First Quarter 2026

This report outlines key bank performance trends and strategic recommendations to help your bank capitalize on the current economic environment.

First Quarter vs Fourth Quarter Banking Trends*:

Balance sheet growth slowed in the first quarter due primarily to a decrease in loan balances. Bank earnings moderated, reflecting a decline in net interest income, partially offset by lower credit costs. Some notable trends are summarized below:

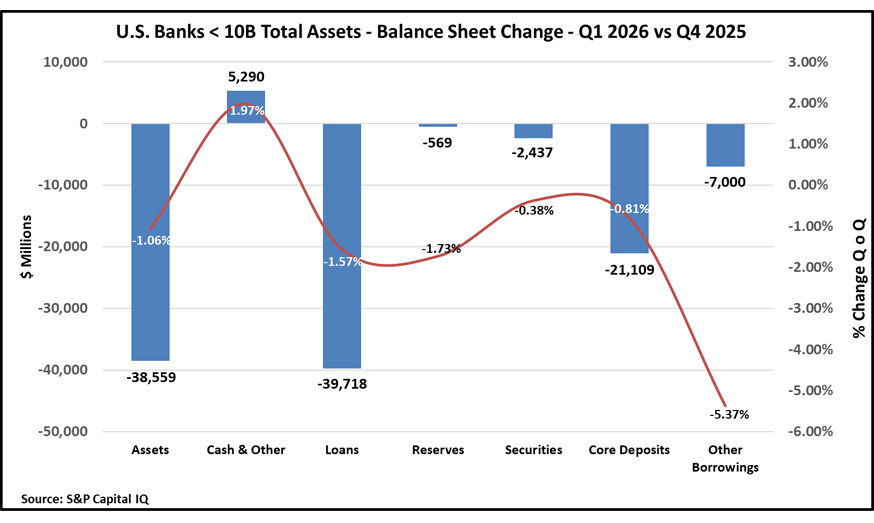

- Loan and deposit balances decline. Bank balance sheets were smaller in Q1, as loan balances dropped 6.3%, annualized. Core deposits declined 3.3%, providing a liquidity offset to the decline in loan balances. Banks utilized excess liquidity to shed higher-cost wholesale funding and add to short-term investments.

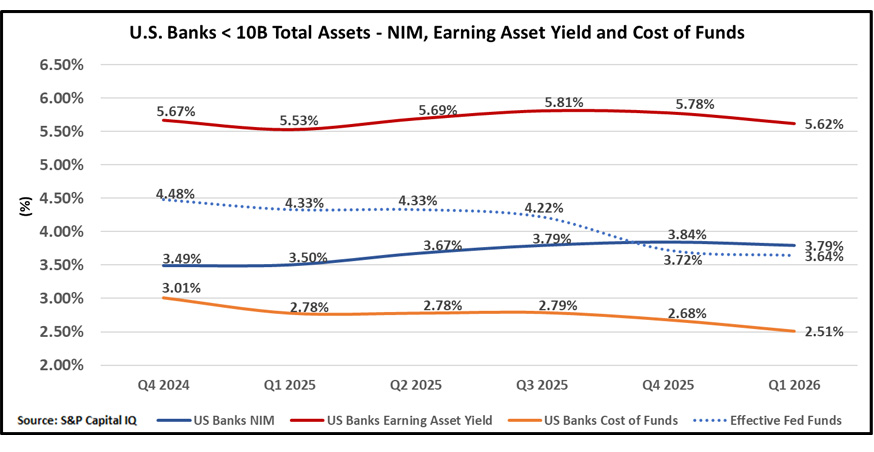

- NIM moderates with Fed pause. The decline in earning asset yields accelerated in Q1, down 16 bps. The sharper decline is an indication that repricing benefits experienced last year have diminished and banks are now seeing pricing pressure on new loan volume. The cost of funds declined 17 bps as banks continued to lower deposit costs to keep pace with declining asset yields.

