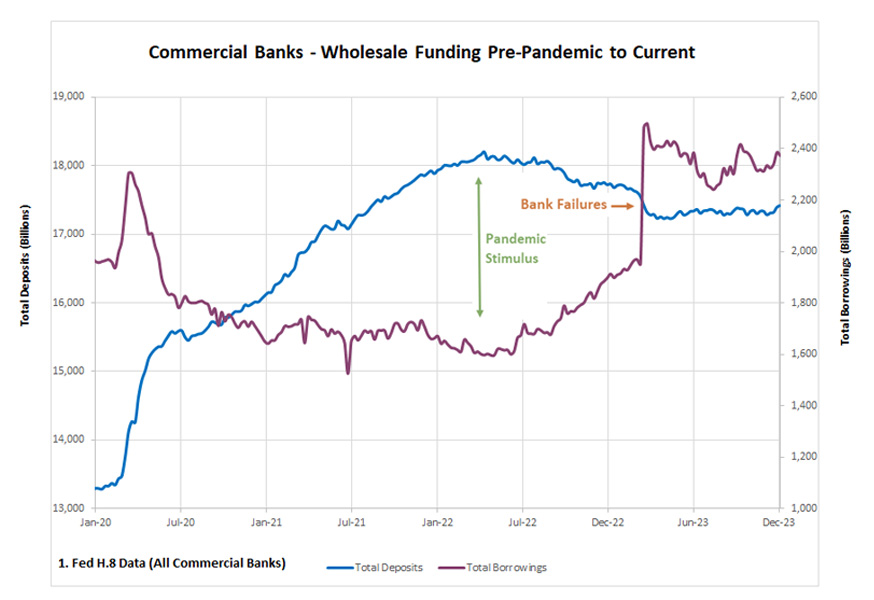

The banking industry turmoil in early 2023 and the outflow of deposits from the banking system led banks to turn to wholesale funding to shore up liquidity positions. This trend is likely to continue as banks look to build greater certainty into liquidity and contingency planning, match-fund long-term fixed rate loans, and better manage interest rate sensitivity.

As deposits gradually normalize to pre-pandemic levels and Asset Liability Committees (ALCO) consider different liquidity strategies, it’s important to consider many nuances surrounding wholesale funding within a bank Asset Lability Management (ALM) strategy.

Since its early days in the 1990s, First Business Bank has used wholesale funding as part of its liquidity strategy — and continues to do so today — which helps to differentiate the bank’s performance from its peers. Now, the experienced Bank Consulting experts at First Business Bank, including former CFO Ed Sloane, share insights about how to successfully incorporate wholesale funding into your ALM strategy and why wholesale funding isn’t just a safety net during tough times but also a tool that can provide ongoing strategic advantages.

While a community bank’s primary funding source is its core deposit base, adding a wholesale funding strategy to the mix gives ALCO and the finance team new tools to manage balance sheet growth and reduce interest rate risk and funding volatility.

Overview of Wholesale Funding Instruments

The most commonly employed wholesale funding instruments within financial institutions of all types are Federal Home Loan Bank (FHLB) advances and brokered deposits.

FHLB advances require pledging of loans and/or securities and purchase of FHLB stock. Collateral is subject to FHLB eligibility and compliance requirements. There are no regulatory restrictions, and funding is immediately available. Terms range from overnight to 10+ years in callable, puttable, amortizing, and floating rate advances. Advances can be prepaid; however, prepayment includes a make-whole penalty.

Brokered deposits are FDIC insured and have no pledging or collateral requirements. However, undercapitalized banks cannot accept brokered deposits, and funding may not be immediately available. Other features include terms ranging from 1 month to 10+ years, and callable, amortizing, and floating CDs are available. Regulators recommend a brokered deposit limit of 10% to 20% of total deposits. Additionally, FDIC penalties apply for brokered deposits in excess of 10% of average assets.

Wholesale Funding Considerations in Asset Liability Management

Incorporating wholesale funding into a bank's Asset Liability Management strategy requires careful consideration of cost, liquidity risk, interest rate fluctuations, and the impact on the bank's overall financial stability. When evaluating wholesale funding, banks should consider the following:

Prudent use of wholesale funding to manage a potential liquidity gap. When using wholesale funding to address potential liquidity gaps, banks must thoughtfully assess both their immediate and future funding requirements under various scenarios while also considering the anticipated growth of their balance sheets, the stability and makeup of their deposit base, the role of their investment portfolios in liquidity management, and establishing appropriate liquidity metrics based on the bank’s risk tolerance limits and targets.

Consider size, duration, optionality, cash flow, laddering, and hedging. Like investment portfolio transactions, when selecting wholesale funding instruments, bank executives should consider the different variables that may affect the overall balance sheet. Determining the proportionate size for their wholesale funding portfolio relative to total funding sources ensures alignment with the institution’s liquidity and strategic planning. Fully evaluating these details provides a structural framework and helps ensure optimal financial stability and flexibility in responding to market dynamics.

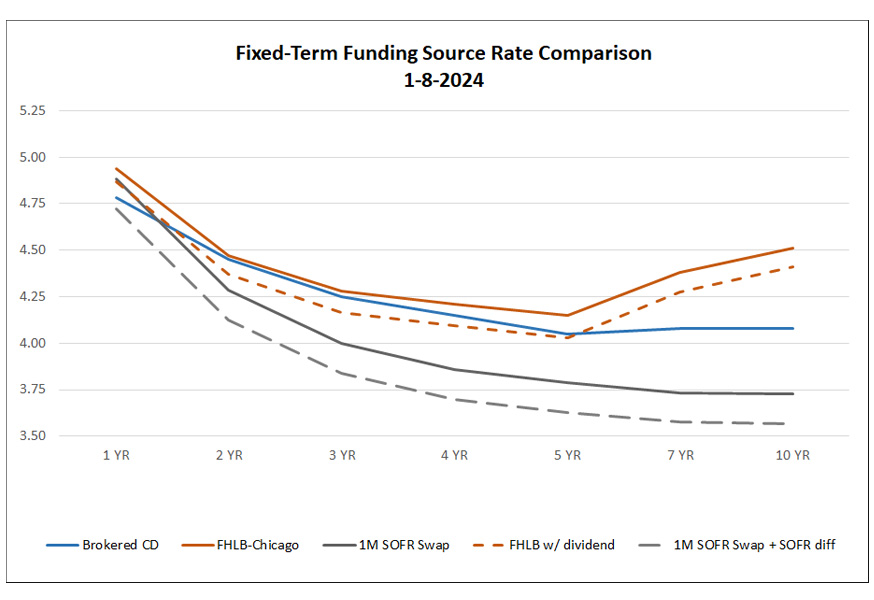

Use the lowest cost of wholesale funds available. When selecting a wholesale funding source, banks need to factor in the desired term, required collateral, and the flexibility they might need in pricing, such as the ability to prepay early. Different sources, like brokered CDs and FHLB advances, have varying rates and terms, so it’s smart to conduct a thorough comparison to pinpoint the most cost-effective option. To ensure stability and profitability, banks should always maintain a funding premium over deposit rates, calibrated to their specific funding requirements, risk appetite, and competitive climate.

Match-fund long-term fixed-rate loans: Banks can use wholesale funding to match-fund long-term fixed-rate loans, locking in spreads and reducing interest rate risk. ALCO should consider a variety of wholesale funding options to match or adjust their interest rate exposure to longer-duration assets, which can lead to a more neutral interest rate sensitivity position and greater stability in their net interest margin. Additionally, the use of wholesale funds provides ALCO greater flexibility to address rate exposure across the entire maturity timeline.

Implement borrowing swaps to lower the cost of wholesale funds: To optimize the cost of wholesale funds, consider implementing cash flow hedge swaps, like issuing and then rolling 3-month FHLB advances or brokered CDs and converting them to fixed. This approach typically offers a more cost-effective fixed funding option compared to longer-term wholesale funds. By strategically capitalizing on beneficial spots in the swap curve versus the funding curve, you can further reduce costs. It's essential to note the inverse relationship between Accumulated Other Comprehensive Income (AOCI) on swaps and investments, a nuance that can impact the overall strategy.

Augment a strong deposit-centric growth strategy. Consider implementing incentives that support a deposit-centric growth strategy in your long-term planning. For instance, equip lenders to align their loan production with deposit growth targets and incentivize deposit-focused outcomes through individual compensation and bonus structures. Moreover, given that new loan growth is primarily backed by wholesale funds rather than the balance sheet, it's advisable to use wholesale deposit or FHLB pricing as a benchmark for loan pricing — a trend likely to persist in the foreseeable future.

Understand the risks of wholesale funding. This includes familiarizing oneself with the collateral eligibility criteria for FHLB advances, both in terms of loans and securities. Recognizing constraints on FHLB collateral during stressful times can influence borrowing capacity, and it's advisable to incorporate haircuts into liquidity stress tests. Pledging securities can affect asset liquidity with FHLB advances, and there are prepayment penalties that impact liquidity, earnings, and capital. Furthermore, it's essential to consider the AOCI implications when dealing with borrowing swaps in varying rate climates and to understand how FHLB advances versus brokered deposits influence the loan-to-deposit ratio.

Wholesale Funding Portfolio Management

When managing a wholesale funding portfolio, bank executives should actively incorporate it into the ALCO process. This means evaluating methods to cut wholesale funding costs, laddering maturities to meet both short and long-term funding needs, and considering optionality, collateral requirements, and the entire portfolio's duration.

Planning & Executing Wholesale Funding with Specialized Guidance

Considering all the factors that go into adding a wholesale funding strategy into Asset Liability Management, bank executives will discover several advantages when working with an experienced outside consultant, like the Bank Consulting team at First Business Bank. First Business Bank has consistently incorporated wholesale funding into its liquidity strategy since its inception in 1990. This approach, sustained over the years, has given the bank a competitive edge and ALCO opportunities to understand how each of the variables affects the bank’s balance sheet.

Aside from bringing specialized expertise and a proven track record executing wholesale funding in ALM strategies, outsourcing to external experts offers several other benefits. With a history of successfully deploying a strategy that includes wholesale funding, an outside firm can help ALCO evaluate the different variables and set up clear internal policies and procedures. By having robust processes and the necessary paperwork ready, they can swiftly and effectively tap into brokered and FHLB markets. Outside experts also help your bank executives prepare for collateral reviews, evaluate risk tolerance, and set ALCO limits, targets, and key metrics.

Finally, working with an outside bank consulting firm allows internal staff to concentrate on their primary duties while providing them opportunities to learn about industry best practices, facilitating quicker adoption of new practices or regulatory requirements.

Leveraging Wholesale Funding for Long-Term Success

After the events of early 2023, wholesale funding has helped many banks ensure liquidity and stability in response to deposit outflows. For an institution aiming to navigate these waters, it's essential to fully evaluate the intricacies of tools like FHLB advances and brokered deposits, each with its advantages and considerations. More than just a response to challenges, wholesale funding provides strategic advantages, allowing banks to manage interest rate risks, optimize costs, and align with long-term planning. While in-house strategies are crucial, there's undeniable value in leveraging outside expertise, like our experienced Bank Consulting professionals.

Published: January 2023