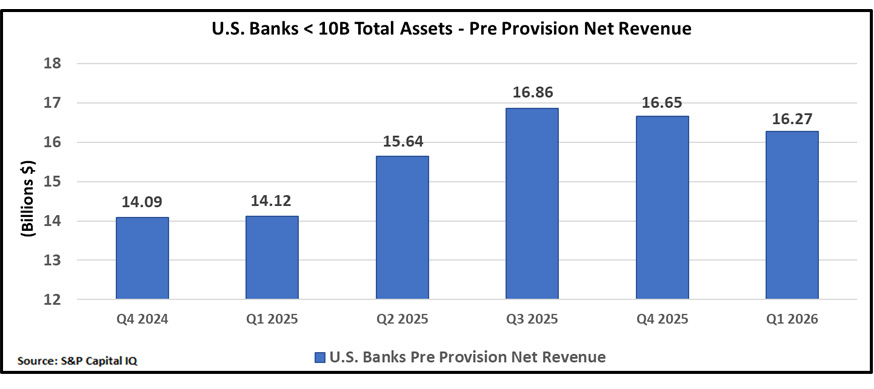

- Pre-provision net revenue growth slows. Top-line revenue declined 2.97% primarily due to net interest income, reflecting a slowdown in loan growth and a 5 bp drop in NIM. Expenses and fee income declined 3.40% and 3.62%, respectively.

- Credit metrics remained strong. NPA and NCO ratios were 0.74% and 0.26%, respectively for the quarter, showing little change over the past several quarters. Loan loss provisioning declined 1.65% in the linked quarter and loan loss reserves remained stable at 1.29%.

- Regulatory update. Bank deregulation continues in 2026 as regulators focus on increasing capital efficiency with significant policy changes expected in the first half of this year. Key actions among Federal regulators include loosening capital requirements, encouraging bank mergers, and reducing compliance burdens for community banks.

Bank Strategies - Remainder of 2026 and Beyond:

Our bank strategies are designed to improve your NIM to target level performance and build a greater level of NIM stability by creating a neutral interest rate sensitivity position on your balance sheet.

In our Strategies in the Spotlight segment, we address two timely topics which we believe are key to improving long-term performance: 1) core deposit strategies to enhance growth and 2) the integration of wholesale funding sources into your liquidity planning and IRR management.

Core Deposit Strategies

Competition for deposits is intensifying in 2026 as large banks are using their market strength to pull in new customers, leaving community banks vulnerable. This appears to be most prevalent in the Midwest markets. As loan growth is expected to gain traction in 2026, banks are looking to add deposits at a faster pace. These pressures could signal some NIM headwinds brought on by rising deposit costs as we progress through the year. We outline a few strategy reminders to stay ahead of mounting market pressure:

- Adopt a deposit-first mentality. This is about building a deposit culture through a strong treasury management team that works seamlessly with bankers.

-

- The strategic plan should lay out growth expectations that cascade through the organization with meaningful incentive programs for building and retaining the full client relationship.

- Train bankers to secure deposits first as part of negotiating the loan.

- Bankers should make every attempt to self-fund their loans.

- A loan pricing model can be an effective tool to incent for deposits. Such models can be used to place a premium or value on deposits and relationships, giving bankers greater flexibility to competitively price the loan.

- Deconstruct your core deposit base. Understanding the composition of deposits can give a bank insight into how a client may behave due to a change in market conditions.

- Perform a deposit study to evaluate behaviors and migration trends.

- Identify relationship vs non-relationship deposits to determine loyalty level.

- Track and measure changes to the full banking relationship.

- This insight may assist the treasury management team and bankers in determining if any exception or premium pricing is warranted.

- Deposit pricing committee discipline. The deposit pricing committee should be viewed as an extension of ALCO strategies and the strategic plan. Members need to be acutely aware of both sides of the balance sheet and how their deposit decisions may affect liquidity, pricing, and growth in other areas of the balance sheet.

- Finance must have a prominent role in deposit pricing to enforce ALCO strategies.

- Short-term NIM forecasting is essential to understand the impact of deposit pricing decisions.

- How well matched are non-maturity deposits to the floating rate loan portfolio?

- Is there immediate interest rate risk to consider in the pricing decisions?

- Are earning asset yield and interest-bearing liability betas aligned?

- Determine if your bank is a market leader, middle of the pack, or historically at the low end of your competitor’s rates.

- Set exception pricing at an acceptable level below the cheapest wholesale funding rates. Continue to review exception pricing regularly, even in a stable rate environment.

- Deposit intermediaries. Use these programs to aid in building a stable core deposit base, manage liquidity by reducing reliance on more expensive wholesale funding, and lessen the need to pledge collateral.

Wholesale Funding Strategies

It’s prudent liquidity management to add multiple funding tools to the toolbox to supplement core deposit growth. Recall the safety and soundness scare from a few years ago brought on by a couple of sizable bank failures, and the resulting liquidity pressure placed on the industry. These events were compounded by a rapid rise in interest rates and an outflow of deposits to non-bank alternatives. This perfect storm led banks to the wholesale markets to stabilize liquidity. Below are some of our thoughts regarding FHLB advances and brokered deposits. We recommend using these instruments interchangeably to improve liquidity planning and IRR management.

- FHLB Advances. By far the most widely used wholesale funding source, FHLB advances provide a flexible and efficient secondary source of funding to the industry. Some key features include:

- Funding capacity limits based on loan and security collateral requirements.

- A wide range of terms and structures to reduce short and long-term exposure to interest rates and match funding to long-term assets.

- Member programs and analysis such as deposit studies or customizing a wholesale funding portfolio to meet liquidity needs.

- Brokered Deposits. A funding alternative to FHLB, brokered deposits have grown in popularity over the last several years, gaining greater acceptance among regulators as a reliable secondary source of funds. Some features to consider and compare with FHLB advances include:

- No collateral requirements.

- Can free up FHLB capacity.

- Classified as a deposit, brokered deposits can lower the loan-to-deposit ratio.

- Other considerations

- Even if you do not have an immediate need for wholesale funding, it is worth the effort to complete the agreements, collateral requirements, and processes, providing a secondary source of funds in a potential liquidity crisis.

- Always compare the best rate and term, including the swap curve. A cash flow borrowing swap can reduce funding costs by 25+ basis points compared to brokered and FHLB rates.

- Set internal limits. For example, establish a wholesale funding limit or target based on a percentage of total funding sources or as a percentage of capital.

Other ALM strategies:

- Investment portfolio strategies

- Purchase considerations. The curve is upward sloping with roll down effect in play over the next year. Consider concentrating on duration protection or lower call/prepay risk bonds maintaining duration in a range of 4 to 6 years.

- Restructuring opportunities. We recommend a quarterly review of the securities portfolio for repositioning. This review should involve either realizing losses and reinvestment in higher-yielding loans or securities or looking for opportunities to sell bonds that have rolled down the curve along with longer-duration, lower-yielding securities.

- Hedging strategies. There are a variety of hedging tools available to mitigate interest rate risk and create a more neutral balance sheet. These may include back-to-back swaps, restructuring pay-fixed/receive float swaps, buying 15-to-20 year municipals and swapping to float, cash flow hedges to fund the balance sheet which carries an added benefit of reducing funding costs, and caps and floors.

The fed funds rate is on hold for now as the FOMC continues to carefully assess incoming data, evolving data, and associated risks. Contributing to the pause is the rise in inflation, which is currently viewed as transitory, brought on mostly by spiking energy prices due to the war in Iran. With rates on pause for now, we see the potential for NIM headwinds moving forward, driven by intensifying competition for deposits leading to higher deposit costs, and aggressive loan pricing amid the prospects of growing loan demand.

*Source: S&P Capital IQ, US Banks < $10B

Date: 5/28/2026